Costco (COST) - Fundamental Analysis Report 2026 (Updated)

Dear Readers, Welcome to Deep Research Global.

Let’s analyze the topic in detail.

Executive TL;DR

Costco (COST) delivered fiscal 2025 net sales of $269.9 billion, up 8.1%, with diluted EPS of $18.21 and membership fee income of $5.32 billion.

Q2 fiscal 2026 net sales reached $68.24 billion with diluted EPS of $4.58 (up from $4.02), while April 2026 four-week sales jumped 13.0% and total company comparable sales rose 11.6%.

The company operates 928 warehouses worldwide as of early May 2026, with a stated target of 30+ new openings annually, anchored by membership renewal rates near 92.7% in the US/Canada.

Valuation remains elevated with a forward P/E in the mid-40s range, reflecting the market’s belief that Costco’s flywheel of membership fees, private-label scale, and operational discipline can compound earnings for years.

Table of Contents

Executive TL;DR

Introduction

Costco Company Profile: Key Facts

Costco Investment Thesis

The Membership Flywheel Is the Real Asset

Pricing Power Through Value, Not Markup

The Kirkland Signature Compounder

Operational Discipline as a Cultural Asset

Costco Business Model Overview

The Limited-SKU, High-Velocity Model

Membership Tiers and Economics

Ancillary Businesses and Trip Frequency

E-commerce and the Digital Layer

Costco Revenue Analysis

Fiscal 2025 Full Year Numbers

Q1 Fiscal 2026 Recap

Q2 Fiscal 2026 Detail

March and April 2026 Monthly Sales

Decomposition: Traffic vs. Ticket vs. New Units

Margins, Earnings Quality, and EPS Trajectory

Gross Margin Construction

SG&A Discipline

Operating Income and Margin

EPS Trajectory and Quality

Cash Flow Mechanics

Operating Cash Flow Engine

Capital Expenditures

Free Cash Flow and Capital Returns

Balance Sheet Health

Liquidity and Cash Position

Debt Profile

Working Capital and Inventory

Costco Segment-by-Segment Teardown

Core Merchandise Categories

Gasoline Business

Pharmacy, Optical, and Hearing Aids

Food Court

E-commerce and Third-Party Delivery

Costco Business Centers

Strategic and Competitive Context

The Warehouse Club Landscape

The Broader Retail Picture

Tariffs and Supply Chain

Labor and Wage Strategy

Valuation Framework

Where the Multiple Sits Today

Bull Case Valuation Anchor

Bear Case Valuation Anchor

Discounted Cash Flow Considerations

Bull, Base, and Bear Case Scenarios

Bull Case

Base Case

Bear Case

Key Risks for Costco

Multiple Compression Risk

Consumer Demand and Macro Cycle

Labor and Wage Inflation

Tariff and Trade Policy

International Execution

Digital and Last Mile

Catalysts to Watch

Near-Term Catalysts (Next 6 to 12 Months)

Medium-Term Catalysts (12 to 24 Months)

Long-Term Catalysts (24+ Months)

My Final Thoughts

Latest Analyst Price Targets

Official Sources and Data

Disclaimer: This analysis is for informational & educational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with their personal financial advisors before making investment decisions. Past performance does not guarantee future results.

Introduction

Costco rarely surprises on the upside the way a growth tech name does, yet the company has quietly built one of the most durable compounding machines in the S&P 500.

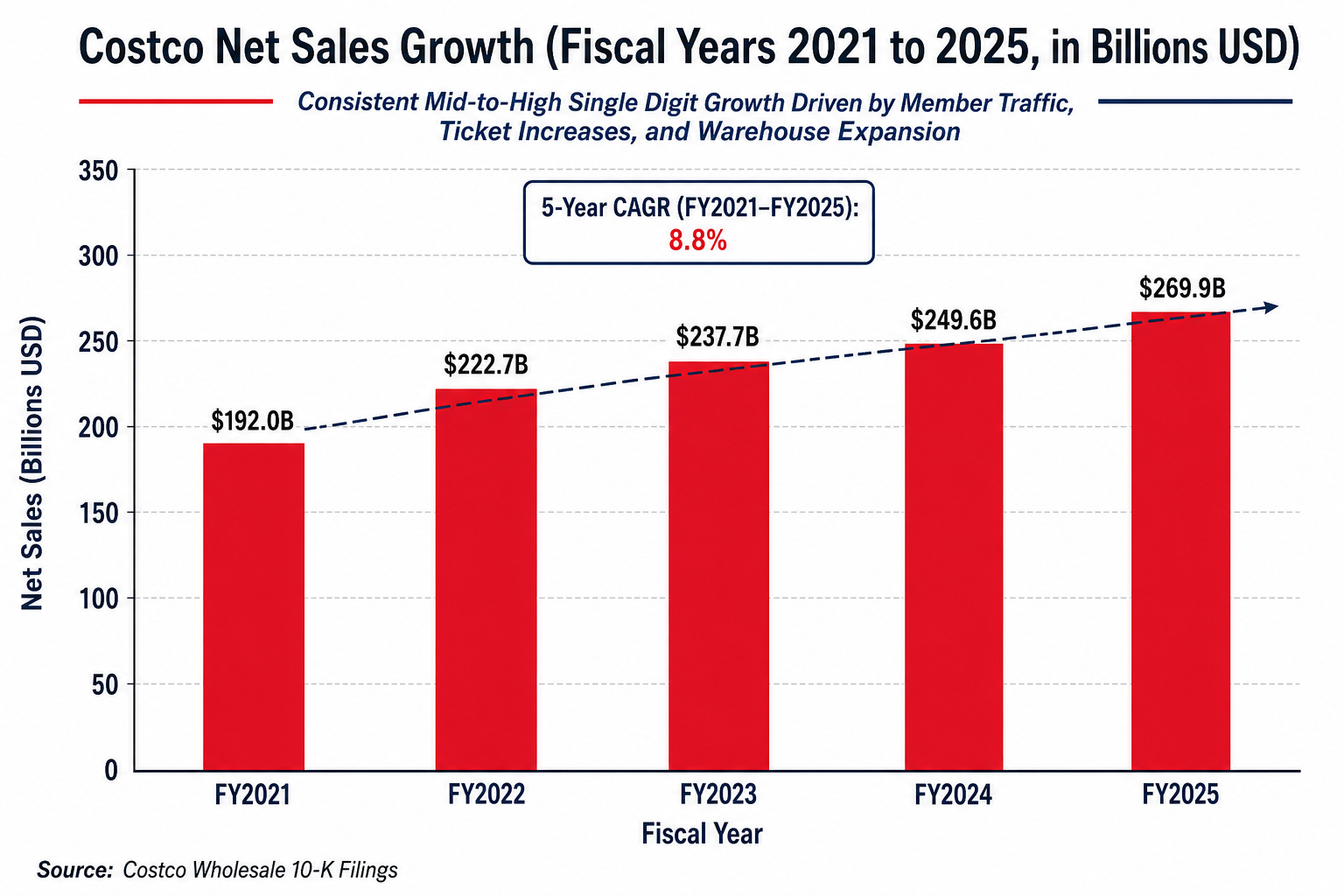

Net sales have grown from $192 billion in fiscal 2021 to $269.9 billion in fiscal 2025, and recent months have shown comparable sales reaccelerating into double digits when calendar shifts cooperate.

The setup heading into the back half of fiscal 2026 is interesting because membership fee economics are still working, private-label Kirkland Signature is rumored to be a $90 billion brand on its own, and management is leaning into a 30-warehouse-per-year expansion cadence even as the stock trades at a premium multiple.

This in-depth analysis report dissects every operating lever, every line of the income statement, and the realistic bull, base, and bear scenarios for Costco investors.

Costco Company Profile: Key Facts

Costco Wholesale Corporation, founded in 1983 and headquartered in Issaquah, Washington, operates the world’s largest membership warehouse club chain by revenue.

The business is led by President and CEO Ron Vachris, who took the top job in January 2024 after spending decades at the company starting as a forklift operator.

The company trades on the Nasdaq under the ticker COST and is a component of major indexes including the S&P 500 and Nasdaq-100. As of May 6, 2026, the company operates 928 warehouses across 14 countries and territories.

Costco Wholesale Corporation - Quick Facts Snapshot

---------------------------------------------------

Ticker / Exchange: COST / Nasdaq

Headquarters: Issaquah, Washington, USA

Founded: 1983 (Costco); merged with Price Club 1993

CEO: Ron Vachris (since January 2024)

CFO: Gary Millerchip

Fiscal Year End: 52/53-week year ending late August

FY2025 Net Sales: $269.9 billion

FY2025 Net Income: $8.099 billion

FY2025 Diluted EPS: $18.21

Total Warehouses (May 2026): 928

Total Cardholders: Over 145 million (per FY2025 annual report)

US/Canada Renewal Rate: ~92.7%

Worldwide Renewal Rate: ~90.5%

The company’s economic model is simple in concept: charge members an annual fee for the right to shop at limited-SKU, high-volume warehouses that sell name brands and Kirkland Signature private label at low markups.

The fee income, not retail margin, is the primary economic engine.

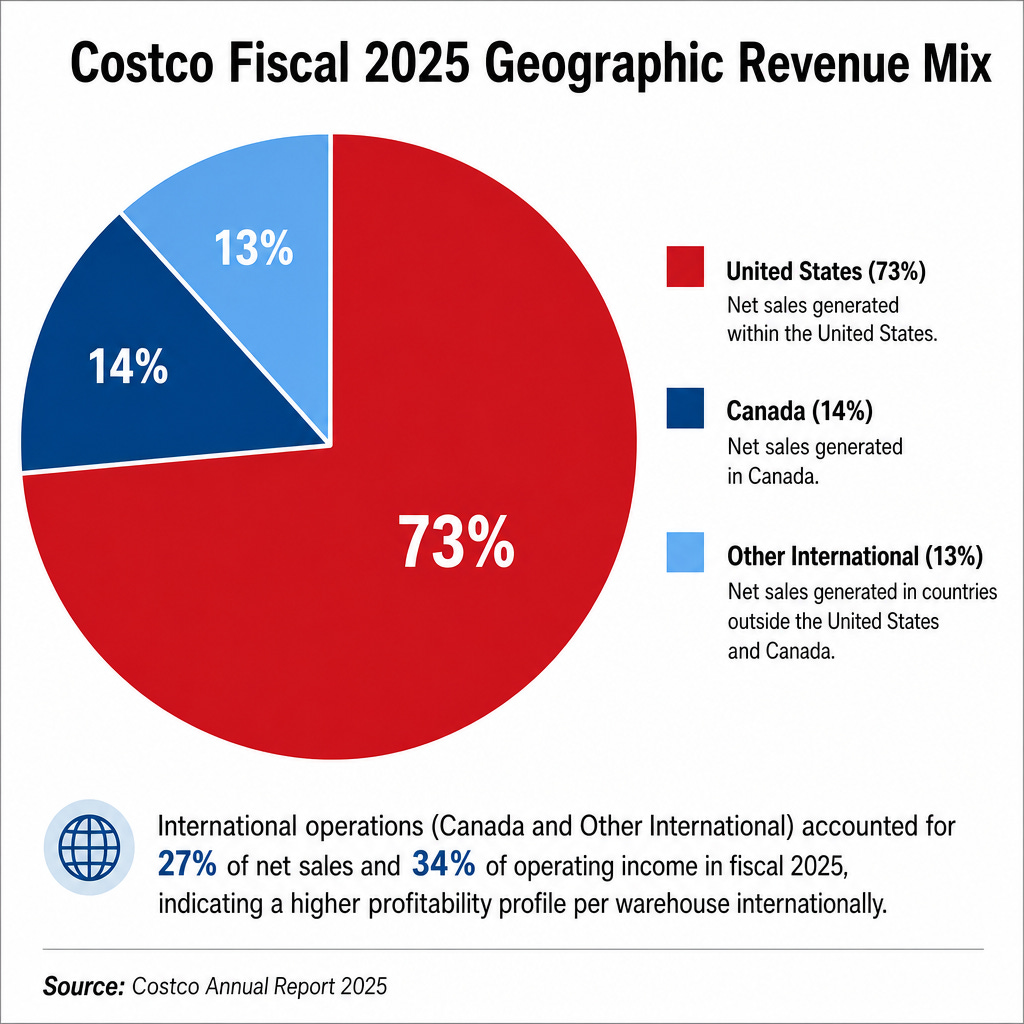

Image source: Deep Research Global analysis based on Costco Annual Report 2025)

Costco Investment Thesis

The Membership Flywheel Is the Real Asset

Costco’s stock chart often distracts investors from the structural reality of the business. The annual membership fee of $65 for Gold Star and $130 for Executive members in the US and Canada flows almost entirely to operating income because there is no incremental cost to service it.

That single line item generated $5.32 billion of revenue in fiscal 2025 and roughly half of total operating income. The September 2024 fee increase, the first since 2017, did not damage retention.

In fact, recent disclosures show the US and Canada renewal rate sitting around 92.7%, with the worldwide rate at roughly 90.5%. Those numbers are extraordinary for any consumer subscription business and almost unheard of for one paid in cash up front.

Pricing Power Through Value, Not Markup

Costco’s promise to members is built on selling fewer SKUs at lower markups than peers. Management has historically capped markups at 14% for branded merchandise and roughly 15% for Kirkland Signature, well below the 25 to 50 percent gross markups found at traditional supermarkets and big-box competitors.

This discipline is the moat. When inflation hits, members trust that Costco will absorb cost pressure rather than chase headline margin. The result is a flight-to-value dynamic during both expansions and recessions.

The 2026 tariff environment is the latest test of that promise. Management has publicly stated they will pass tariff refunds back to members if they materialize from pending US Supreme Court action.

The Kirkland Signature Compounder

Kirkland Signature has become a brand of its own scale. Recent shareholder communications indicate the private-label line generated approximately $90 billion in retail sales during fiscal 2025, larger than the standalone revenue of Boeing, FedEx, or T-Mobile.

Kirkland items typically deliver 15 to 20 percent savings versus comparable national brands while preserving Costco’s margin structure. That gap is the lever that lets the company compete on price while still funding capital expenditures.

Investment Thesis Pillars - Quick Reference

--------------------------------------------

Pillar 1: Membership fee annuity (~$5.3B in FY25, growing ~10% YoY)

Pillar 2: Below-market markups create durable value moat

Pillar 3: Kirkland Signature private label at ~$90B run rate

Pillar 4: Warehouse expansion runway of 30+ openings/year

Pillar 5: Digital flywheel accelerating with same-day delivery

Pillar 6: Net cash balance sheet with capital return optionality

Operational Discipline as a Cultural Asset

Founder Jim Sinegal’s principles still permeate the operating culture. Vachris reportedly works from a cubicle in Issaquah, and the company maintains no separate media relations team, which keeps overhead lean.

The investor takeaway is that Costco’s SG&A discipline is not a quarterly KPI to be optimized but a cultural reflex. That makes it sticky in a way most retailers cannot replicate.

Costco Business Model Overview

The Limited-SKU, High-Velocity Model

A typical Costco warehouse carries roughly 4,000 SKUs versus 30,000 to 50,000 at a typical supermarket and 100,000-plus at a Walmart Supercenter. This narrow assortment lets the company concentrate buying power and turn inventory faster than peers.

Inventory turns at Costco run materially higher than at most large retailers, meaning the company often sells goods before having to pay suppliers. That working capital dynamic is a quiet source of negative cash conversion benefit on the balance sheet.

The warehouses themselves are intentionally austere, with concrete floors, exposed steel ceilings, and product displayed on the original shipping pallets. Every dollar saved on store presentation flows through to member prices.

Membership Tiers and Economics

Costco currently offers three primary US and Canada membership types: Gold Star at $65 per year for individuals, Business at $65 per year, and Executive at $130 per year. Executive members earn a 2% reward on most purchases, capped at $1,250 annually.

The strategic significance of Executive membership cannot be overstated. Executive members represent roughly 47.7% of paid members but 74.2% of worldwide sales. That means the most loyal half of the base drives nearly three-quarters of revenue.

Costco Membership Tier Economics

---------------------------------

Tier US/Canada Annual Fee Key Benefit

Gold Star $65 Standard warehouse and online access

Business $65 Add-on cards, business buying

Executive $130 2% reward (max $1,250/yr) plus extras

Executive Members: ~47.7% of paid members

Executive Sales Share: ~74.2% of worldwide sales

Ancillary Businesses and Trip Frequency

Costco operates a deep stack of ancillary businesses inside or adjacent to its warehouses. The annual report lists 747 gas stations at the close of fiscal 2025, with gasoline alone representing roughly 10% of net sales.

Beyond fuel, members visit Costco for pharmacy, optical, hearing aids, tire installation, photo, travel, and the famous food court. Each of these services creates a reason to make incremental trips, lifting traffic and basket size.

The optical and hearing aid businesses in particular are durable margin contributors because they leverage in-warehouse real estate that is already paid for. They also tend to attract older, higher-income members who anchor renewal.

E-commerce and the Digital Layer

Historically Costco was viewed as a digital laggard. That narrative has flipped meaningfully. In fiscal 2025, e-commerce sales grew 15.6% and the company began incorporating third-party delivery channels including Instacart, Uber Eats, and DoorDash into its e-commerce metric starting after Q4 2025.

In April 2026, digitally-enabled comparable sales rose 18.8%, and Q2 fiscal 2026 saw digital comps of 22.6%. That kind of growth from a $250 billion-plus base is rare.

The strategic logic of the digital push is to convert younger, urban members who might shop less frequently in person into multi-touchpoint customers. Same-day delivery, the Uber Eats partnership, and the buy-now-pay-later expansion all serve that goal.

Costco Revenue Analysis

Fiscal 2025 Full Year Numbers

Costco closed fiscal 2025 (ended August 31, 2025) with total revenue of $275.24 billion, comprised of $269.9 billion in net sales plus $5.32 billion in membership fees. Net sales grew 8.1% versus the prior year on roughly 5.9% total company comparable sales growth.

The remaining contribution came from

Keep reading with a 7-day free trial

Subscribe to Deep Research Global to keep reading this post and get 7 days of free access to the full post archives.