Is Micron the New Nvidia? Analyzing the $1 Trillion AI Memory Surge

Dear Readers, Welcome to Deep Research Global.

The pecking order of the AI hardware boom has just been rewritten.

On May 26, 2026, Micron Technology crossed a $1 trillion market cap, joining Samsung Electronics and SK Hynix in a club that, until last year, contained zero memory companies.

The stock surged 17.4% in a single session, after UBS lifted its price target to a Street high of $1,625 from $535.

For investors who spent two decades treating Micron as a cyclical commodity name, the question has become unavoidable: has the company outgrown its history, or are we watching another peak?

And more provocatively, can a memory chipmaker really become the next Nvidia?

This deep dive analysis examines the numbers behind the rally, the structural shifts inside the memory industry, the competitive dynamics with SK Hynix and Samsung, the risks every investor should weigh, and how Micron’s role compares with Nvidia’s at the center of the generative AI build-out.

Recommended - Read Full Reports

Read All Reports

Disclaimer: This analysis is for informational & educational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with their personal financial advisors before making investment decisions. Past performance does not guarantee future results.

The Numbers That Triggered the Rally

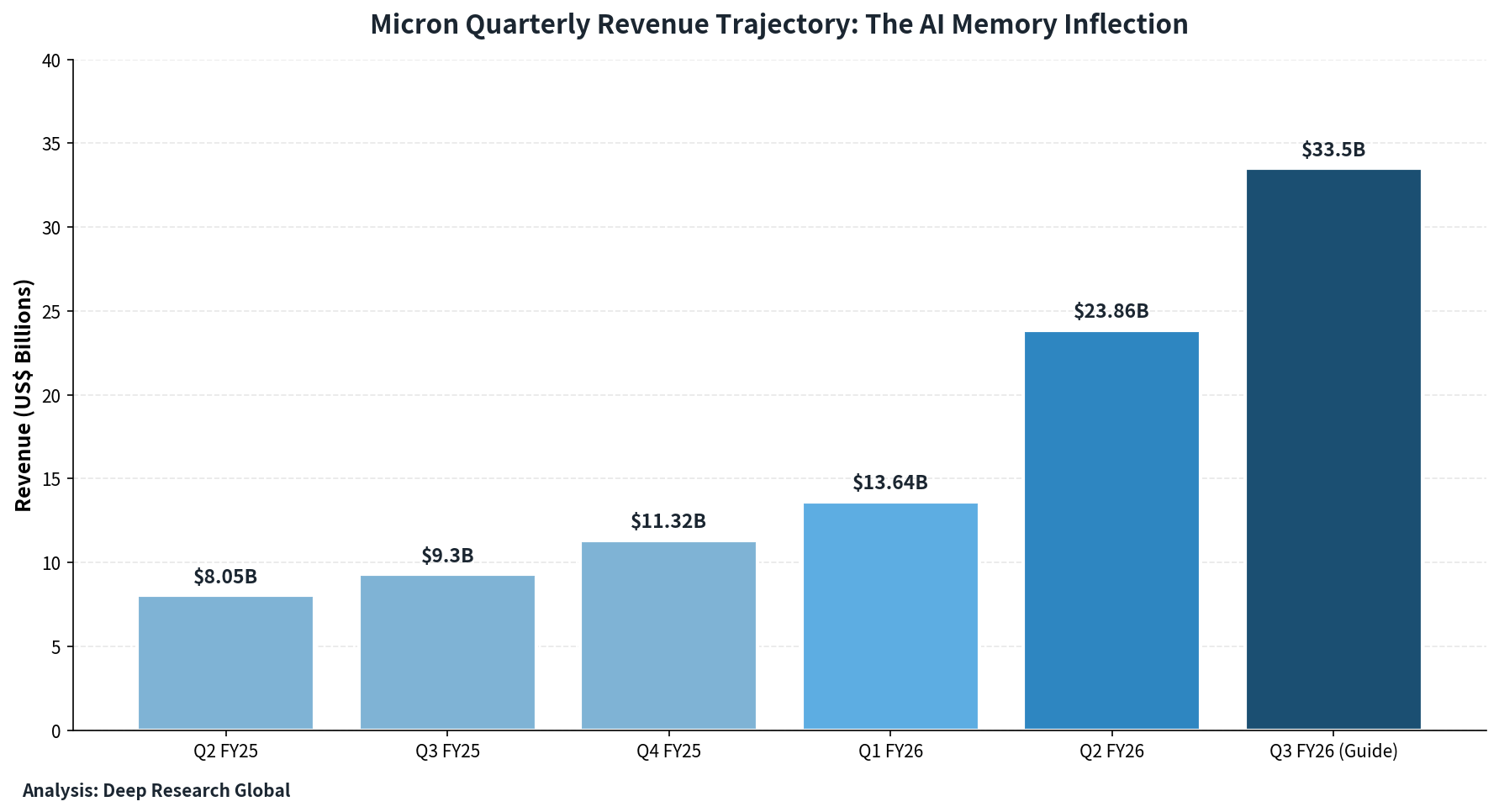

Micron’s fiscal Q2 2026 results, released in March 2026, were the catalyst that re-rated the entire sector.

Revenue reached $23.86 billion, up 196% year over year. Non-GAAP operating margin hit 69.0%, and non-GAAP diluted EPS came in at $12.20.

Two quarters earlier, the company had reported just $13.64 billion in Q1 FY2026, which itself was a 57% year-over-year jump. The sequential acceleration from Q1 to Q2 was the largest in the company’s modern history.

MICRON FISCAL Q2 2026 SNAPSHOT

- Revenue: $23.9 billion (+196% YoY)

- Non-GAAP operating income: $16.5 billion

- Non-GAAP operating margin: 69.0%

- Non-GAAP diluted EPS: $12.20

- Cloud Memory Business Unit: $7.7 billion

- Core Data Center: $5.7 billion

- Mobile & Client: $7.7 billion

- Automotive & Embedded: $2.7 billion

- Q3 FY2026 revenue guidance: $33.5B (plus or minus $0.75B)

- Q3 gross margin guidance: ~81%

- Q3 EPS guidance: $19.15 (plus or minus $0.4)

The Q3 guidance is the part Wall Street fixated on.

A jump from $23.9 billion to $33.5 billion in a single quarter, with gross margins expanding from roughly 75% to 81%, implies pricing power that traditional memory cycles never produced.

Image source: Deep Research Global analysis. Quarterly revenue chart showing Micron’s acceleration from $8.05B in Q2 FY2025 to a guided $33.5B in Q3 FY2026, reflecting the AI memory inflection.

The cloud business unit alone now generates more revenue per quarter than Micron’s entire company produced just two years ago.

That segment carries 74% gross margin, a number unthinkable in the prior decade when memory routinely swung between losses and modest profits.

The HBM Sell-Out: How Demand Outran Supply

CEO Sanjay Mehrotra confirmed in fiscal Q1 results that Micron’s entire 2026 HBM production is sold out, with prices locked in through long-term agreements.

He went further in May 2026, warning Bloomberg that the memory shortage extends beyond 2026 and that customers are receiving partial allocations rather than full orders.

This is not a typical cyclical setup. Customers are signing multi-quarter and multi-year volume agreements at fixed prices, which gives Micron visibility memory companies have historically lacked.

HBM SOLD-OUT TIMELINE PER CEO COMMENTARY

- Calendar 2026: Volume and pricing locked

- HBM4 36GB 12-Hi: High-volume production began Q1 2026

- HBM4 16-Hi (48GB per cube): Sampling stage

- HBM4E: In development, volume ramp in calendar 2027

- Shortage outlook: Persists beyond 2026 per CEO

Micron began volume shipments of HBM4 36GB 12-high stacks in the first calendar quarter of 2026, designed specifically for Nvidia’s Vera Rubin platform. The product delivers more than 2.8 TB/s of bandwidth with a 20% improvement in power efficiency over the prior generation.

A 16-high version, lifting per-cube capacity to 48GB, is already sampling with customers. HBM4E follows in 2027, built on Micron’s 1-gamma DRAM node.

Inside the Vera Rubin Platform: Why Memory Became the Bottleneck

Nvidia kicked off the Vera Rubin generation at GTC 2026, unveiling six new chips that together form what Jensen Huang called an extreme-codesign supercomputer.

The Rubin GPU itself packs 288GB of HBM4 per package, with later Rubin Ultra variants pushing memory capacity even higher.

The arithmetic is stark. Each Rubin GPU requires roughly four to six times the HBM capacity of a 2023-era H100, and the system-level bandwidth requirements scale with model parameters that are now routinely above one trillion.

This is why Mehrotra and his counterparts at SK Hynix keep talking about a structural shift rather than a cycle.

Every incremental GPU sold by Nvidia, AMD, or a custom-silicon hyperscaler pulls dramatically more memory than the prior generation.

RUBIN VS BLACKWELL MEMORY DELTA

- Rubin GPU: 288GB HBM4 per package

- Blackwell B200: 192GB HBM3E per package

- Rubin Ultra (planned): higher stack count, more capacity

- Per-rack bandwidth: scales into the petabyte-per-second range

- Customer mix: GPU + custom ASIC adopters

Nvidia’s own Q1 FY2027 results, released in May 2026, showed data center revenue of $75.2 billion, up 92% year over year.

Each dollar of Nvidia data center revenue now corresponds to significantly more memory dollars than the prior generation, which is why memory suppliers are riding the same wave with steeper margin slopes.

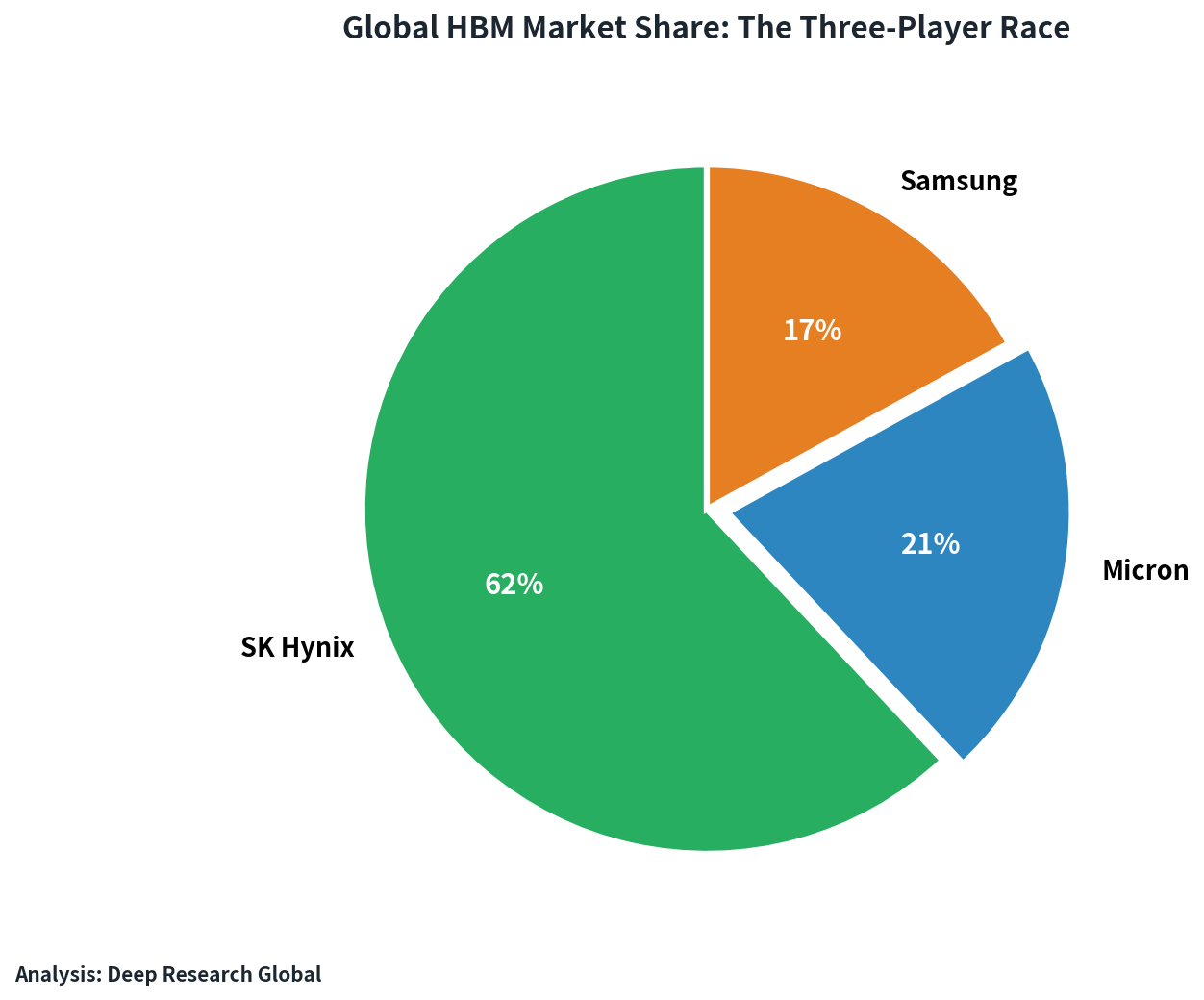

The Three-Player HBM Race: Where Micron Fits

The HBM market is effectively a triopoly. Industry data puts SK Hynix at roughly 62%, Micron at 21%, and Samsung at 17% as of recent quarters.

That 21% share is striking because Micron was a distant third with mid-single-digit share less than two years ago. The company moved up by combining yield execution on HBM3E with an earlier-than-rivals push into HBM4.

Image source: Deep Research Global analysis. Visualization of the three-player HBM market based on industry tracker data, showing SK Hynix’s dominant 62% share, Micron’s rise to 21%, and Samsung at 17%.

SK Hynix remains the dominant supplier and the primary HBM partner for Nvidia’s initial Rubin builds.

Reports suggest Nvidia’s first-year Rubin volumes lean heavily on SK Hynix and Samsung for HBM4, with Micron taking a smaller initial allocation that expands later.

HBM SHARE & POSITIONING SUMMARY

- SK Hynix (~62%): Lead Nvidia supplier, HBM4 leader, 57T won Q1 OP

- Micron (~21%): Third entrant, HBM4 in volume Q1 2026, U.S. base

- Samsung (~17%): Catching up after HBM3 setbacks, 50% capacity surge planned

- Combined annual HBM revenue: tracking toward record levels

- ASIC HBM demand growth in 2026: +82% YoY (Goldman Sachs)

The competitive picture is also shifting beyond Nvidia.

Goldman Sachs forecasts that ASIC HBM demand will grow 82% in 2026, making custom silicon roughly 33% of the total HBM market.

Micron has confirmed it now ships HBM in volume to four customers spanning both GPU and ASIC platforms.

Hyperscaler Capex: The Demand Floor Under Memory

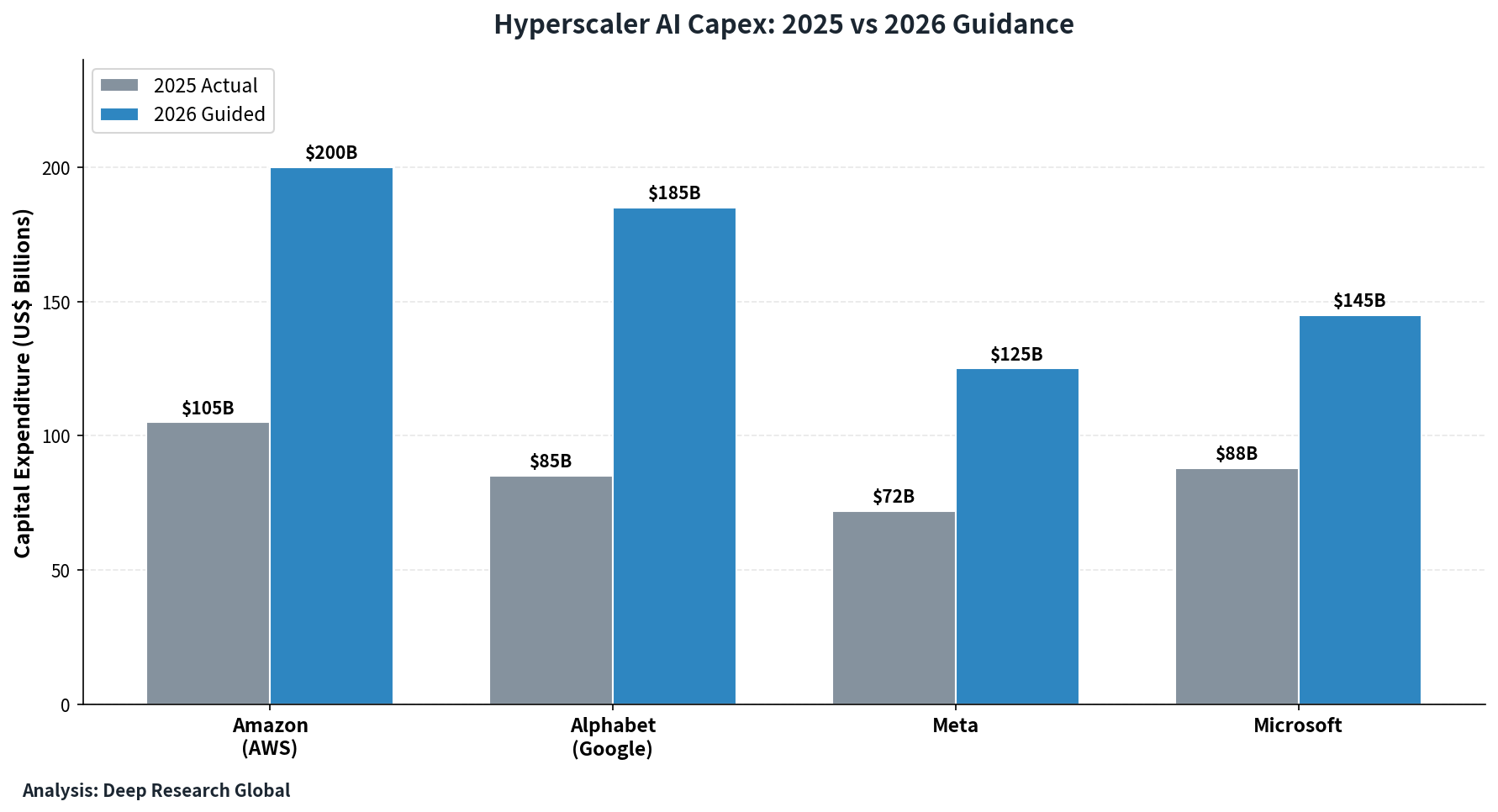

The single most important external variable for Micron is the capital spending plan of the largest cloud builders.

Aggregate 2026 capex guidance from Amazon, Alphabet, Meta, and Microsoft has reached roughly $725 billion combined, up sharply from the 2025 record.

That spending pool is what funds the AI server build-out that, in turn, pulls HBM, DDR5, and high-density storage. Estimates show roughly $690 billion in 2025-2026 committed AI infrastructure spending across the top U.S. hyperscalers.

Image source: Deep Research Global analysis. Comparison of hyperscaler capex guidance for 2025 actual versus 2026 guided midpoints across Amazon, Alphabet, Meta, and Microsoft, illustrating the spending wave underpinning AI memory demand.

The math behind the memory tightness is straightforward.

AI server bills of materials allocate a growing share to memory subsystems, with HBM commonly representing 30% to 50% of a Rubin-class accelerator’s bill of materials.

HYPERSCALER 2026 CAPEX (GUIDED MIDPOINTS)

- Amazon (AWS): ~$200B

- Alphabet (Google): ~$185B

- Microsoft: ~$140-150B range

- Meta: ~$115-135B range

- Combined Big Four: ~$725B (Tom's Hardware aggregation)

- Implied AI infrastructure share: large majority of total

For Micron, the read-across is that data center DRAM and NAND bit total addressable market are expected to exceed 50% of industry TAM for the first time in calendar 2026.

That mix shift alone explains a large portion of the margin uplift, because data center memory carries significantly richer economics than consumer DRAM.

The DRAM and NAND Supercycle Beyond HBM

HBM gets the headlines, but conventional DRAM is the bigger contributor to Micron’s revenue base.

Contract DRAM prices rose roughly 80% to 90% quarter over quarter entering Q1 2026 across most segments, with further increases of 30% locked in for Q2 2026 contracts.

Samsung finalized a ~30% DRAM price hike for Q2 2026 contract customers, a move Micron and SK Hynix have largely matched.

2026 MEMORY PRICING DYNAMICS

- DRAM contract prices Q4 2025 to Q1 2026: +80-90% QoQ

- Q2 2026 contract hikes: ~30% (industry-wide)

- H2 2026 outlook: +5-20% QoQ moderation expected

- IDC 2026 supply growth: DRAM +16%, NAND +17% (below historical norm)

- DRAM TAM share from data centers in 2026: >50% for first time

NAND flash is showing similar dynamics, with IDC projecting 2026 supply growth of just 17%, well below the historical mid-twenties percentage. Demand for high-density enterprise SSDs has spiked as hyperscalers rebuild storage tiers around vector databases and inference caches.

The result is the broadest memory pricing surge since the 2017-2018 cycle, and arguably the most durable one.

Where the 2017 cycle ended when smartphone demand normalized, the current setup is anchored to multi-year hyperscaler capex commitments.

Capacity Expansion: The $200 Billion U.S. Build-Out

To meet this demand, Micron has committed to roughly $200 billion in U.S. investments across Idaho, New York, and Virginia. Fiscal 2026 capex alone exceeds $25 billion, up from $20 billion in the prior plan and roughly $8 billion two years ago.

The capacity additions are sequenced. Idaho first production is targeted between late 2026 and 2027, with New York fabs ramping between 2028 and 2029.

MICRON FAB EXPANSION TIMELINE

- Idaho (Boise): Production ramp late 2026 to 2027

- New York (Clay): Up to four fabs, 2028-2029 onwards

- Taiwan (Tongluo): Cleanroom expansion ongoing

- Japan, Singapore, India: Additional capacity investments

- Total U.S. commitment: ~$200 billion over the decade

- FY2026 capex: >$25 billion (raised from $20B)

The capital intensity is precisely what bears point to as a long-term risk. Memory has historically been a capital-burning industry where additions arrive late in cycles, depressing prices.

The counter-argument from management is that customer contracting structures have evolved. Long-horizon volume and pricing agreements, particularly for HBM, give suppliers visibility that supports more disciplined investment.

Margins, Cash Flow, and the New Economic Profile

The financial profile that has emerged at Micron looks very different from the company that lost money in 2023. Q2 FY2026 free cash flow was $6.9 billion, generated against $5.0 billion of capital expenditure in the same quarter.

That swing from negative to massively positive free cash flow is what UBS pointed to when arguing the multiple should re-rate.

The bank’s $1,625 target implies a market cap of roughly $1.8 trillion, which would slot Micron between Broadcom and Tesla in U.S. company rankings.

MICRON CASH FLOW PROFILE Q2 FY2026

- Operating cash flow: well above $11B

- Capital expenditure: $5.0 billion

- Adjusted free cash flow: $6.9 billion

- Annualized FCF run-rate: trending toward $30B+

- Net debt position: rapidly improving

- Q3 FY2026 EPS guide: $19.15 (plus or minus $0.4)

Forward valuation tells the same story.

Micron trades at roughly 8.42 times forward earnings, against 22.15 for the S&P 500 and 26.23 for the Nasdaq 100.

The market is still pricing Micron as a cyclical that will crash, while management and the bull case argue it has structurally shifted toward a contracted, visibility-rich earnings profile.

Which view is correct will be one of the dominant equity-market debates of the next few quarters.

How Micron’s Story Differs From Nvidia’s

The comparison investors keep making is direct: Micron rallied roughly 243% to 307% over the trailing year, while Nvidia gained 35% to 43% over the same period.

So is Micron the new Nvidia?

The honest answer is more nuanced.

Nvidia commands a platform position with proprietary CUDA software, system-level integration, and pricing power that resembles Apple or Microsoft far more than a memory supplier.

Micron, by contrast, sells a commoditized product that, even with HBM customization, is fundamentally a building block in someone else’s system.

The customization for HBM4 logic dies narrows that gap, because chipmakers can now tweak base dies to specific customer requirements, but it does not eliminate the dependence.

MICRON VS NVIDIA - STRUCTURAL COMPARISON

- Pricing power: Nvidia >> Micron (platform vs component)

- Customer concentration: Both heavy in hyperscalers

- Gross margin profile: Nvidia ~75% software-like; Micron ~75% peak cycle

- Capital intensity: Nvidia fabless; Micron heavy fab spend

- Trailing 12M stock return: Micron significantly outperformed

- Forward P/E: Micron ~8x; Nvidia ~30x+

- Moat durability: Nvidia software lock-in; Micron tech node race

The clearer parallel is that Micron is to the AI compute build-out what Intel was to the PC era, or what Western Digital and Seagate were to early cloud.

It’s a critical, high-margin component supplier whose fortunes track but do not replicate the platform owner’s.

For investors, the better question may not be whether Micron is the new Nvidia, but whether the AI cycle is durable enough to make the third-largest HBM supplier worth more than General Electric.

That is the bet the market is actively making.

Risks That Could Break the Narrative

The bull case rests on assumptions that need to hold for the rally to extend.

The first and most important is sustained hyperscaler capex.

If even one of Amazon, Alphabet, Meta, or Microsoft trims its 2027 capex by 20%, the marginal memory demand picture shifts immediately. Memory has historically been the leverage point of any AI capex correction because customers cancel chips faster than data center shells.

KEY DOWNSIDE RISKS TO THE THESIS

1. Hyperscaler capex pause or cut in 2027

2. SK Hynix and Samsung HBM4 yield acceleration crushes pricing

3. Nvidia takes more HBM share from Samsung at Micron's expense

4. Custom ASICs shift HBM to in-house qualification, slowing Micron ramp

5. Geopolitical disruption to Taiwan packaging supply chain

6. Industry capacity additions arriving in 2027-2028 normalize prices

7. Macro recession compresses enterprise IT spending broadly

The second risk is supply response.

The same $25 billion-plus annual capex programs Micron is running are mirrored at SK Hynix and Samsung, with Samsung planning a 50% HBM capacity surge in 2026.

If those additions come online with strong yields in late 2027, the current pricing environment could moderate. The historical lesson from memory is that supply always eventually catches demand, the only question is timing.

A third risk is customer concentration.

Nvidia, Broadcom, AMD, and a handful of hyperscaler ASIC programs likely account for the majority of HBM demand, and any single program slipping changes the order book quickly.

The fourth, less discussed risk is technology transition.

HBM4E in 2027 brings customizable base dies, and the supplier that wins the most logic-die qualifications will likely take share.

SK Hynix’s relationships with Nvidia and AMD give it a head start that Micron is working hard to close.

What the Q3 FY2026 Print Will Tell Investors

Micron’s next earnings release lands in late June 2026 and will be the single most important data point of the summer. The guided revenue range of $32.75 billion to $34.25 billion and 81% gross margin sets a high bar.

WATCH ITEMS FOR Q3 FY2026 PRINT

- Actual gross margin vs 81% guide

- Cloud Memory BU revenue trajectory

- HBM revenue disclosure as % of total DRAM

- Q4 FY2026 guidance shape

- Any commentary on 2027 HBM contracting status

- Updated capex envelope for FY2027

- Color on customer mix between GPU and ASIC

A beat-and-raise will likely send the stock through prior highs and trigger another round of price-target revisions. A miss, particularly on margins, would test whether investors are willing to underwrite the structural-shift narrative or revert to cyclical-discount math.

The single most useful signal will be whether Micron extends its sold-out commentary into calendar 2027.

If management can credibly say next year’s volumes and pricing are also locked, the cyclical discount in the multiple becomes much harder to defend.

Positioning in the Broader AI Memory Trade

For investors building exposure to the AI memory build-out, Micron is the largest and only meaningfully liquid U.S.-listed pure-play.

SK Hynix and Samsung trade in Seoul with material won-exposure friction, and Samsung’s broader business mixes memory with consumer electronics and foundry.

Adjacent beneficiaries include the equipment makers, particularly Applied Materials, Lam Research, and KLA, all of which supply tools for the advanced packaging that HBM requires.

Hybrid bonding and through-silicon-via deposition are now bottleneck steps where memory makers compete for tool slots.

AI MEMORY VALUE CHAIN MAP

- Pure-play memory: Micron (U.S.), SK Hynix (KR), Samsung (KR)

- Memory equipment: Applied Materials, Lam Research, KLA, ASML

- HBM controller IP: Synopsys, Cadence, Rambus

- Advanced packaging: TSMC (CoWoS), Amkor, ASE

- AI compute customers: Nvidia, AMD, Broadcom, Marvell

- Hyperscaler buyers: AWS, Google, Microsoft, Meta, Oracle

The full value chain perspective matters because the same dollar of hyperscaler capex flows through multiple beneficiaries.

Investors who own only one name in the stack may be over-exposed to product-specific risks while missing the broader build-out.

Whether Cyclicality Truly Ends This Time

The most consequential debate around Micron is not earnings or HBM share, it is whether memory has been permanently de-cyclicalized.

Every prior cycle in the industry’s history ended with overcapacity and pricing crashes.

What’s different this time, the bulls argue, is the combination of three structural shifts.

First, hyperscaler capex now operates on multi-year planning horizons that smooth out the demand whipsaw.

WHAT THE BULLS SAY IS DIFFERENT THIS CYCLE

1. Multi-year volume + price contracts replace spot markets

2. Memory has become >50% of data center silicon TAM

3. AI workload growth is non-discretionary for cloud competitiveness

4. Three-supplier discipline limits capacity arms race

5. Capital intensity has risen faster than expected, slowing additions

6. Customer mix has broadened beyond GPUs to ASICs

Second, the technology gap between HBM4 and HBM4E creates qualification cycles that lock customer relationships for years rather than quarters.

Third, the capital cost of new fabs has risen to the point that no Chinese new entrant can credibly close the gap before 2028.

The bear counter is simpler: every cycle felt different at the top. The 2000 dot-com peak, the 2007 mobile peak, the 2017 cloud peak all came with structural-shift arguments that did not survive the next twelve months.

The truth is likely somewhere between.

Memory will probably still be cyclical, but the cycle floor and amplitude could be permanently higher because the AI demand layer sits underneath the consumer cycle that historically drove the busts.

The Investor Takeaway

What the May 2026 milestone really represents is the moment the market started pricing Micron as an AI infrastructure stock rather than a memory commodity.

Whether that re-rating fully holds depends on three things the company does not entirely control: hyperscaler capex durability, competitor execution, and the macro environment.

What Micron does control, it is executing well.

HBM4 is in volume, HBM4E is on schedule, U.S. capacity is being added with bipartisan policy support, and customer contracting is moving toward multi-year structures.

FINAL FRAMING - WHAT TO WATCH

- Hyperscaler 2027 capex guidance (next 2-3 quarters)

- Q3 FY2026 earnings: late June 2026

- HBM4E sampling milestones and customer wins

- Any commentary on 2027 sold-out status

- Margin trajectory beyond Q3 81% guide

- New York fab construction progress

The comparison with Nvidia will likely remain imperfect.

Nvidia owns the platform, Micron supplies a critical component, and those two roles command different valuations across history.

What is now clear is that the AI build-out has lifted memory from a commodity afterthought to a strategically scarce input, and the equity market has woken up to the implications.

Whether the next leg up comes from the bears capitulating or from a genuinely new earnings power emerging, the trade has moved well beyond a pure cyclical bounce.

For long-horizon investors, the question to wrestle with is not whether Micron is the new Nvidia, but whether the current memory profit pool is structurally larger than at any prior peak.

The evidence so far points yes, with the caveat that the industry’s track record of eventually breaking its own pricing discipline remains intact.