Intel - SWOT Analysis Report (2026)

Intel is on one of the most ambitious transformation efforts in its history. Let's examine its internal capabilities and external market dynamics.

Intel Corporation $INTC ( ▲ 6.51% ) is embarking on one of the most ambitious transformation efforts in the semiconductor industry’s history.

After decades of dominance in the microprocessor market, the company faces unprecedented competition while simultaneously pursuing a bold strategy to become a leading-edge foundry service provider.

For investors, understanding Intel’s position requires a deep examination of its internal capabilities and external market dynamics.

As of November 2025, Intel’s market capitalization stands at approximately $175.8 billion, representing a complex valuation story. The stock has demonstrated remarkable resilience in 2025, surging more than 90% from its 2024 lows, yet it remains well below its historical highs. This recovery reflects both improved operational execution and significant external support, including substantial government backing and strategic partnerships.

The semiconductor industry itself is experiencing a period of unprecedented growth, driven primarily by artificial intelligence, data center expansion, and the proliferation of connected devices.

According to Deloitte, chip sales are set to soar in 2025, led by generative AI and data center build-outs. Intel’s ability to capture this growth while transforming its business model will determine its long-term investment viability.

Table of Contents

1. Company Overview and Recent Performance

Corporate Structure and Leadership

Intel Corporation, founded in 1968, has been a cornerstone of the American semiconductor industry for over five decades. The company’s headquarters remain in Santa Clara, California, where it continues to drive innovation in computing technologies. As of November 2025, Intel operates through several key business segments:

Primary Business Segments:

- Client Computing Group (CCG): Desktop and mobile processors

- Data Center and AI (DCAI): Server processors and AI accelerators

- Network and Edge (NEX): Infrastructure and networking solutions

- Intel Foundry Services (IFS): Contract manufacturing for external clients

- Mobileye: Autonomous driving technologies

The company underwent a significant leadership transition in late 2024 and early 2025. After Pat Gelsinger’s departure as CEO in December 2024, Intel appointed Lip-Bu Tan as CEO in March 2025. Tan brings extensive semiconductor industry experience, having previously led Cadence Design Systems for 25 years. His appointment signals Intel’s commitment to foundry success and manufacturing excellence.

Recent Financial Performance

Intel’s third-quarter 2025 results, released on October 23, 2025, marked a turning point in the company’s turnaround efforts:

Financial Metric

Q3 2025

Q3 2024

Year-over-Year Change

Revenue

$13.7B

$13.3B

+3%

Gross Margin (GAAP)

38.2%

15.0%

+23.2 percentage points

Gross Margin (Non-GAAP)

40.0%

35.7%

+4.3 percentage points

Operating Margin

5.0%

(68.2%)

+73.2 percentage points

Net Income

$4.1B

$(16.6B)

Positive turnaround

EPS (Non-GAAP)

$0.23

-

Above guidance

The Q3 2025 results demonstrated several encouraging trends. Revenue growth of 3% year-over-year may appear modest, but it represents the third consecutive quarter of revenue growth after a prolonged decline. More importantly, the gross margin improvement of over 23 percentage points year-over-year reflects both improved product mix and the benefits of cost-reduction initiatives.

The non-GAAP gross margin of 40% exceeded company guidance by 4 percentage points, driven by higher revenue, favorable product mix, and lower inventory reserves. This margin expansion is particularly significant for investors, as it demonstrates Intel’s ability to improve profitability even in a highly competitive environment.

Strategic Transformation Under New Leadership

CEO Lip-Bu Tan has implemented a comprehensive restructuring strategy focused on four key pillars:

Tan's Turnaround Strategy:

1. Financial Discipline

- Aggressive cost reduction targeting $10 billion+ in annual savings

- Workforce reduction from 109,900 (end of 2024) to 88,400 (September 2025)

- Suspension of dividend to redirect capital to manufacturing investments

- Focus on projects with 50%+ gross margins

2. Foundry Transformation

- Establishment of Intel Foundry as independent subsidiary

- Pursuit of external customers for 18A and future nodes

- Strategic partnerships with Microsoft, Amazon, and others

- Potential minority stake sale to external investors

3. Technology Leadership

- Accelerated development of 18A process technology

- Five nodes in four years roadmap execution

- Advanced packaging capabilities investment

- AI-focused product development

4. Operational Excellence

- Simplified organizational structure

- Customer-centric culture transformation

- Supply chain optimization

- Quality and execution improvements

According to Fortune’s coverage, Tan’s focus on balance sheet discipline has been particularly noteworthy. Since his appointment, Intel has launched a sweeping restructuring plan that anticipates cutting approximately 21,000 to 25,000 positions, representing roughly 20% of the workforce. While painful, these measures are designed to create a leaner, more agile organization capable of competing with TSMC and Samsung in both technology and cost structure.

2. Strengths: Intel’s Competitive Advantages

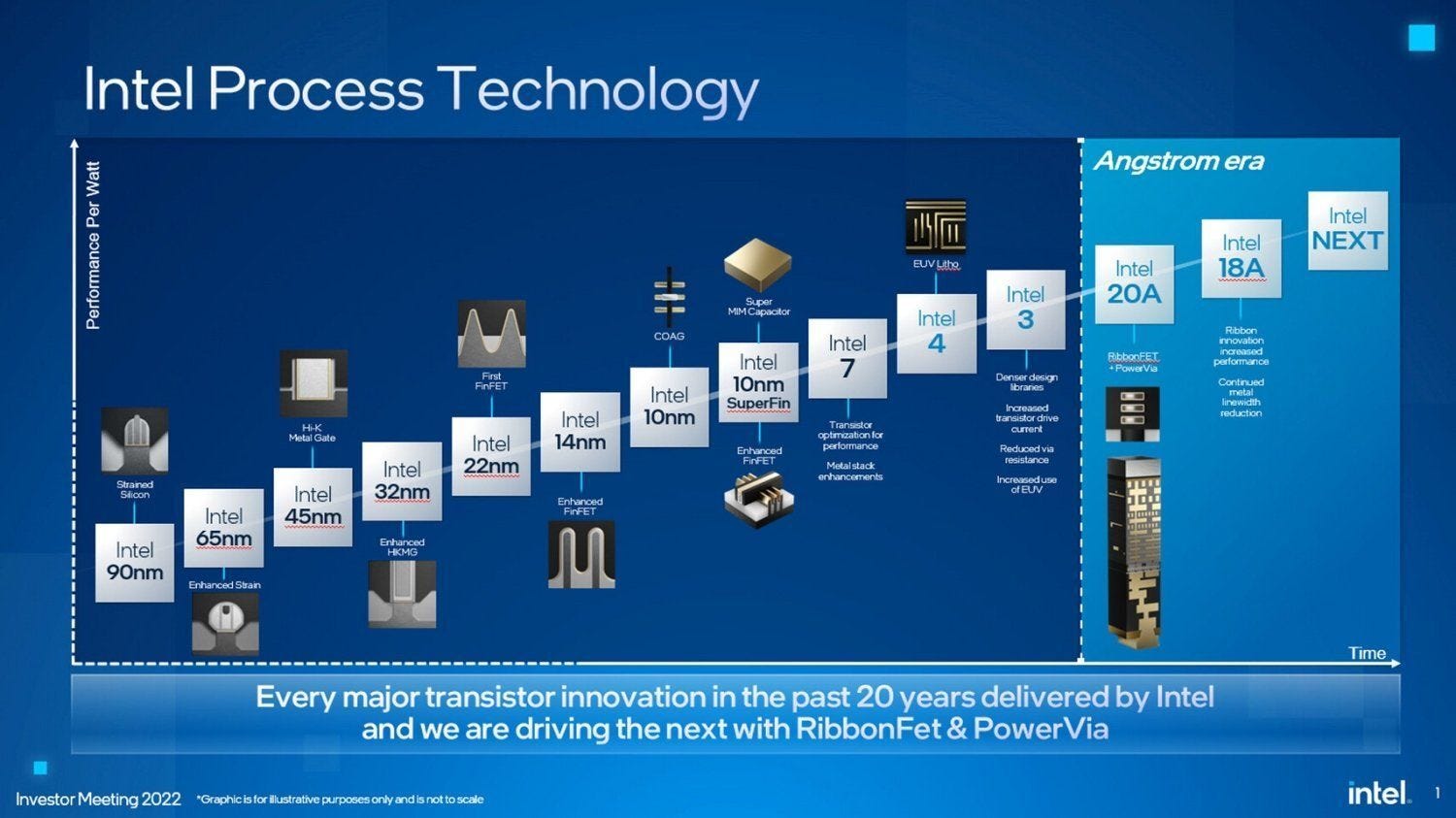

2.1 Advanced Manufacturing Technology and 18A Process Node

Intel’s most significant strength heading into 2026 is its ambitious manufacturing roadmap, centered around the 18A process technology. The 18A node represents Intel’s return to manufacturing leadership and incorporates two groundbreaking innovations:

RibbonFET Technology: Intel’s implementation of Gate-All-Around (GAA) transistors, known internally as RibbonFET, represents a fundamental shift in transistor architecture. Unlike traditional FinFET designs, RibbonFET wraps the gate material completely around the channel, providing superior electrostatic control. This architecture enables:

15% better performance-per-watt compared to Intel 3

30% greater transistor density improvement

Enhanced power efficiency for mobile and edge applications

Better scaling characteristics for future nodes

PowerVia Backside Power Delivery: Intel’s PowerVia technology, the industry’s first backside power delivery network in high-volume manufacturing, separates power delivery from signal routing. This innovation:

Reduces IR drop by placing power delivery on the backside of the wafer

Enables denser routing on the front side for logic and signals

Improves performance by optimizing power distribution

Reduces design complexity for advanced chips

According to Tom’s Hardware’s analysis, Intel’s 18A production timeline puts it ahead of TSMC’s competing N2 technology in terms of market introduction. Intel began risk production of 18A in April 2025, with volume manufacturing ramping in late 2025. This timing advantage, even if temporary, provides Intel with a critical opportunity to demonstrate foundry competitiveness.

Forbes reported that 18A offers up to 15% better performance-per-watt and 30% greater transistor density compared to Intel 3. For foundry customers, these metrics directly translate to better product performance and lower power consumption—key selling points in the competitive foundry market.

2.2 Comprehensive Product Portfolio Across Multiple Segments

Unlike pure-play foundries such as TSMC, Intel maintains a diversified product portfolio that provides multiple revenue streams and reduces dependence on any single market segment. This diversification offers resilience against market cyclicality:

Business Segment

Key Products

Market Position

2025 Revenue Contribution

Client Computing

Core Ultra, Core processors

#2 behind AMD in some segments

~50% of total revenue

Data Center & AI

Xeon processors, Gaudi accelerators

Competing with AMD, NVIDIA

~30% of total revenue

Network & Edge

IPU, FPGA, infrastructure chips

Strong in telco/edge

~10% of total revenue

Foundry Services

Contract manufacturing

Emerging competitor to TSMC

<5% of total revenue

Mobileye

ADAS and autonomous driving

Market leader in ADAS

~3-5% of total revenue

Client Computing Strength: Intel’s Client Computing Group delivered strong performance in Q3 2025, with revenue growth driven by the Core Ultra 200S series desktop processors. The group’s revenue reached $13.7 billion, representing solid execution in a seasonally strong period. The introduction of AI PC capabilities with integrated neural processing units (NPUs) has created a new product category where Intel maintains technical leadership.

Data Center Growth Potential: While Intel has lost market share to AMD in the data center space, the company maintains significant installed base advantages and customer relationships. The upcoming Clearwater Forest Xeon 6+ processor, built on 18A and targeting launch in H1 2026, represents Intel’s most power-efficient server CPU to date. Designed around dense E-cores, Clearwater Forest specifically targets hyperscale cloud providers and edge deployments where power efficiency is paramount.

AI Accelerator Portfolio: Intel’s Gaudi 3 AI accelerators, featuring 128GB of HBM2e memory, provide an alternative to NVIDIA’s dominant GPUs. While market share remains small, partnerships with Dell, IBM Cloud, and other vendors are expanding Gaudi 3’s reach. For cost-conscious customers seeking alternatives to NVIDIA’s premium pricing, Gaudi 3 offers competitive training and inference performance at more attractive price points.

2.3 Unprecedented Government Support and Strategic Partnerships

Intel benefits from extraordinary government support that no other U.S. semiconductor company can match. This backing stems from Intel’s strategic importance to national security and semiconductor supply chain resilience:

CHIPS Act Funding: In a historic agreement announced in August 2025, Intel reached a revised deal with the U.S. government that includes:

$8.9 billion in direct equity investment (10% government ownership stake)

$2.2 billion previously received in grants

Additional $11 billion in low-interest loans available

Up to 25% investment tax credits for manufacturing facilities

Total potential government support exceeding $20 billion

This government partnership provides Intel with several strategic advantages:

Government Support Benefits:

Financial Advantages:

- Reduces capital requirements for fab construction

- Lowers cost of capital through subsidized financing

- Provides cash flow stability during transition period

- Enables acceleration of manufacturing investments

Strategic Advantages:

- Validates Intel's importance to U.S. semiconductor strategy

- Creates barriers for overseas competition

- Positions Intel for secure government contracts

- Enhances credibility with foundry customers

Operational Advantages:

- Accelerates 18A and future node development

- Supports advanced packaging investments

- Enables U.S.-based manufacturing expansion

- Facilitates workforce development programs

Defense and Secure Manufacturing: Intel received a $3 billion federal grant specifically for developing chip manufacturing infrastructure for the U.S. defense industry. This Secure Enclave program ensures Intel’s long-term role in producing semiconductors for sensitive military and intelligence applications, providing a stable, high-margin revenue stream insulated from commercial market fluctuations.

Strategic Industry Partnerships: Beyond government support, Intel has secured critical partnerships that validate its foundry strategy:

Microsoft: Committed to using Intel Foundry for manufacturing custom Azure AI chips on 18A

Amazon Web Services: Partnership for manufacturing custom silicon at Intel Foundry

NVIDIA: Unexpected alliance where NVIDIA may use Intel Foundry for future products

SoftBank: Partnership creating an AI chip venture with substantial investment

These partnerships provide both revenue and credibility. Landing customers like Microsoft and potentially NVIDIA demonstrates that Intel Foundry’s technology and service model can compete with TSMC, even as Intel rebuilds its manufacturing capabilities.

2.4 Integrated Design and Manufacturing Model (IDM 2.0)

Intel’s IDM 2.0 strategy, which combines internal chip design with foundry services, creates unique advantages:

Vertical Integration Benefits: As both a chip designer and manufacturer, Intel can optimize designs specifically for its manufacturing processes, potentially achieving better performance and yields than fabless competitors using third-party foundries. This co-optimization of design and process technology has historically been one of Intel’s greatest strengths.

Intellectual Property Depth: Intel owns extensive patent portfolios covering microarchitecture, manufacturing processes, packaging technologies, and software optimization. This IP creates competitive moats and licensing revenue opportunities. The company’s x86 instruction set architecture, while facing competition from ARM, remains the dominant standard for PCs and servers with deep software ecosystem support.

Advanced Packaging Leadership: Intel has invested heavily in advanced packaging technologies including:

Foveros: 3D chip stacking technology used in products like Meteor Lake and Panther Lake

EMIB (Embedded Multi-die Interconnect Bridge): High-bandwidth die-to-die connectivity

Co-EMIB: Combination of Foveros and EMIB for complex multi-die designs

These packaging capabilities enable Intel to create heterogeneous computing solutions that combine different process nodes and chip types, providing flexibility that pure-play foundries cannot easily replicate without similar design expertise.

Image source: semiwiki.com

2.5 U.S.-Based Manufacturing as Geopolitical Advantage

The concentration of advanced semiconductor manufacturing in Taiwan creates supply chain vulnerabilities that have become increasingly apparent. Intel’s extensive U.S. manufacturing footprint provides several advantages:

Geographic Diversification: Intel operates advanced fabs in:

Arizona (Fab 52, fully operational with 18A)

Oregon (Hillsboro, Intel’s primary R&D center)

New Mexico (Fab 9, recently opened)

Ireland (Fab 34, producing Intel 4)

This geographic diversification, particularly the U.S.-based facilities, appeals to customers concerned about geopolitical risks associated with Taiwan-based manufacturing. For defense, aerospace, and critical infrastructure customers, U.S.-manufactured chips provide supply chain security that offshore alternatives cannot match.

Regulatory Advantages: As restrictions on semiconductor exports to China and other countries tighten, Intel’s U.S. manufacturing provides clearer export control compliance. Customers can more easily navigate International Traffic in Arms Regulations (ITAR) and Export Administration Regulations (EAR) when working with U.S.-based manufacturing.

3. Weaknesses: Internal Challenges and Limitations

3.1 Foundry Business Remains Unproven and Loss-Making

Despite significant investments and strategic importance, Intel Foundry Services remains an unproven business with substantial execution risk. The scale of this challenge cannot be understated:

Financial Losses: Intel Foundry continues to generate significant operating losses. According to analysis from SemiWiki, Intel’s external foundry revenue was only $35 million in Q3 2025, down significantly from previous years. These anemic revenues stand in stark contrast to the billions Intel is investing in foundry infrastructure.

The foundry business model requires:

Foundry Success Requirements:

Financial Requirements:

- Sustained multi-billion dollar capital investments

- 5-7 year payback periods on new fabs

- Ability to operate at low margins during customer ramps

- Working capital for long-lead time orders

Technical Requirements:

- Process technology competitive with TSMC N3/N2

- Yields matching or exceeding 90-95% for mature products

- Design ecosystem supporting multiple PDKs and IP libraries

- Reliability and defect density meeting automotive/industrial specs

Operational Requirements:

- Customer-centric culture replacing product-centric approach

- Foundry-specific pricing, contracts, and business terms

- Supply chain flexibility for diverse customer needs

- Manufacturing capacity allocation balancing internal/external demands

Cultural Transformation Challenges: Intel has operated for decades as an integrated device manufacturer, prioritizing its own products over external customers. Transforming to a foundry service provider requires fundamental cultural change. Foundry customers expect:

Transparent communication about capacity, yields, and schedules

Willingness to manufacture competitors’ products

Flexible contract terms and pricing models

IP protection guarantees

Technology transfer and design support

Creating this customer-centric culture while maintaining internal design operations creates inherent conflicts. Internal business units may resist sharing manufacturing capacity with external customers, particularly when Intel’s own product launches are at risk.

Competitive Positioning: Intel enters the foundry business facing entrenched competition. TSMC controls approximately 60% of the global foundry market, with Samsung holding another 12%. Both competitors have decades of foundry operating experience, established customer relationships, and proven execution records. Intel must overcome significant skepticism from potential customers who remember Intel’s historical reliability issues and delayed process technology transitions.

3.2 Market Share Losses Across Key Segments

Intel has experienced erosion of market share across multiple critical business segments:

Desktop and Laptop Processors: AMD has made substantial inroads into Intel’s historical stronghold. In desktop processors, AMD’s Ryzen processors have captured significant enthusiast and gaming market share based on competitive performance and pricing. While Intel maintains volume leadership in laptops, AMD’s mobile Ryzen processors have gained OEM design wins and consumer mindshare.

Server and Data Center: The data center market represents Intel’s most significant share loss. From near-monopoly position in server CPUs a decade ago, Intel now faces fierce competition:

Data Center Market Segment

Intel Position

Key Competitors

Trend

General Purpose Servers

~65-70% share

AMD EPYC growing rapidly

Declining

Cloud/Hyperscale

~50-55% share

AMD, ARM-based alternatives

Under pressure

AI Training

<5% share

NVIDIA dominates with 90%+

Struggling

AI Inference

~20-25% share

NVIDIA, AMD, custom ASICs

Competitive

Edge/Telco

~40-45% share

AMD, Marvell, Ampere

Relatively stable

According to AMD’s Q3 2025 market data, AMD continues to gain data center share quarter-over-quarter, driven by EPYC processor performance advantages in multi-threaded workloads and competitive pricing. Intel’s Xeon processors have struggled to match AMD’s core counts and performance-per-watt metrics.

AI Accelerators: Intel’s weakness in AI accelerators represents one of its most significant strategic challenges. NVIDIA controls over 90% of the AI training market and a substantial portion of inference. Intel’s Gaudi accelerators, despite technical capabilities, have gained minimal traction:

Gaudi 3 revenues estimated at only $500 million for 2025

NVIDIA’s data center revenue: approximately $40 billion in 2025

Intel lacks the CUDA software ecosystem that locks customers to NVIDIA

Enterprise reluctance to adopt non-NVIDIA solutions for AI workloads

3.3 Manufacturing Delays and Execution Concerns

Intel’s manufacturing execution has been inconsistent, creating credibility issues:

Historical Process Node Delays: Intel’s 10nm process (later renamed Intel 7) experienced years of delays, allowing competitors to leapfrog Intel’s technology leadership. The 7nm process (Intel 4) similarly faced delays. While recent node transitions (Intel 4, Intel 3, and the upcoming 18A) appear on track, investors remain skeptical about Intel’s ability to execute its aggressive roadmap.

Yield Challenges: Reports indicate that Intel 18A yields are not expected to reach industry-standard levels until 2027. Lower yields translate directly to higher costs and reduced gross margins, particularly problematic when competing against TSMC’s mature processes with proven yields above 90%.

Quality Control Issues: Intel experienced product quality issues with certain generations, including voltage instability problems with some 13th and 14th generation processors. Such problems, while eventually resolved, damage brand reputation and create customer hesitation about adopting next-generation products.

3.4 High Cost Structure and Margin Pressure

Intel’s cost structure remains significantly higher than competitors, constraining profitability and competitive positioning:

Manufacturing Cost Disadvantages: Building and operating leading-edge fabs in the United States costs substantially more than in Taiwan or South Korea. Labor costs, regulatory requirements, and infrastructure expenses create structural cost disadvantages estimated at 20-30% compared to Asian competitors.

Gross Margin Compression: Intel’s gross margins have declined from historical levels above 60% to the 40% range in 2025. CEO Tan has implemented a policy requiring new products to achieve 50% gross margins to proceed, acknowledging that many current products fall short of this threshold. For comparison:

Company

Gross Margin (2025)

Operating Margin (2025)

NVIDIA

70-75%

55-60%

TSMC

55-60%

45-50%

Intel

38-40%

5-10%

AMD

50-53%

15-20%

These margin disadvantages reflect both cost structure issues and competitive pricing pressure. Intel must price products aggressively to compete with AMD, limiting pricing power even when products are competitive on technical merits.

R&D Intensity: While necessary for technology leadership, Intel’s R&D spending as a percentage of revenue remains high. The company spent approximately $4.4 billion in R&D and SG&A in Q3 2025 alone, representing nearly one-third of quarterly revenue. Maintaining this investment level while rebuilding profitability creates significant financial tension.

3.5 Leadership Instability and Strategic Uncertainty

Intel has experienced significant leadership turbulence that creates uncertainty about strategic direction:

CEO Transitions: The company went through two CEO transitions in six months, from Pat Gelsinger’s sudden departure in December 2024 through an interim co-CEO period to Lip-Bu Tan’s appointment in March 2025. Reuters reported that Gelsinger’s board removed him after losing confidence in his turnaround plan’s cost and timeline.

Strategic Direction Shifts: Different CEOs have emphasized different priorities, creating confusion about Intel’s long-term strategy:

Former CEO Brian Krzanich (2013-2018): Mobile and IoT focus

Former CEO Bob Swan (2018-2021): Financial optimization, considered outsourcing manufacturing

CEO Pat Gelsinger (2021-2024): IDM 2.0, aggressive process roadmap, foundry services

CEO Lip-Bu Tan (2025-present): Foundry emphasis, cost discipline, operational excellence

Each transition brings revised priorities, reorganizations, and strategic reviews that delay decision-making and create employee uncertainty.

Organizational Restructuring: Intel has undergone multiple rounds of organizational changes, including:

Creation of Intel Foundry Services as a business unit (2021)

Conversion of IFS to a subsidiary (2025)

Multiple layoff rounds eliminating 35,000+ positions since 2024

Management departures across multiple business units

These disruptions, while necessary for transformation, create execution risk and distract from operational focus.

4. Opportunities: Growth Vectors for 2026 and Beyond

4.1 Artificial Intelligence Market Expansion

The AI revolution represents Intel’s most significant growth opportunity, albeit one where the company currently lags competitors. The global AI semiconductor market is projected to grow from approximately $50 billion in 2024 to over $200 billion by 2028, representing a compound annual growth rate exceeding 40%.

AI PC Market Leadership: Intel has positioned itself as the leader in AI-enabled PCs with its Core Ultra processors featuring integrated Neural Processing Units (NPUs). The company’s chips can deliver over 40 TOPS (trillion operations per second) of AI performance across CPU, GPU, and NPU, enabling on-device AI applications including:

Real-time language translation

Background blur and enhancement in video calls

AI-assisted content creation and editing

Privacy-preserving local AI processing

Intelligent power management and performance optimization

The AI PC market is in early stages, with Microsoft and Intel projecting that over 100 million AI PCs will ship in 2025, growing to the majority of PC shipments by 2027. As the technology leader in AI PC processors, Intel can capture premium pricing and strengthen its position against AMD.

Data Center AI Growth: While NVIDIA dominates AI training, the inference market remains more competitive and is growing even faster than training. Intel’s opportunities include:

Data Center AI Opportunities:

Gaudi Accelerator Expansion:

- Gaudi 3 with 128GB HBM2e targeting large language model inference

- Partnerships with Dell, IBM, Oracle expanding customer access

- Price-performance advantages over NVIDIA for specific workloads

- Focus on cost-sensitive customers and specific AI applications

Xeon CPU AI Capabilities:

- Built-in AI acceleration with AMX (Advanced Matrix Extensions)

- Attractive for hybrid workloads combining traditional and AI computing

- Lower total cost of ownership for customers with existing Xeon infrastructure

- AI inference on general-purpose processors avoiding specialized hardware

Custom AI Silicon:

- Microsoft Azure Maia chips manufactured at Intel Foundry

- Opportunity to manufacture custom AI accelerators for hyperscalers

- Design services and IP licensing for AI chip startups

- Advanced packaging enabling heterogeneous AI systems

The total addressable market for AI accelerators could exceed $100 billion by 2027. Even capturing 10-15% of this market would represent $10-15 billion in annual revenue for Intel, significantly moving the needle on overall financial performance.

4.2 Foundry Services Growth and Market Share Gains

Intel Foundry Services represents perhaps Intel’s highest-potential but highest-risk opportunity. The global semiconductor foundry market exceeded $100 billion in 2024 and continues growing at double-digit annual rates. Intel has set ambitious targets to become the world’s second-largest foundry by 2030.

18A Technology Differentiation: Intel’s 18A process provides a window of opportunity. With TSMC’s N2 process not expected in volume production until late 2026 or early 2027, Intel’s 18A offers comparable technology with faster time-to-market for customers needing cutting-edge process technology in 2025-2026. This timing advantage, combined with RibbonFET and PowerVia innovations, creates differentiation.

According to Forbes analysis, under CEO Lip-Bu Tan, Intel is working to demonstrate that Intel Foundry can be competitive in both production technology and customer service. The company has expanded its Process Design Kit (PDK) library, improved design tool support, and invested in customer-facing organizations.

Target Customer Segments: Intel Foundry is pursuing several customer categories:

Customer Type

Opportunity

Intel Advantages

Challenges

Fabless Chip Companies

Design wins from TSMC/Samsung

U.S. manufacturing, leading-edge tech

Trust, track record, capacity

Cloud Hyperscalers

Custom AI and compute chips

Partnership depth, design expertise

Competition from TSMC relationships

Automotive

Safety-critical applications

U.S./EU manufacturing, reliability

Qualification cycles, volume pricing

Defense/Aerospace

Secure supply chain

Trusted foundry status, U.S.-based

Specialized requirements, margins

AI Startups

Next-generation accelerators

Advanced packaging, design support

Financial viability of customers

Advanced Packaging Differentiation: Intel’s strength in advanced packaging technologies, including Foveros 3D stacking, provides foundry differentiation. Customers can combine chiplets manufactured on different process nodes, integrating mature I/O with cutting-edge compute logic. This heterogeneous integration capability addresses a key industry trend toward disaggregated chip designs.

4.3 Edge Computing, IoT, and 5G Infrastructure

The proliferation of connected devices and edge computing infrastructure creates substantial opportunities across Intel’s product portfolio. According to industry analyses, edge computing market with AI integration is projected to reach $83.86 billion by 2032, driven by industrial IoT, 5G deployment, and intelligent infrastructure expansion.

Edge Server and Networking Growth: Intel’s Network and Edge (NEX) business unit addresses telecommunications infrastructure, including:

5G base stations and edge data centers

Content delivery networks and edge caching

Industrial automation and manufacturing edge computing

Smart city infrastructure and sensor networks

The rollout of 5G infrastructure continues globally, with private 5G networks emerging as part of enterprise edge computing strategies. Intel’s processors, FPGAs, and SmartNICs address these applications, providing growth avenues diversified from traditional PC and server markets.

IoT Endpoint Expansion: More than 55% of all data analysis by deep neural networks is expected to occur at edge devices by 2025, up from less than 10% in 2020. Intel’s processors and accelerators for edge devices enable:

Real-time video analytics for security and retail

Predictive maintenance in industrial settings

Autonomous robots and vehicles

Smart building automation

Healthcare monitoring and diagnostics

These applications require computing power, AI acceleration, and power efficiency—areas where Intel’s technology roadmap delivers improvements.

4.4 Automotive and Autonomous Vehicle Revolution

The automotive industry is undergoing a fundamental transformation toward electric and autonomous vehicles, creating substantial semiconductor content growth. Average semiconductor content per vehicle is projected to increase from approximately $600 in 2023 to over $1,200 by 2030 for advanced vehicles.

Mobileye’s Leadership Position: Intel’s majority-owned subsidiary Mobileye remains the market leader in Advanced Driver Assistance Systems (ADAS), with over 150 million vehicles equipped with its technology. Mobileye’s EyeQ chips power driver assistance features for virtually every major automotive OEM globally.

Growth drivers for Mobileye include:

Mobileye Growth Opportunities:

ADAS Penetration:

- Regulatory requirements mandating safety features

- Consumer demand for advanced driver assistance

- Insurance incentives for safety-equipped vehicles

- Level 2+ autonomy becoming standard in premium vehicles

Autonomous Vehicle Commercialization:

- Robotaxi deployments in multiple cities

- Autonomous delivery and logistics vehicles

- L4 highway autonomy for trucks

- Licensing revenue from autonomous systems

Technology Expansion:

- Radar and LiDAR integration with camera systems

- Mapping and positioning services revenue

- Software-defined vehicle platform partnerships

- OTA update and feature subscription opportunities

At CES 2025, Intel unveiled new adaptive control solutions and next-generation discrete graphics specifically for automotive applications. The company’s strategy integrates Mobileye’s perception with Intel’s computing platforms, positioning Intel as a complete automotive solution provider.

Automotive Foundry Services: Automotive semiconductors require specialized manufacturing capabilities including:

Automotive-grade qualification (AEC-Q100) standards

Long product lifecycles spanning 10-15 years

Extreme temperature and reliability requirements

Supply chain resilience and geographic diversity

Intel Foundry’s U.S.-based manufacturing and established automotive relationships position it well for this market. Automotive chips typically use mature process nodes (28nm to 7nm), allowing Intel to monetize older fabs while addressing growing demand.

4.5 Geographic Diversification and Supply Chain Resilience

Geopolitical tensions and supply chain disruptions have elevated supply chain security as a critical factor in semiconductor sourcing decisions. Intel’s geographic diversification creates competitive advantages:

U.S. Manufacturing Expansion: Intel is investing over $50 billion in U.S. manufacturing capacity expansion, including:

Fab 52 in Arizona, fully operational with 18A technology

Fab 62 and Fab 82 in Arizona, under construction

Ohio mega-site with multiple planned fabs

New Mexico fab expansion

This U.S. capacity addresses customer demands for domestic supply and positions Intel to benefit from “Buy American” policies in federal procurement and infrastructure projects.

European Manufacturing: Intel’s manufacturing presence in Ireland, with planned expansions in Germany and Poland, positions the company for the European market’s push for supply chain independence. The European Chips Act aims to double Europe’s semiconductor manufacturing share to 20% of global production by 2030, with Intel positioned as a key beneficiary.

Strategic Customer Preferences: Major customers increasingly prioritize supply chain diversification away from Taiwan-concentrated manufacturing. For customers in defense, aerospace, telecommunications infrastructure, and automotive, Intel’s geographic diversity provides options that pure-play foundries cannot easily replicate.

5. Threats: External Risks and Competitive Pressures

5.1 Intense Competition from AMD, NVIDIA, and ARM-based Alternatives

Intel faces competitive pressure across virtually every business segment, with competitors that have momentum, technical advantages, or both:

AMD’s Sustained Technology Leadership: Advanced Micro Devices has transformed from a perennial underdog to a formidable competitor with technology and market share momentum. AMD’s advantages include:

AMD Competitive Strengths vs. Intel:

Technology Advantages:

- Chiplet architecture enabling cost-effective scaling

- Partnership with TSMC providing leading-edge manufacturing

- Competitive performance-per-watt in many segments

- Faster adoption of advanced packaging technologies

Market Position:

- Gaining desktop and laptop market share in enthusiast/gaming

- Strong momentum in data center with EPYC processors

- Growing customer relationships with cloud providers

- Brand perception of innovation and value

Strategic Flexibility:

- Fabless model enabling focus on design

- Lower capital requirements than Intel's IDM model

- Agility in responding to market changes

- Partnership ecosystem supporting rapid scaling

According to recent market data, AMD has been gaining server market share at Intel’s expense for multiple quarters consecutively. AMD EPYC processors offer compelling core counts, memory bandwidth, and power efficiency that Intel’s current Xeon lineup struggles to match.

NVIDIA’s AI Dominance: NVIDIA has established a near-monopoly position in AI training and significant strength in inference. The company’s advantages extend beyond hardware to software ecosystems, developer tools, and customer relationships. NVIDIA’s CUDA programming platform creates a powerful moat—once enterprises invest in CUDA-based AI development, switching costs become prohibitive.

Intel’s Gaudi accelerators face an uphill battle against NVIDIA’s GPU ecosystem. Even with competitive or superior price-performance, Intel must overcome enterprise reluctance to adopt non-NVIDIA solutions for mission-critical AI workloads.

ARM-based Server Competition: ARM-based server processors from companies like Ampere, AWS (Graviton), and potential future offerings from NVIDIA represent a fundamental architectural threat. ARM advantages include:

Lower power consumption than x86 for many workloads

Licensing model enabling customized designs

Growing software ecosystem support

Price-performance advantages for specific applications

While ARM servers represent only about 10% of the market in 2025, this share is growing. Cloud providers particularly favor ARM for standardized workloads where software compatibility is less critical.

5.2 TSMC’s Manufacturing Dominance and Technology Leadership

Taiwan Semiconductor Manufacturing Company remains Intel’s most formidable competitive threat in manufacturing technology and foundry services. TSMC’s dominance creates multiple challenges for Intel:

Technology Leadership: Despite Intel’s aggressive roadmap, TSMC maintains technology leadership with approximately 60% of the global foundry market. TSMC’s N3 process is in high-volume production, with N2 entering production in 2026. Key TSMC advantages include:

Factor

TSMC Position

Intel Challenge

Process Maturity

N3 in production at scale

18A just ramping

Yield Performance

>90% for mature nodes

18A yields developing

Customer Trust

Decades of proven execution

Rebuilding credibility

Capacity

>1M wafer/month leading-edge

Limited 18A capacity initially

Ecosystem

Complete IP/EDA partnerships

Building foundry ecosystem

Customer Relationships: TSMC has deep, longstanding relationships with virtually every major fabless semiconductor company, including Apple, NVIDIA, AMD, Qualcomm, and Broadcom. These customers have integrated TSMC processes deeply into their design flows, product roadmaps, and manufacturing strategies. Convincing them to adopt Intel Foundry requires overcoming substantial switching costs and relationship inertia.

Geographic Concentration Risk vs. Reality: While Taiwan’s geopolitical situation creates theoretical risk, in practice, TSMC is investing in diversification (Arizona fab, Japan fab) while maintaining its core manufacturing in Taiwan. The company’s advanced manufacturing capabilities, particularly for 3nm and future nodes, remain Taiwan-centric with no near-term alternatives at comparable scale.

5.3 Geopolitical Tensions and Taiwan Risk

The concentration of advanced semiconductor manufacturing in Taiwan, particularly TSMC’s dominance, creates both opportunities and threats for Intel. While Intel benefits from being a U.S.-based alternative, the broader geopolitical situation poses risks:

China-Taiwan Tensions: Escalating tensions between China and Taiwan create uncertainty about semiconductor supply chains. Scenarios range from economic coercion to military conflict, any of which could disrupt TSMC’s operations. While this theoretically benefits Intel as an alternative supplier, the reality is more complex:

Major customers would face severe disruptions affecting their Intel-based products too

Global semiconductor shortages would constrain all electronics manufacturing

Intel lacks capacity to absorb diverted TSMC customers quickly

Economic disruption would reduce overall demand

U.S.-China Technology Competition: Semiconductor technology has become central to U.S.-China strategic competition. Export controls restricting advanced chip sales to China have already impacted industry revenues. Potential escalation could lead to:

Further restrictions limiting Intel’s China revenue (approximately 25% of total)

Retaliation affecting supply chains and equipment suppliers

Technology decoupling requiring duplicate development efforts

Forced divestiture of Chinese operations or partnerships

Export Control Compliance: Intel must navigate increasingly complex export control regulations while maintaining global operations. The company’s manufacturing presence in China (including fabs and testing facilities) creates compliance challenges as restrictions tighten. Balancing market access with regulatory compliance requires ongoing legal and strategic attention.

5.4 Capital Requirements and Financial Constraints

Intel’s strategy requires sustained, massive capital investments that strain the company’s financial capacity:

Capital Expenditure Requirements: Intel’s IDM 2.0 strategy and foundry ambitions require capital investments that dwarf historical spending. The company has guided to:

Projected Capital Expenditures:

2024-2025: $25-28 billion annually

2026-2027: $20-25 billion annually (reduced but still high)

2028-2030: $15-20 billion annually (normalized levels)

Total 2024-2030: Approximately $150 billion

Comparison to Competitors:

- TSMC: ~$30-40 billion annually (larger scale, focused on manufacturing)

- Samsung: ~$20-25 billion annually (diversified across memory, foundry, devices)

- AMD: Minimal (fabless model requires minimal capex)

These investment levels strain Intel’s cash generation, particularly given current operating margins. The company has:

Suspended dividends to preserve cash

Reduced workforce significantly to cut costs

Relied on government subsidies to supplement capital

Explored selling minority stakes in the foundry business

Debt Burden: Intel’s debt has increased significantly to fund investments and operations during the turnaround period. While the company maintains investment-grade credit ratings, increasing debt levels limit financial flexibility and increase interest expenses.

Competitive Capital Efficiency: Intel faces competitors with more capital-efficient business models. AMD’s fabless model requires minimal capital investment, allowing the company to invest in R&D and sales rather than fabs. This structural advantage enables AMD to operate with higher return on invested capital (ROIC) even with lower revenues than Intel.

5.5 Technology Transition Risks and Execution Challenges

Intel’s ambitious technology roadmap (“five nodes in four years”) creates significant execution risk:

18A Yield and Ramp Risk: The most immediate risk centers on 18A technology. As Intel’s first use of both RibbonFET and PowerVia technologies, 18A represents a significant manufacturing challenge. Concerns include:

Initial yield reports suggesting industry-standard yields won’t be achieved until 2027

Complexity of managing both new transistor architecture and backside power delivery

Limited volume production reducing learning curve benefits

Foundry customer hesitation if yields lag expectations

Process Node Transition Complexity: Transitioning from Intel 3 to 18A, then subsequently to 14A and 10A requires flawless execution of multiple complex manufacturing steps. Each transition introduces risks of delays, yield issues, or performance shortfalls that could cascade through Intel’s product roadmap.

Foundry Customer Dependency: Unlike Intel’s internal products, foundry customers cannot tolerate significant delays or yield issues. A fabless chip company relies entirely on its foundry partner to deliver working silicon on schedule. Any significant 18A problems could not only delay Intel products but also terminate foundry customer relationships before they truly begin.

Technology Validation: Intel must demonstrate that 18A delivers on performance, power, and density promises. If 18A performance falls short of expectations or fails to compete effectively with TSMC N2, the entire foundry strategy loses credibility. Subsequent nodes (14A in 2026, 10A in 2027) must follow without delays to maintain momentum.

5.6 Market Cyclicality and Macroeconomic Sensitivity

The semiconductor industry is inherently cyclical, with demand closely tied to macroeconomic conditions:

PC Market Saturation: The PC market, representing roughly 50% of Intel’s revenue through the Client Computing Group, faces structural challenges:

Market saturation in developed economies

Lengthening replacement cycles as performance improvements plateau

Competition from tablets and smartphones for consumer computing

Economic sensitivity affecting consumer and corporate PC purchases

While AI PCs represent a potential catalyst for refresh cycles, the overall PC market is expected to remain relatively flat, limiting Intel’s largest revenue segment to low-single-digit growth.

Data Center Volatility: Data center infrastructure spending can be highly volatile, as demonstrated by cloud providers’ periodic optimization cycles. Major customers like Amazon, Microsoft, and Google periodically reduce server purchases to optimize utilization, creating revenue volatility for Intel.

Economic Recession Risk: A broader economic recession would impact Intel across all segments. Business IT spending, consumer electronics purchases, and automotive production all contract during recessions, directly affecting Intel’s revenues. With elevated debt levels and significant fixed costs from manufacturing capacity, Intel has less flexibility to weather extended downturns than in previous cycles.

Image source: intel.com

6. Strategic Initiatives and Execution Timeline

6.1 Process Technology Roadmap

Intel’s process technology roadmap represents the foundation of its turnaround strategy. The company has committed to regaining process leadership through an aggressive “five nodes in four years” roadmap:

Near-term Process Nodes (2025-2026):

Process Node

Status

Key Products

Timing

Competitive Comparison

Intel 3

In production

Meteor Lake, Granite Rapids

2024-2025

Similar to TSMC N5/N4

Intel 18A

Ramping

Panther Lake, Clearwater Forest

Late 2025-2026

Competitive with TSMC N3/N2

Intel 14A

Development

Nova Lake, data center products

2026-2027

Targets beyond TSMC N2

Intel 10A

Research

Next-generation products

2027-2028

Competitive with TSMC 1nm

Panther Lake and Clearwater Forest: These two products represent Intel’s first commercial implementations of 18A technology.

The successful launch and market acceptance of these products will largely determine whether Intel’s process technology strategy succeeds.

6.2 Product Launch Roadmap

Intel has a comprehensive product roadmap spanning multiple market segments:

Client Computing Products (2025-2027):

Client Roadmap Timeline:

2025:

- Arrow Lake Refresh (Intel 3): Enhanced desktop processors

- Panther Lake (18A): Next-generation mobile processors with AI focus

- Enhanced AI PC software ecosystem and developer tools

2026:

- Nova Lake (14A): Major architectural refresh for mobile and desktop

- Arrow Lake-S Refresh: Updated desktop mainstream products

- Expanded AI PC adoption across product stack

2027:

- Beast Lake (10A): Future architecture on cutting-edge process

- Continued AI PC evolution and feature expansion

Data Center and AI Products (2025-2027):

Data Center Roadmap:

2025-2026:

- Sierra Forest (Intel 3): E-core focused for cloud efficiency

- Granite Rapids (Intel 3): P-core focused for performance

- Clearwater Forest (18A): Next-generation E-core server

- Gaudi 3 expansion and Gaudi 4 development

2026-2027:

- Diamond Rapids (14A): Future Xeon platform

- Crescent Island GPU: AI inference-focused data center GPU

- Falcon Shores (delayed): Combined x86 and GPU platform

The data center roadmap aims to address different customer needs with specialized products rather than one-size-fits-all approaches.

6.3 Foundry Business Development Strategy

Intel Foundry Services must execute on multiple fronts simultaneously to build a viable foundry business:

Technology Enablement:

Process Design Kit (PDK) development for 18A and future nodes

IP library partnerships with ARM, Synopsys, Cadence, and others

EDA tool integration and validation

Design services and customer support infrastructure

Customer Acquisition:

Intel has announced several foundry customers, but needs to expand this base significantly:

Microsoft: Manufacturing Azure Maia AI chips on 18A

Amazon Web Services: Custom chip manufacturing partnership

Potential NVIDIA Partnership: Discussions around future products

Department of Defense: Secure manufacturing for defense applications

The company needs 10-15 significant customers to achieve $10-15 billion in foundry revenue by 2028-2030, which is necessary for profitability.

Capacity Planning:

Intel Foundry Capacity Expansion:

2025-2026:

- Fab 52, Arizona: 18A production ramp to 100K wafers/month

- Fab 34, Ireland: Intel 4/3 production at full capacity

- Fab 9, New Mexico: 18A initial production

2027-2028:

- Fab 62, Arizona: 18A/14A capacity expansion

- Ohio Fab 1 & 2: Future node production beginning

- European facilities: Depending on government funding and customer demand

Total planned investment exceeds $100 billion over the next five years, the largest private sector investment in U.S. manufacturing history.

6.4 AI Strategy Across the Portfolio

AI represents Intel’s most important growth opportunity, requiring coordinated strategy across products:

AI PC Leadership:

Core Ultra processors with integrated NPUs

Software ecosystem development (OpenVINO, oneAPI)

Developer tools and frameworks

Partnership with Microsoft, Adobe, and others for AI-enabled applications

Data Center AI:

Gaudi accelerator family (Gaudi 3 now, Gaudi 4 in development)

Xeon processors with built-in AI acceleration

Advanced networking for AI clusters

Integrated solutions with hardware and software optimization

Edge AI:

Purpose-built edge processors for industrial/automotive applications

Neural Compute Stick and edge accelerators

5G infrastructure with AI capabilities

Mobileye integration for automotive AI

Foundry for AI Chips:

Manufacturing custom AI accelerators for hyperscalers

Advanced packaging for heterogeneous AI systems

IP and design services for AI chip startups

Support for diverse AI architectures beyond x86

My Final Thoughts: Investor Recommendations and Outlook

Intel Corporation presents a high-risk, potentially high-reward investment opportunity centered on one of the most ambitious corporate transformations in technology industry history. The investment thesis rests on several key pillars:

Bull Case Pillars:

Reasons to Own Intel Stock:

1. 18A Technology Success

2. Government Support Unprecedented

3. Valuation Appears Attractive

4. Diversification Provides Resilience

5. Management Focused on Execution

Bear Case Concerns:

Reasons to Avoid or Sell Intel Stock:

1. Foundry Strategy Execution Risk

2. Competitive Pressures Intense

3. Financial Constraints Limiting

4. Technology Transition Risks

5. Market Dynamics Unfavorable