Nike (NKE) - Fundamental Analysis Report 2026 (Updated)

Dear Readers, Welcome to Deep Research Global.

Let’s analyze the topic in detail.

Executive TL;DR

Nike’s fiscal 2026 third quarter delivered $11.3 billion in revenue, flat year-over-year on a reported basis, while diluted EPS of $0.35 contracted 35 percent as tariffs and inventory cleanup compressed gross margin by 130 basis points to 40.2 percent.

CEO Elliott Hill, now eighteen months into his “Win Now” reset, says the company is in the “middle innings” of its turnaround, with North America wholesale and the running category showing the earliest signs of recovery while Greater China is being deliberately reset.

Tariff exposure remains the single biggest near-term overhang, with management quantifying a roughly $1.5 billion gross impact on fiscal 2026 cost of goods and a 3.15 percentage point drag on Q4 gross margin.

Despite revenue softness, Nike returned $609 million to shareholders in dividends in Q3 alone and has now extended its consecutive annual dividend increase streak to 24 years.

Recommended - Read Full Reports

Read All Reports

Table of Contents

Executive TL;DR

Introduction

Nike Company Profile: Key Facts

Nike Investment Thesis

Proposition 1

Proposition 2

Proposition 3

Nike Business Model Overview

The Brand Creation Engine

The Product Development Engine

The Distribution Engine

Nike Revenue Analysis

Q1 FY26

Q2 FY26

Q3 FY26

Reading the Cadence

Latest Quarterly Earnings, Guidance, and Earnings Quality

Q3 FY26 Earnings Quality Review

Q4 FY26 Guidance

Management Commentary

Margins, Earnings Power, and EPS Trajectory

Gross Margin Mechanics

Operating Expense Discipline

EPS Trajectory

Cash Flow Mechanics and Balance Sheet Health

Balance Sheet Snapshot

Capital Returns Engine

Segment-by-Segment Teardown

North America: The Engine of Recovery

Europe, Middle East & Africa (EMEA)

Greater China: The Hardest Problem

Asia Pacific & Latin America (APLA)

Converse: The Persistent Problem Child

NIKE Direct vs Wholesale: The Channel Rebalance

Product Categories: The Sport Offense in Action

Strategic & Competitive Context

The Hill Doctrine: Win Now and Sport Offense

The Competitive Landscape: A Two-Front War

The China Question

Tariff Impact in Detail

Valuation Framework

Earnings-Based Frameworks

Cash Flow and Dividend Frameworks

Multiples Versus History

Bull, Base, and Bear Case Scenario Analysis

Bull Case

Base Case

Bear Case

Key Risks

Tariff and Trade Policy Risk

China Geopolitical and Competitive Risk

Inventory and Promotional Risk

Competitive Innovation Risk

Leadership and Execution Risk

Macro and Consumer Risk

Catalysts to Watch

Near-Term Catalysts (Next 6 Months)

Medium-Term Catalysts (6 to 18 Months)

Long-Term Catalysts (18+ Months)

Latest Analyst Price Targets

My Final Thoughts

Official Sources & Data

Disclaimer: This analysis is for informational & educational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with their personal financial advisors before making investment decisions. Past performance does not guarantee future results.

Introduction

Nike’s fiscal 2026 has been a story of two diverging tape measures.

The top line has stopped collapsing and clawed back to roughly flat, yet the bottom line keeps shrinking, with Q3 net income falling to $0.5 billion against a 40.2 percent gross margin that has compressed for six straight quarters.

That divergence sits at the heart of every investor question about the company today.

Has Elliott Hill’s reset actually changed Nike’s trajectory, or is the swoosh simply running in place while tariffs, China weakness, and a $7.5 billion inventory position bleed margin?

This in-depth analysis report break down the numbers, segment by segment, to answer all.

Nike Company Profile: Key Facts

Company: NIKE, Inc.

Ticker: NKE (NYSE)

Headquarters: Beaverton, Oregon (Philip H. Knight Campus)

Founded: 1964 (as Blue Ribbon Sports); renamed Nike in 1971

President & CEO: Elliott Hill (returned October 2024)

EVP & CFO: Matthew Friend

Fiscal Year End: May 31

FY2025 Revenue: $46.3 billion (reported)

FY2025 Net Income: $3.2 billion

FY2025 Diluted EPS: $2.16

Q3 FY26 Revenue: $11.3 billion

Recent Close: $42.57 (May 18, 2026)

Brands: NIKE, Jordan, Converse

Employees: ~77,800 (full-time, May 31, 2025)

Manufacturing: Vietnam 51%, Indonesia 28%, China 17% (footwear)

Dividend: $0.41 quarterly (24 consecutive years of raises)Nike’s structural footprint is anchored in three brand pillars: the NIKE Brand itself (which houses Jordan), and the standalone Converse business. Within NIKE Brand, the company sells through two channels: NIKE Direct (its owned digital and stores) and Wholesale (department stores, sporting goods chains, specialty retailers).

The geographic structure splits the world into four operating segments: North America, Europe, Middle East & Africa (EMEA), Greater China, and Asia Pacific & Latin America (APLA).

For fiscal 2025, non-U.S. NIKE Brand and Converse sales accounted for approximately 57% of total revenues, underscoring how internationally exposed the franchise still is.

Production is concentrated in three Asian countries.

In fiscal 2025, factories in Vietnam, Indonesia, and China manufactured approximately 51%, 28% and 17% of total NIKE Brand footwear, respectively. That concentration is now the single most important driver of the company’s exposure to the United States tariff regime introduced in 2025.

Nike Investment Thesis

The investment thesis on Nike in 2026 is no longer about whether the brand is broken.

The franchise is among the most recognized commercial trademarks on Earth, runs at margins most apparel peers envy even today, and produces enough cash to keep raising its dividend through the worst stretch of operational disruption in 20 years.

The thesis is now about timing and earnings power.

Investors who buy Nike at current levels are effectively underwriting three propositions at once.

Proposition 1: The Hill Reset Will Restore Premium Brand Equity

The first proposition is that Elliott Hill’s “Win Now” strategy, layered with a new “Sport Offense” operating model, will rebuild premium positioning and product narrative after the brand drift of 2022 to 2024.

Hill’s public scoreboard for himself has been deliberately blunt. On the Q2 FY26 call he stated, “Fiscal year ‘26 continues to be a year of taking action to rightsize our classics business, return Nike digital to a premium experience, diversify our product portfolio, deepen our consumer connection, strengthen our partner relationships and realign our teams and leadership.”

He added that the company is in the “middle inning” of its comeback, and bluntly conceded, “we’re nowhere near our potential.” That is honest framing for a $46 billion company.

Proposition 2: Tariff Costs Are Temporary, Not Structural

The second proposition is that the gross margin damage being done by United States reciprocal tariffs in fiscal 2026 represents a transient cost shock, not a permanent reset.

The company has guided that reciprocal tariff rates will add approximately $1.5 billion in gross costs over the next several quarters, with a 3.15 percentage point hit to Q4 gross margin specifically attributed to tariffs.

If this turns out to be a 12 to 18 month digestion problem, Nike can offset it through targeted pricing, sourcing shifts, and operating leverage as volume recovers. If tariffs prove structural and competitors do not face equivalent pressure, Nike’s North American profitability resets lower for years.

Proposition 3: China Recovers, Eventually

The third proposition is the most contentious. Greater China is Nike’s third largest market but the most challenged, with Q3 FY26 sales falling 10 percent and management guiding to a 20 percent decline next quarter as it deliberately reduces selling-in to clear old product.

Hill says China remains “one of the company’s most powerful long-term opportunities” but acknowledged improvement is “not happening at the level or the pace we need.” That is corporate code for “we have lost share to Anta and Li Ning and we know it.”

Nike Business Model Overview

Revenue Architecture (FY2025, $46.3B total):

- NIKE Brand $44.7B (96.5%)

- NIKE Direct $18.8B (channel)

- Wholesale $25.9B (channel)

- Converse $1.7B (3.6%)

- Global Brand Divisions small residual

Nike’s economic engine is built around three interlocking flywheels: brand creation, product development, and global distribution.

Each reinforces the others, which is why the brand has historically commanded a premium gross margin in the mid 40s relative to most apparel peers.

The Brand Creation Engine

Brand creation is anchored in sport partnerships. Nike’s roster spans the NBA (uniform partner since 2017), the NFL (extended through 2038 via a 10-year deal), the WNBA, individual athletes ranging from LeBron James and A’ja Wilson to Kylian Mbappé and Sha’Carri Richardson, and federations across soccer, basketball, and athletics.

The recent partnership extension with the NFL and the signing of a 2026 NFL Rookie Class of 20 elite athletes are not marketing window dressing. They are how Nike maintains premium pricing power and category authority. Sports marketing expense was elevated again in Q3 FY26, reflecting the cost side of this strategy.

The Product Development Engine

Product development under Hill is being explicitly reorganized around sport categories rather than the gender-and-style matrix that defined Nike’s structure under predecessor John Donahoe. Hill’s new “Sport Offense” model restructures the operating model around core sports including running, basketball, training, and football.

In the Q3 FY26 call, Hill noted that “Spring 2027 will be the first time we see the fruits of those teams working together.” That is a concrete planning anchor for investors trying to time the recovery.

The Distribution Engine

Distribution is being deliberately rebalanced. Under the prior regime, Nike pushed aggressively into NIKE Direct (digital plus owned stores) and pulled back from wholesale relationships. Hill has reversed that mix. In Q3 FY26, wholesale revenues rose 5 percent on a reported basis to $6.5 billion, while NIKE Direct revenues fell 4 percent to $4.5 billion.

That deliberate reweighting toward wholesale is one of the most important strategic changes inside the company. It restores partnership health with Foot Locker, JD Sports, Dick’s Sporting Goods, and similar accounts that drive incremental traffic and inventory turn that Nike cannot match through its own channels alone.

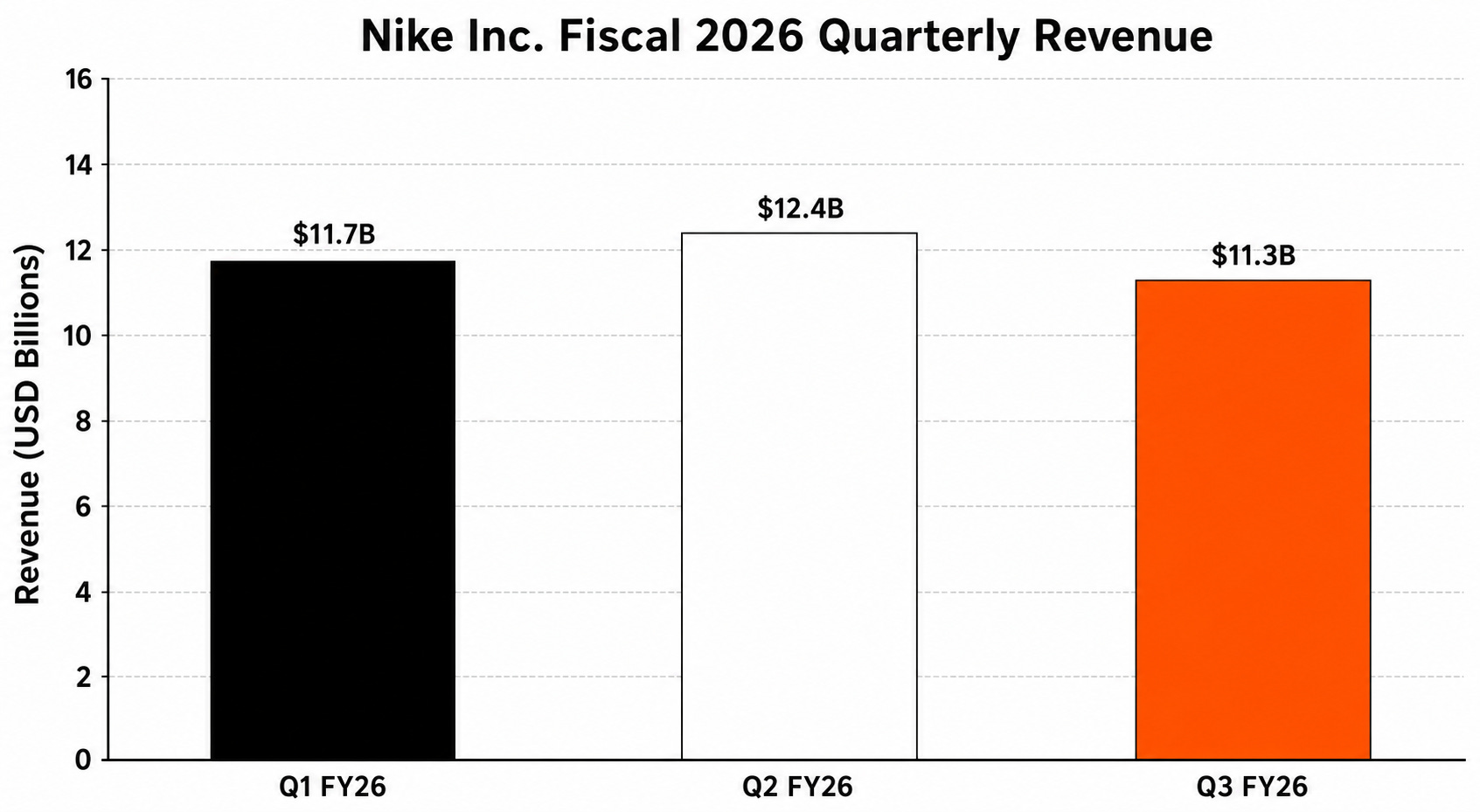

Nike Revenue Analysis

Image source: Deep Research Global analysis, based on Nike Inc. fiscal 2026 quarterly press releases

Looking at the FY26 cadence quarter by quarter tells the story better than annualized aggregates.

Q1 FY26 (August 31, 2025)

First quarter revenues were $11.7 billion, up 1 percent reported and roughly flat on a currency-neutral basis. Gross margin decreased 320 basis points to 42.2 percent, and diluted EPS was $0.49.

Q1 FY26 Geographic Mix (in $M):

- North America 5,020

- EMEA 3,331

- Greater China 1,512

- APLA 1,490

This was the quarter when management first confirmed measurable progress on its “Win Now” priorities of North America, Wholesale, and Running.

Q2 FY26 (November 30, 2025)

Second quarter revenues were $12.4 billion, up 1 percent reported and flat on a currency-neutral basis. Gross margin fell 300 basis points to 40.6 percent. Net income was $0.8 billion, with diluted EPS at $0.53, which actually beat consensus by 15 cents.

Q2 FY26 Geographic Mix (in $M):

- North America 5,633 (+9% YoY)

- EMEA 3,392

- Greater China 1,423 (-17% YoY)

- APLA 1,667

- Global Brand Divisions 9

The North America strength and China collapse defined the quarter. North America wholesale alone climbed 8 percent to $7.5 billion at the company level, and the company recorded its strongest Black Friday ever on Nike.com, partially powered by the Air Jordan “Black Cat” launch.

The stock still fell more than 10 percent the next morning because investors fixated on the 17 percent China decline and the persistent tariff impact.

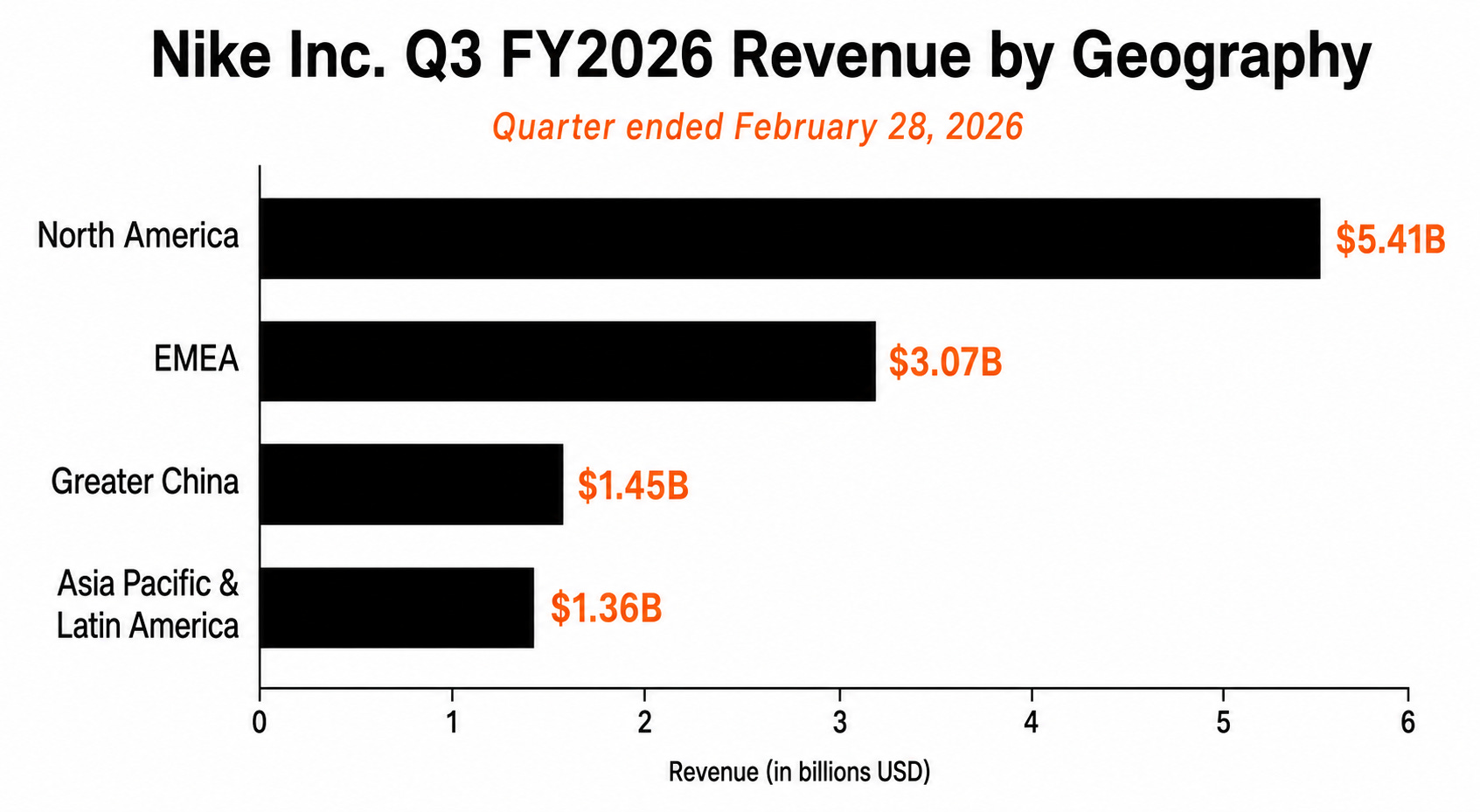

Q3 FY26 (February 28, 2026)

Third quarter revenues were $11.3 billion, flat reported and down 3 percent on a currency-neutral basis. NIKE Brand revenues were $11.0 billion, with wholesale up 5 percent at $6.5 billion and NIKE Direct down 4 percent at $4.5 billion.

NIKE Brand Digital fell 9 percent and NIKE-owned stores were down 5 percent, both reflecting the deliberate retreat from heavy promotional activity that had defined the prior regime.

Image source: Deep Research Global analysis, based on Nike Inc. fiscal 2026 third quarter press release

Reading the Cadence

Reported Revenue ($B), trailing five quarters:

Q3 FY25: 11.27 (down 9% YoY)

Q4 FY25: 11.10

Q1 FY26: 11.72 (+1% YoY)

Q2 FY26: 12.43 (+1% YoY)

Q3 FY26: 11.28 (flat YoY)

The flattening at the top line is the first piece of empirical evidence that the

Keep reading with a 7-day free trial

Subscribe to Deep Research Global to keep reading this post and get 7 days of free access to the full post archives.