Datadog - SWOT Analysis Report (2026)

Our comprehensive Datadog SWOT analysis evaluates the company’s potential to sustain its growth trajectory in the observability platform sector.

The cloud observability market stands at a transformative crossroads as enterprises accelerate their digital transformation initiatives and artificial intelligence (AI) workloads reshape infrastructure requirements.

Datadog, Inc. $DDOG ( ▼ 1.85% ) , the monitoring and security platform for cloud applications, has emerged as a dominant force in this sector. With revenue surpassing $886 million in Q3 2025 alone, representing 28% year-over-year growth, the company demonstrates remarkable resilience amid macroeconomic headwinds that have challenged many of its peers.

For investors seeking exposure to the intersection of cloud infrastructure, AI, and enterprise software, understanding Datadog’s competitive position requires an examination of its strengths, weaknesses, opportunities, and threats.

Our comprehensive SWOT analysis provides a strategic framework for evaluating the company’s potential to sustain its growth trajectory through 2026 and beyond, offering insights critical for portfolio allocation decisions in the observability platform sector.

Table of Contents

Executive Summary: Datadog’s Market Position at a Glance

Datadog operates at the epicenter of two converging technological megatrends: the ongoing migration to cloud-native architectures and the exponential growth of AI-driven workloads.

The company’s unified observability platform has achieved remarkable market penetration, serving approximately 32,000 customers as of September 30, 2025, including a substantial portion of Fortune 500 enterprises.

This customer base generates an impressive annual recurring revenue (ARR) profile, with 4,060 customers contributing $100,000 or more in ARR, representing a 16% increase year-over-year.

The company’s strategic positioning combines several competitive advantages: a comprehensive product portfolio spanning infrastructure monitoring, application performance management (APM), log management, security monitoring, and increasingly, AI observability; a differentiated land-and-expand business model that drives multi-product adoption; and industry-leading recognition, including Leader status in multiple Gartner Magic Quadrants for 2025.

These strengths position Datadog favorably as enterprises grapple with increasingly complex technology environments.

However, investors must also weigh significant challenges facing the company.

Pricing complexity has emerged as a recurring customer concern, with usage-based billing creating unpredictability in total cost of ownership.

Intensifying competition from both established players like Dynatrace and New Relic, as well as emerging open-source alternatives, threatens margin compression and market share.

Additionally, macroeconomic headwinds have prompted enterprises to scrutinize software spending, leading to optimization initiatives that can temporarily constrain revenue growth.

Key Performance Indicators Summary

Metric Q3 2025 YoY Growth

─────────────────────────────────────────────────────────

Revenue $886M +28%

Total Customers ~32,000 +9.5%

$100K+ ARR Customers 4,060 +16%

Free Cash Flow $214M +24% margin

Non-GAAP Operating Margin 23% Stable

AI-Native Revenue Contribution 12% of total +253% YoY

Understanding Datadog’s Business Model and Market Context

Before examining the SWOT framework, investors must understand how Datadog generates value in the observability ecosystem.

The company operates a software-as-a-service (SaaS) platform that ingests, processes, and analyzes massive volumes of telemetry data from customers’ infrastructure, applications, and services.

This data provides real-time visibility into system performance, security posture, and user experience metrics that are essential for modern DevOps and IT operations teams.

The Land-and-Expand Growth Engine

Datadog’s land-and-expand strategy represents a fundamental pillar of its growth model. Customers typically begin with a specific use case—perhaps infrastructure monitoring or APM—and progressively adopt additional products as they recognize the value of unified observability. This approach creates several investor-relevant dynamics:

Product Adoption Progression

83% of customers use 2 or more products

52% of customers use 4 or more products (up from 49% a year ago)

31% of customers use 6 or more products

Average revenue per customer continues expanding

The economic logic is compelling: as customers consolidate monitoring tools onto Datadog’s platform, switching costs increase dramatically. Each additional product integration creates technical dependencies and institutional knowledge that make migration to competitors progressively more difficult and expensive.

Market Opportunity and Total Addressable Market

The observability platform market is experiencing robust expansion driven by several secular trends. According to industry research, the global observability platform market is projected to reach $13.9 billion by 2034, growing at a 23.3% compound annual growth rate. Enterprise monitoring markets show similar trajectories, with the enterprise monitoring sector expected to reach $184.65 billion by 2034.

These projections understate the opportunity in several critical dimensions:

AI Observability: As enterprises deploy machine learning models and AI agents at scale, monitoring requirements multiply exponentially. Traditional observability tools lack the context-aware capabilities needed for AI workloads, creating greenfield opportunities for platforms like Datadog that have developed specialized AI observability products.

Security Convergence: The blurring boundaries between observability and security create expansion opportunities. Datadog’s Cloud Security Posture Management (CSPM), Cloud Workload Security, and Application Security products tap into distinct budget pools while leveraging the same underlying telemetry infrastructure.

Digital Experience Monitoring: As customer experience becomes a competitive differentiator, frontend monitoring and real user monitoring (RUM) transition from nice-to-have to mission-critical, expanding Datadog’s addressable market beyond traditional IT operations teams.

Image source: dynatrace.com

STRENGTHS: Competitive Advantages Driving Market Leadership

1. Comprehensive Platform Architecture and Integration Ecosystem

Datadog’s most formidable strength lies in its unified platform architecture, which consolidates disparate monitoring functions that historically required multiple point solutions. In October 2025, the company achieved a significant milestone by surpassing 1,000 integrations on its platform, underscoring the breadth of technology coverage available to customers.

This integration ecosystem provides several strategic advantages:

Vendor Consolidation Value Proposition

Traditional Multi-Vendor Approach Datadog Unified Platform

─────────────────────────────────────────────────────────────

Infrastructure: Vendor A Infrastructure: Datadog

APM: Vendor B APM: Datadog

Logs: Vendor C Logs: Datadog

Security: Vendor D Security: Datadog

Synthetics: Vendor E Synthetics: Datadog

RUM: Vendor F RUM: Datadog

Result: Data silos, integration Result: Unified data model,

overhead, fragmented insights correlated insights, single pane

The platform’s ability to correlate data across infrastructure, application, and security layers creates insights that fragmented point solutions cannot replicate. When an application performance issue occurs, Datadog can automatically trace it to underlying infrastructure problems, network latency, or security events, dramatically reducing mean time to resolution (MTTR).

2. Robust Financial Performance and Cash Generation

Datadog’s financial strength provides strategic flexibility for investment in product development and strategic acquisitions. The company’s Q3 2025 performance demonstrates exceptional operational discipline:

Financial Metric

Q3 2025 Performance

Strategic Implication

Revenue

$886M (+28% YoY)

Sustained high growth despite market maturation

Free Cash Flow

$214M

Demonstrates operational efficiency and scalability

Free Cash Flow Margin

24%

Among highest in enterprise software sector

Non-GAAP Operating Margin

23%

Proof of unit economics at scale

Cash & Securities

$4.1B

War chest for strategic initiatives

The company’s ability to generate substantial free cash flow while maintaining aggressive growth distinguishes it from many growth-stage software companies that sacrifice profitability for expansion. This balanced approach reduces execution risk and provides downside protection during market corrections.

Operating Leverage Analysis

Revenue Growth: +28% YoY

Operating Expenses: Growing slower than revenue

Result: Expanding margins demonstrating

operating leverage

For investors, this financial profile suggests Datadog has achieved the critical inflection point where incremental revenue increasingly translates to incremental profit, a characteristic of durable franchise businesses.

3. AI-Native Customer Growth and AI Observability Leadership

Perhaps the most strategically significant strength is Datadog’s positioning at the forefront of AI observability. The company reported that AI-native customers now represent 12% of total revenue, up from 6% a year ago, with revenue from this cohort growing 253% year-over-year.

This explosive growth reflects several underlying dynamics:

AI Workload Monitoring Complexity: Traditional observability tools struggle with AI workloads due to:

Non-deterministic behavior of machine learning models

Complex data pipelines spanning training and inference

GPU utilization patterns that differ from CPU workloads

Model drift and performance degradation over time

Prompt engineering and token usage optimization needs

Datadog has developed specialized capabilities to address these challenges, including LLM Observability that provides end-to-end tracing across AI agents, visibility into inputs and outputs, latency tracking, token usage monitoring, and error detection at each step.

AI-Native Customer Characteristics

Attribute

Impact on Datadog

Higher data volumes

Increased usage-based revenue per customer

Complex architectures

Greater product adoption breadth

Rapid scaling

Faster ARR expansion

Mission-critical nature

Lower churn rates

The strategic significance cannot be overstated. As enterprises across all sectors integrate AI capabilities, Datadog’s early leadership in AI observability creates a powerful moat. Teams deploying production AI systems have limited viable alternatives, positioning Datadog to capture disproportionate value from what may be the most significant technology shift since cloud computing.

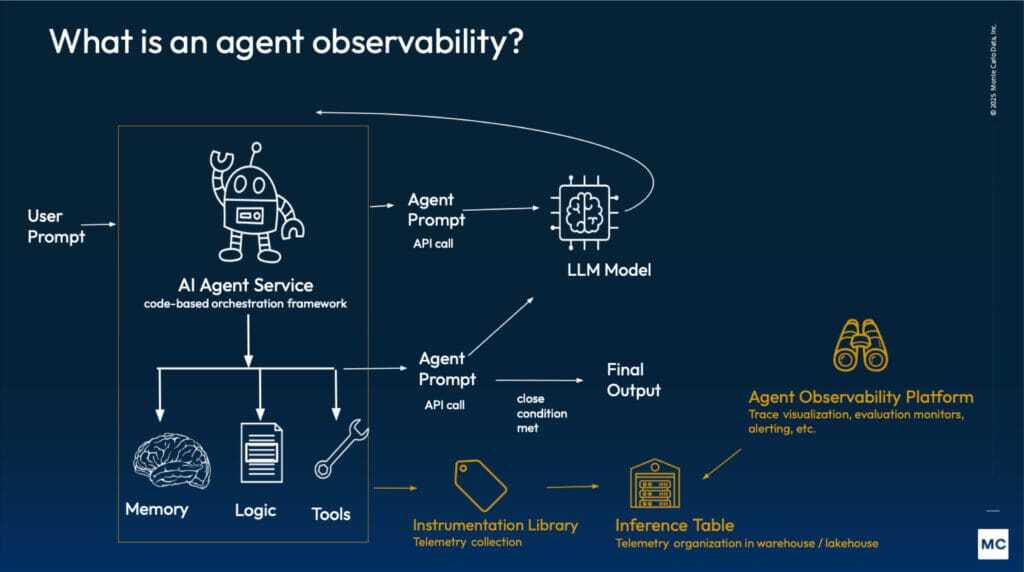

Image source: montecarlodata.com

4. Customer Quality and Enterprise Penetration

Datadog’s customer base skews toward large, sophisticated enterprises with complex technology environments and substantial budgets. This customer profile provides several advantages:

Large Customer Expansion Dynamics

Fortune 500 penetration creates long-term revenue visibility

Complex environments drive multi-product adoption

Enterprise budgets support premium pricing

Strategic relationships reduce competitive displacement risk

The company’s success in landing and expanding within large enterprises is evidenced by the robust growth in high-value customer cohorts. The 4,060 customers with $100,000+ in ARR represent the quality end of the customer spectrum, typically featuring multi-year contracts, multiple product deployments, and strategic vendor relationships.

Recent customer wins illustrate this strength. In Q3 2025, Datadog announced a seven-figure annualized expansion with a Fortune 500 financial services company starting with 14 products, and a seven-figure deal with a Fortune 500 technology hardware company adopting 11 products. These sophisticated deployments demonstrate that enterprise IT leaders view Datadog as a strategic platform rather than a tactical tool.

5. Industry Recognition and Analyst Validation

Gartner’s recognition of Datadog as a Leader in the 2025 Magic Quadrant for Observability Platforms marks the fifth consecutive year the company has achieved this status. Additionally, Datadog earned Leader recognition in the 2025 Magic Quadrant for Digital Experience Monitoring, with the highest position for Ability to Execute among all vendors.

These analyst endorsements carry significant weight in enterprise purchase decisions. IT leaders evaluating observability platforms frequently rely on Gartner research to develop vendor shortlists, and Leader positioning substantially increases the probability of inclusion in competitive bids. The consistency of this recognition over multiple years also validates that Datadog’s competitive advantages are durable rather than transitory.

6. Product Innovation Velocity and R&D Capabilities

Datadog maintains an aggressive product innovation cadence, regularly releasing new capabilities that expand addressable markets and deepen competitive moats. The company’s R&D investment as a percentage of revenue remains substantial, enabling continued innovation across multiple vectors:

Recent Innovation Highlights

AI & ML:

- Bits AI Agents for SRE, Developers, and Security teams

- TOTO time-series foundation model

- LLM Experiments for prompt optimization

- Enhanced AI observability for Amazon Bedrock and Strands

Data Management:

- Flex Frozen for cost-optimized log retention

- Archive Search for long-term log analysis

- CloudPrem for data residency compliance

Platform Enhancements:

- 1,000+ integration milestone

- MCP Server for extensibility

- Enhanced Oracle Cloud Infrastructure support

The breadth of innovation demonstrates that Datadog is not resting on its existing product portfolio but actively expanding into adjacent markets and addressing emerging customer needs. This innovation velocity creates a moving target for competitors, who must not only match Datadog’s current capabilities but also keep pace with continuous enhancements.

WEAKNESSES: Vulnerabilities and Internal Challenges

1. Pricing Complexity and Customer Cost Concerns

Despite its technical strengths, Datadog faces recurring criticism regarding pricing complexity and total cost of ownership unpredictability. The company’s usage-based pricing model, while theoretically aligning costs with value, creates several challenges:

Pricing Friction Points

Issue

Customer Impact

Business Risk

Overage charges

Budget surprises and CFO scrutiny

Relationship strain, churn risk

Metric explosion

Costs scale faster than anticipated

Defensive optimization behavior

Log volume unpredictability

Monthly bill volatility

Reduced adoption of log management

Complex SKU structure

Difficult cost modeling

Extended sales cycles

Industry analysis reveals that Datadog’s pricing can become prohibitively expensive as organizations scale, with some customers reporting 30% quarterly bill increases. These cost concerns have prompted a cottage industry of Datadog cost optimization services and tools, suggesting the issue is widespread rather than isolated.

The strategic risk extends beyond individual accounts. When customers experience billing surprises, they often respond by:

Implementing aggressive filtering to reduce ingested data

Limiting product adoption to essential use cases only

Evaluating competitors with more predictable pricing models

Advocating internally for vendor diversification

For investors, the pricing perception issue represents a potential governor on growth velocity. While Datadog’s net revenue retention remains healthy at approximately 120%, optimization-driven headwinds could compress this metric if macroeconomic conditions deteriorate further.

2. Customer Acquisition Costs and Sales Efficiency Pressures

As Datadog has matured and moved upmarket toward larger enterprises, customer acquisition costs have naturally increased. Enterprise sales cycles are longer, requiring extensive proof-of-concept engagements, security reviews, and multi-stakeholder buy-in. The company’s Q3 2025 commentary noted that new customer contribution to revenue growth increased to 25%, up from 20% in Q2, indicating healthy acquisition momentum, but the efficiency of this acquisition warrants scrutiny.

Sales Efficiency Considerations

Metric Trend Implication

──────────────────────────────────────────────────────────────

Sales & Marketing % of Revenue ~27% Significant

Enterprise Sales Cycle Lengthening Higher CAC

Average Contract Value Growing Offsets CAC increase

Payback Period 12-18 months Within norms

While current metrics remain within acceptable ranges for enterprise SaaS companies, investors should monitor whether the company can maintain efficient growth as it exhausts the easier-to-reach segments of its addressable market. The land-and-expand model mitigates this concern somewhat, as expansion revenue requires less sales investment than new logos, but the challenge persists.

3. Dependence on Third-Party Cloud Infrastructure

Datadog’s platform runs on public cloud infrastructure, primarily AWS, which creates both operational and economic dependencies. The company incurs substantial costs for compute, storage, and data transfer from cloud providers, and these costs represent a significant portion of the cost of revenue.

Infrastructure Cost Dynamics

Factor

Current State

Risk Dimension

Cloud Provider Pricing

Stable but subject to change

Gross margin compression if prices increase

Data Egress Costs

High for cross-region traffic

Limits architectural flexibility

Vendor Lock-in

Limited multi-cloud leverage

Negotiating position constraints

Regional Expansion

Requires new infrastructure investment

Capital intensity of geographic growth

The economic challenge manifests in gross margins. While Datadog achieves impressive 80-81% gross margins, these trail pure-software companies that don’t incur infrastructure costs. Any deterioration in cloud provider economics flows directly to Datadog’s unit economics.

Additionally, this dependency creates operational risks. Major cloud provider outages directly impact Datadog’s service availability, and the company’s own reliability is partially contingent on third-party infrastructure operators. While Datadog has architected for high availability across multiple availability zones and regions, the fundamental constraint remains.

4. Limited Geographic Diversification

Datadog generates the majority of its revenue from North American customers, particularly within the United States. While the company operates globally and serves international customers, geographic concentration creates several risks:

Geographic Revenue Distribution (Approximate)

North America: ~60-65% of revenue

Europe: ~25-30% of revenue

Asia-Pacific: ~10% of revenue

Other: ~5% of revenue

This concentration exposes the company to region-specific risks:

Macroeconomic Exposure: North American economic conditions disproportionately impact financial performance

Regulatory Risk: U.S. regulatory changes have outsized effects on the business

Competitive Dynamics: Regional competitors may have advantages in local markets where Datadog has limited presence

Currency Risk: Dollar strength can make Datadog’s pricing less competitive internationally

For comparison, many enterprise software peers achieve more balanced geographic distribution, with 40-50% of revenue from international markets. Datadog’s relative under-indexing internationally represents both a weakness and an opportunity.

5. Talent Acquisition and Retention in Competitive Market

The company competes for engineering, sales, and product talent in one of the most competitive labor markets globally. As a New York-headquartered company, Datadog faces wage pressures from financial services firms, technology giants, and well-funded startups all competing for the same talent pool.

Talent Market Challenges

Competitive compensation requirements pressure operating margins

Stock-based compensation dilution concerns for existing shareholders

Remote work trends enable competitors from any location

Specialized skill requirements (AI/ML, distributed systems, security) face particularly acute shortages

The company’s Q3 2025 financial statements show stock-based compensation of $200.6 million in the quarter, or approximately 23% of revenue. While this level is not unusual for high-growth technology companies, it represents a real economic cost to shareholders through dilution. Investors should monitor whether compensation costs remain proportional to value creation or begin exceeding optimal levels.

OPPORTUNITIES: Growth Vectors for 2026 and Beyond

1. AI and Machine Learning Infrastructure Monitoring Explosion

The most significant growth opportunity for Datadog stems from the proliferation of artificial intelligence workloads across enterprise environments. As organizations transition from experimental AI projects to production deployments, observability becomes mission-critical infrastructure rather than a convenience.

AI Infrastructure Growth Drivers

The company’s position in this market is already yielding results, with AI-native customers growing from 6% to 12% of revenue in a single year. However, the opportunity has barely begun to materialize:

AI Adoption Stage

Current Penetration

Observability Need

Datadog Positioning

Experimentation

High (~60-70% of enterprises)

Low (development tools sufficient)

Limited revenue opportunity

Pilot Deployments

Medium (~30-40%)

Medium (monitoring becomes useful)

Early adoption phase

Production at Scale

Low (~10-15%)

High (observability becomes critical)

Maximum capture potential

As the distribution shifts rightward toward production deployments, Datadog stands to capture exponentially more value. A single large language model deployment monitoring contract can generate hundreds of thousands to millions in annual revenue, given the data volumes and monitoring complexity involved.

AI Observability Revenue Model

Traditional Application:

- 10-50 metrics per instance

- Moderate log volumes

- Standard APM traces

AI Application:

- 100-500 metrics (GPU utilization, inference latency, token usage)

- High log volumes (model inputs/outputs for debugging)

- Complex traces (multi-model workflows, vector database queries)

Revenue Multiple: 5-10x per workload

The company’s recent product innovations, including specialized LLM observability features, position it to capture disproportionate share of this greenfield market. Competitors that treat AI monitoring as an afterthought will struggle to match Datadog’s specialized capabilities.

2. Security and Compliance Market Expansion

The convergence of observability and security creates substantial expansion opportunities. Datadog’s security products, including Cloud Security Posture Management (CSPM), Cloud Workload Security, and Application Security Monitoring, tap into distinct budget allocations while leveraging the same underlying telemetry infrastructure.

Security Market Opportunity Dimensions

The global cloud security market is projected to exceed $40 billion by 2026, growing at over 20% annually. Datadog’s differentiation comes from its ability to correlate security signals with operational telemetry, enabling:

Integrated Security and Observability Use Cases

Use Case

Traditional Approach

Datadog Advantage

Vulnerability Response

Security team identifies issue, submits ticket to engineering

Real-time correlation with affected workloads and automatic remediation workflows

Performance vs. Security Trade-offs

Siloed decisions leading to suboptimal outcomes

Unified visibility enabling informed trade-off decisions

Incident Investigation

Manual correlation across multiple tools

Automated timeline reconstruction across security and operational events

Compliance Monitoring

Point-in-time audit snapshots

Continuous compliance verification with operational context

The company’s 2025 State of Cloud Security Report findings indicate that enterprises are adopting more sophisticated security strategies, creating demand for the integrated approach Datadog provides.

3. International Market Expansion and Geographic Diversification

Datadog’s relative under-penetration in international markets, particularly in Asia-Pacific and emerging markets, represents a substantial growth opportunity. While international expansion carries execution risks, the company’s SaaS delivery model and existing global infrastructure provide a foundation for acceleration.

International Expansion Opportunity Matrix

Region Penetration Opportunity Strategic Priority

───────────────────────────────────────────────────────────

Europe Medium-High $5-7B TAM Consolidate position

Asia Low-Medium $8-10B TAM High growth potential

L. America Low $1-2B TAM Selective expansion

Middle East Low $1-2B TAM Emerging opportunity

The company’s success in achieving GovRAMP High Authorization “In Process” status demonstrates its capability to meet stringent requirements for regulated markets, a skill transferable to international public sector opportunities.

Key expansion vectors include:

European Sovereignty Requirements: Data localization and sovereignty concerns create opportunities for regional deployments

Asia-Pacific Digital Transformation: Rapid cloud adoption in markets like India, Southeast Asia, and Japan

Industry Vertical Penetration: Healthcare, financial services, and government sectors with unique compliance needs

Channel Partnerships: Leveraging systems integrators and regional value-added resellers to accelerate market entry

4. Vertical Industry Solutions and Specialized Offerings

While Datadog has historically maintained a horizontal platform strategy, opportunities exist to develop specialized solutions for specific industries with unique monitoring and compliance requirements:

High-Potential Vertical Markets

Industry

Specific Needs

Datadog Opportunity

Healthcare

HIPAA compliance, patient data monitoring, medical device connectivity

PHI-specific logging, specialized compliance dashboards

Financial Services

Transaction monitoring, fraud detection, regulatory reporting

Real-time transaction tracing, audit trail guarantees

Retail/E-commerce

Customer journey analytics, inventory systems, POS monitoring

Integrated digital experience and inventory correlation

Manufacturing/IoT

Edge device monitoring, industrial equipment telemetry

Edge-to-cloud observability, predictive maintenance

The development of industry-specific solutions could command premium pricing while reducing competitive threats from generalist platforms. Moreover, specialized offerings create opportunities for professional services revenue and deeper customer relationships.

5. Strategic Acquisitions and Product Portfolio Enhancement

Datadog’s strong balance sheet, with $4.1 billion in cash and securities as of Q3 2025, provides substantial capacity for strategic acquisitions. The company’s recent acquisition of Eppo for approximately $220 million demonstrates management’s willingness to deploy capital for strategic expansion.

M&A Strategic Rationale

The Eppo acquisition illustrates Datadog’s acquisition criteria and strategy:

Expanding into adjacent markets (feature flagging and experimentation)

Acquiring specialized expertise and technology

Accelerating product development timelines

Eliminating potential competitive threats early

Future acquisition targets might include:

Specialized AI/ML monitoring platforms

Security information and event management (SIEM) capabilities

Cost optimization and FinOps tools

Incident management and on-call platforms

Business intelligence and data visualization capabilities

Each acquisition serves dual purposes: immediately expanding addressable market and cross-selling opportunities, while also preemptively neutralizing competitive threats. For investors, strategic M&A represents a catalyst for growth acceleration, though execution risk must be carefully evaluated.

THREATS: External Challenges and Risk Factors

1. Intensifying Competition from Established and Emerging Players

The observability market has attracted intense competitive interest, with well-funded adversaries attacking Datadog’s position from multiple angles. Competition manifests across several dimensions:

Competitive Threat Matrix

Competitor Type

Examples

Competitive Strategy

Risk to Datadog

Incumbent APM Vendors

Dynatrace, New Relic

All-in-one platforms with strong enterprise relationships

Direct feature and pricing competition

Log Management Specialists

Splunk (Cisco)

Deep logging/security capabilities with observability expansion

Security and log management displacement

Cloud Native Players

Grafana, Prometheus ecosystem

Open-source foundations with commercial offerings

Low-end disruption, pricing pressure

Cloud Provider Tools

AWS CloudWatch, Azure Monitor, Google Cloud Operations

Native integration and bundled pricing

Cloud provider lock-in effects

AI-Focused Entrants

Emerging startups

Specialized AI observability features

Niche displacement in fast-growing segments

Dynatrace has invested heavily in AI-powered automation and boasts strong performance in the Gartner rankings. New Relic has repositioned around consumption-based pricing that may be more attractive to cost-conscious customers. Meanwhile, the Grafana ecosystem provides capable open-source alternatives that resonate with engineering-led organizations.

Competitive Pressure Points

Pricing: Aggressive discounting from challengers seeking share

Feature Parity: Competitors closing capability gaps through rapid development

Bundling: Cloud providers offering "good enough" monitoring at no extra cost

Specialization: Vertical-focused solutions capturing niche use cases

The proliferation of alternatives creates deal risk at renewal time. As customers face budget scrutiny, competitive proposals provide leverage to demand concessions or justify vendor switches. While Datadog’s integrated platform creates switching friction, no position is unassailable.

2. Macroeconomic Headwinds and Enterprise IT Budget Pressures

Despite Datadog’s strong Q3 2025 performance, macroeconomic conditions continue to create headwinds for software spending. Several trends warrant investor attention:

Economic Environment Impacts

The company has acknowledged that customers are implementing optimization initiatives to control costs, leading to slower usage growth among existing customers. While new customer acquisition has partially offset this effect, sustained economic uncertainty could amplify these pressures.

Economic Scenario

Impact on Datadog

Probability

Risk Severity

Prolonged High Interest Rates

Reduced cloud migration velocity, extended sales cycles

Medium-High

Moderate

Technology Sector Recession

Budget cuts, project deferrals, aggressive optimization

Low-Medium

High

Gradual Recovery

Improving conditions through 2026

Medium

Low

Rapid Expansion

Accelerated digital transformation spending

Low-Medium

None (positive)

The company’s exposure to technology sector customers creates concentration risk. If technology companies that have driven recent growth face challenges, the impact on Datadog could be disproportionate. Conversely, expansion into more diverse industry verticals would provide natural hedging.

3. Open Source Alternative Adoption and Commoditization Pressure

The observability market faces ongoing commoditization pressure from open-source alternatives that have achieved remarkable maturity. The combination of Prometheus for metrics, Grafana for visualization, Elasticsearch for logs, and Jaeger for tracing provides a competent monitoring stack at zero software cost.

Open Source Ecosystem Maturity

Component Open Source Maturity Competition

─────────────────────────────────────────────────────────────

Metrics Prometheus High Direct feature parity

Visualization Grafana Very High Superior in some areas

Logs Elasticsearch High Strong capabilities

Tracing Jaeger, Tempo Medium-High Catching up rapidly

While the total cost of ownership for open-source stacks includes operational overhead, skilled engineering teams can achieve significant savings. The trend toward platform engineering and internal developer platforms makes self-hosting more attractive for large enterprises with technical sophistication.

Datadog’s counter-strategy emphasizes managed service convenience, integrated workflows, and specialized capabilities like AI observability that open-source alternatives lack. However, the persistent pricing pressure from open-source alternatives constrains Datadog’s pricing power and margin expansion potential.

4. Data Privacy and Regulatory Compliance Complexity

As a platform that ingests and processes massive volumes of operational data, Datadog faces increasing regulatory scrutiny regarding data handling, privacy, and sovereignty. Multiple regulatory regimes create complex compliance obligations:

Regulatory Landscape Challenges

Regulation

Geographic Scope

Key Requirements

Datadog Impact

GDPR

European Union

Data localization, right to deletion, consent requirements

Regional infrastructure requirements, feature development costs

CCPA/CPRA

California, expanding

Consumer data rights, opt-out mechanisms

Operational complexity, potential liability

Data Sovereignty Laws

Various (China, Russia, etc.)

In-country data storage and processing

Market access barriers, infrastructure duplication

Industry-Specific (HIPAA, PCI-DSS, etc.)

U.S. and global

Specialized handling of sensitive data

Compliance certification costs, feature constraints

The challenge extends beyond compliance costs. Regulatory fragmentation requires region-specific infrastructure deployments, multiplying operational complexity. Additionally, heightened scrutiny of data handling practices creates reputational risk if breaches or mishandling incidents occur.

Datadog has made progress on compliance, including the GovRAMP authorization initiative and various certifications. However, the regulatory environment continues evolving, and unexpected requirements could necessitate significant architectural changes or feature limitations.

5. Technology Disruption and Platform Architecture Shifts

The observability market exists within a broader technology ecosystem subject to disruptive change. Several emerging trends could fundamentally alter requirements or create new competitive threats:

Potential Disruptive Forces

Edge Computing and Distributed Architectures: As computing moves closer to data sources and end-users, traditional cloud-centric observability models may require fundamental rethinking. Edge deployments create challenges for centralized data aggregation and analysis, potentially requiring new architectural approaches.

AI-Powered Autonomous Operations: Advanced AI systems that automatically detect and remediate issues could reduce the need for human-facing observability tools. While Datadog is investing in AI capabilities like Bits AI, truly autonomous systems could commoditize aspects of the observability stack.

eBPF and Kernel-Level Instrumentation: Technologies like eBPF (extended Berkeley Packet Filter) enable observability with zero application instrumentation. This shift could disintermediate traditional APM approaches, though Datadog has been adopting these technologies in its own stack.

Traditional Instrumentation: eBPF-Based Approach:

────────────────────────────────────────────────────────

Application code modification No application changes required

Language-specific agents Language-agnostic observation

Performance overhead Minimal performance impact

Deployment complexity Simplified deployment

Serverless and Function-as-a-Service Evolution: As serverless computing matures, monitoring requirements evolve. Ephemeral execution environments, sub-second function invocations, and event-driven architectures create unique observability challenges that may favor purpose-built solutions over general platforms.

While Datadog has demonstrated adaptability to technology transitions, the pace of change creates ongoing execution risk. Missing a fundamental shift or being slow to adapt could enable competitors to gain share in emerging segments.

Strategic Implications for Investors

Investment Thesis Framework

Evaluating Datadog as a potential investment requires synthesizing the SWOT elements into a coherent framework. The following scenarios outline potential future trajectories:

Bull Case: AI-Driven Acceleration

In this scenario, AI workload proliferation accelerates faster than anticipated, with enterprises moving rapidly from experimentation to production deployments. Datadog’s specialized AI observability capabilities enable it to capture disproportionate market share, driving revenue growth acceleration to 30-35% annually through 2026-2027. The company successfully expands internationally while maintaining operating margins above 25%, generating substantial free cash flow that funds strategic acquisitions and shareholder returns.

Key Catalysts:

AI-native customer revenue exceeding 20% of total by end of 2026

Successful international expansion adding 5+ points to growth rate

Strategic acquisitions that expand TAM without margin dilution

Net revenue retention expanding above 125% as multi-product adoption accelerates

Base Case: Steady Growth with Gradual Margin Expansion

The most likely scenario involves Datadog maintaining revenue growth in the 22-28% range through 2026, with gradual operating margin expansion to 25-27% as the company achieves greater scale. AI observability contributes meaningfully but doesn’t transform growth trajectory dramatically. Competition intensifies but Datadog defends market position through platform advantages and execution consistency. Macroeconomic conditions gradually improve, reducing optimization headwinds.

Key Characteristics:

Revenue reaching $4.5-4.8 billion in 2026

Free cash flow margins sustaining in 23-26% range

Customer count growing at 8-12% annually with stable net retention

Operating efficiency improvements offsetting competitive pricing pressure

Bear Case: Margin Compression and Growth Deceleration

In the pessimistic scenario, intensifying competition forces aggressive pricing concessions while macroeconomic headwinds persist longer than expected. Large customers leverage competitive alternatives to extract discounts, compressing margins. Open-source alternatives gain enterprise traction. Growth decelerates to high-teens percentage rates while operating margins compress below 20%. The market re-rates growth-at-scale multiples downward.

Key Risk Factors:

Major customer losses to competitors or open-source alternatives

Pricing pressure leading to gross margin deterioration below 78%

AI observability opportunity maturing slower than anticipated

Regulatory changes requiring costly platform modifications

Valuation Considerations

For investors, determining appropriate valuation multiples requires considering Datadog’s growth, profitability, and competitive position:

Comparative Valuation Framework

Metric

Datadog

Growth SaaS Peers (Avg)

Enterprise Software (Avg)

Revenue Growth Rate

~25-28%

~20-25%

~12-18%

Free Cash Flow Margin

~24%

~15-20%

~25-30%

Net Revenue Retention

~120%

~115-120%

~105-110%

Rule of 40 Score

~47-52

~40-45

~35-40

Datadog’s Rule of 40 score (revenue growth rate plus free cash flow margin) of approximately 50 places it in the top quartile of enterprise software companies, justifying premium valuation relative to slower-growing or less profitable peers.

Key Valuation Drivers

Positive Factors:

- Exceptional growth and profitability balance

- Large and expanding TAM

- Strong competitive position with multiple moats

- Secular tailwinds from cloud and AI adoption

Risk Factors:

- High absolute valuation multiples vulnerable to multiple compression

- Execution risk in maintaining growth at scale

- Competitive intensity and pricing pressure

- Macroeconomic sensitivity

Portfolio Positioning Recommendations

For investors considering Datadog as a portfolio holding, several factors inform appropriate position sizing:

Conservative Investors (Risk Tolerance: Low to Moderate)

Rationale: Quality business with strong fundamentals but elevated valuation risk

Entry Strategy: Dollar-cost averaging on weakness, avoid chasing

Monitoring: Quarterly earnings, net retention trends, competitive developments

Growth-Oriented Investors (Risk Tolerance: Moderate to High)

Rationale: Multi-year growth runway with AI opportunity offering asymmetric upside

Entry Strategy: Core position with tactical additions on momentum

Monitoring: AI customer metrics, product innovation velocity, international expansion progress

Aggressive Growth Investors (Risk Tolerance: High)

Rationale: Best-in-class operator in massive addressable market with AI tailwind

Entry Strategy: Full position rapidly, potentially using options for leverage

Monitoring: Detailed analysis of customer cohort dynamics, competitive positioning shifts

Risk Mitigation Strategies

Investors holding or considering Datadog positions should implement monitoring frameworks to identify emerging risks early:

Key Performance Indicators to Monitor

Financial Health Metrics

Metric

Warning Threshold

Action if Breached

Revenue Growth Rate

Falls below 20% YoY

Reassess growth thesis, reduce position

Net Revenue Retention

Declines below 115%

Examine customer health and competitive losses

Free Cash Flow Margin

Falls below 20%

Evaluate operating efficiency and margin trajectory

Customer Acquisition Efficiency

Payback period exceeds 24 months

Question scalability of growth model

Operational Indicators

Metric

Warning Signal

Interpretation

$100K+ Customer Growth

Decelerates to single digits

Large customer momentum slowing

Multi-Product Adoption

Stagnates or declines

Platform strategy weakening

AI-Native Revenue %

Growth rate decelerates

AI opportunity materializing slower than expected

Gross Margin

Compression exceeding 100 basis points annually

Infrastructure costs or competitive pricing pressure

Competitive Intelligence Monitoring

Investors should track competitor developments that could signal shifting competitive dynamics:

Product Releases: Major feature announcements from Dynatrace, New Relic, or emerging players

Pricing Changes: Aggressive discounting or pricing model innovations from competitors

Customer Wins: High-profile customers switching from Datadog to alternatives

Market Share Data: Independent research on relative platform adoption

Analyst Reports: Gartner, Forrester, and IDC positioning updates

Macroeconomic Indicators

Given Datadog’s sensitivity to enterprise IT spending, several economic indicators provide early warning signals:

Leading Indicators:

- Technology sector employment trends

- Cloud infrastructure spending growth (AWS, Azure, GCP revenue)

- Software spending surveys (e.g., Gartner IT spending forecasts)

- Customer optimization commentary in earnings calls

Lagging Indicators:

- Datadog's own revenue growth rate

- Net retention rate trends

- Customer churn disclosures

My Final Thoughts: Assessment and Forward Outlook

Datadog occupies an enviable position at the nexus of multiple technology megatrends, with a proven platform, strong customer relationships, and meaningful competitive advantages. The company’s comprehensive SWOT profile reveals an organization with substantial strengths, manageable weaknesses, compelling opportunities, and identifiable but addressable threats.

Synthesis of Key Findings

The most critical takeaway for investors is that Datadog represents a high-quality growth business trading at growth stock valuations. The company’s ability to sustain 25%+ revenue growth while generating substantial free cash flow distinguishes it from many growth-stage software companies. This balanced profile reduces downside risk while preserving meaningful upside potential.

The AI observability opportunity could prove transformative, potentially accelerating growth and expanding addressable markets significantly. However, investors should avoid extrapolating current AI-native customer growth rates indefinitely, as some deceleration is inevitable as the cohort matures. The question is whether AI workloads represent a temporary boost or a sustained structural tailwind through the end of the decade.

Critical Success Factors for 2026

Several factors will determine whether Datadog can sustain its premium valuation and market leadership through 2026:

AI Observability Leadership: Maintaining technological edge as competitors introduce AI monitoring capabilities

International Expansion Execution: Successfully penetrating Asia-Pacific and emerging markets without margin dilution

Pricing and Value Perception: Addressing customer cost concerns while preserving unit economics

Platform Integration: Deepening product integration to increase switching costs and multi-product adoption

Competitive Defense: Fending off challengers without aggressive pricing concessions

Investment Verdict Framework

For most investors, Datadog merits consideration as a core holding within a growth-oriented technology portfolio, with position sizing calibrated to individual risk tolerance and conviction levels. The company’s combination of growth, profitability, and market position create an attractive risk-reward profile for patient investors with multi-year time horizons.

However, near-term volatility should be expected. Quarterly results will likely show variability as macroeconomic conditions evolve, and the stock may experience significant drawdowns during broader market corrections given its high valuation multiples. Investors prone to emotional decision-making or those requiring capital preservation should consider smaller positions or alternative investment vehicles.

The forward path through 2026 and beyond will test management’s ability to navigate intensifying competition while sustaining innovation velocity and operational efficiency. For investors willing to accept execution risk and valuation volatility, Datadog offers exposure to secular growth trends in cloud computing, artificial intelligence, and digital transformation that will likely define the next decade of enterprise technology.

As enterprises continue their inexorable migration toward cloud-native architectures and AI-augmented operations, the demand for sophisticated observability platforms will only intensify.

Whether Datadog can capitalize fully on this opportunity while defending against competitive incursions will determine its ultimate success as an investment.

Our SWOT analysis framework provided here offers investors a structured approach to monitoring progress and adjusting portfolio positions as new information emerges.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with financial advisors before making investment decisions.