onsemi (ON Semiconductor) - SWOT Analysis Report (2026)

onsemi SWOT analysis 2026: Silicon carbide leadership, AI data center growth, automotive recovery prospects, and competitive challenges examined for investors.

onsemi $ON ( ▲ 0.72% ) , the Arizona-based power semiconductor specialist, posted $1.55 billion in revenue for Q3 2025, beating analyst expectations despite a 12% year-over-year decline.

Our comprehensive SWOT analysis examines onsemi’s internal capabilities and external market dynamics as it pursues leadership in automotive electrification, AI infrastructure, and industrial automation against intensifying competition and cyclical pressures.

Table of Contents

Strengths: Core Capabilities Driving Competitive Advantage

Vertically Integrated Silicon Carbide Leadership

onsemi has established one of the semiconductor industry’s most comprehensive silicon carbide (SiC) production chains. The company controls every stage from raw material sourcing to finished power modules, a rarity that provides both cost advantages and supply security.

Manufacturing Footprint

Facility Location

Capacity

Production Stage

Status

Bucheon, South Korea

1M+ wafers/year (200mm)

SiC wafer fabrication

Operational since 2023

Hudson, New Hampshire

400K+ wafers/year

SiC crystal growth & substrate

Expanded 2025

Rožnov pod Radhoštěm, Czech Republic

End-to-end SiC production

Integrated manufacturing

Construction phase

The Czech Republic facility, backed by €450 million in European Commission funding, represents a $2 billion investment over multiple years. When operational, this integrated site will produce everything from SiC substrates through power modules for European automotive customers.

This vertical integration delivered tangible results in 2025. onsemi’s China SiC revenue doubled in Q2 2025, driven by new electric vehicle production ramps with manufacturers including Xiaomi’s YU7 electric SUV and expanded partnerships with NIO and other Chinese EV makers.

Image source: onsemi.com

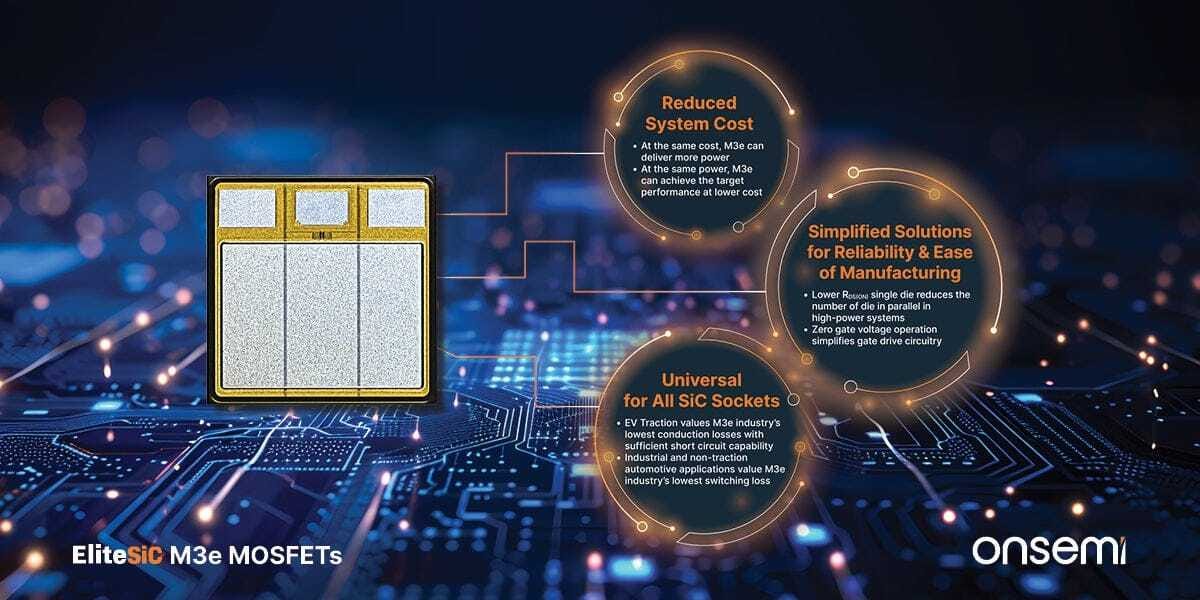

EliteSiC Technology Platform

The company’s EliteSiC technology platform offers demonstrable performance advantages over competing solutions. Partnerships with Schaeffler for plug-in hybrid electric vehicle (PHEV) traction inverters leverage EliteSiC’s lower conduction losses and superior short-circuit robustness.

Key EliteSiC advantages:

30% lower switching losses versus previous generation

Higher current density per chip area

Enhanced thermal performance for compact designs

Proven reliability across temperature extremes

Strategic AI Data Center Positioning

While automotive silicon carbide commanded attention through 2024, onsemi’s AI data center initiatives emerged as a critical growth driver in 2025. The company’s collaboration with NVIDIA to enable 800 Volts Direct Current (VDC) power architectures positions it at the center of next-generation AI infrastructure.

AI Revenue Trajectory

Period

AI Data Center Revenue

Growth Rate

Percentage of Total Revenue

Q1 2025

~$60M

-

4.1%

Q2 2025

~$100M

67% sequential

6.8%

Q3 2025

~$125M

25% sequential

8.1%

FY2025 Target

$250M+

-

~5.5%

This explosive growth trajectory reflects genuine demand for power-efficient solutions as AI workloads strain existing data center infrastructure. NVIDIA’s shift toward 800V architectures to support one-megawatt IT racks creates immediate opportunities for onsemi’s high-voltage power semiconductors.

The October 2025 acquisition of Vcore Power Technology from Aura Semiconductor accelerated this positioning. Vcore’s advanced voltage regulation technology addresses the “last inch” of power delivery, bringing energy directly to AI processors with minimal losses.

This complements onsemi’s existing AC-DC and DC-DC conversion solutions, creating a complete power tree from grid to silicon.

Image source: onsemi.com

Treo Platform Innovation

The Treo Platform, introduced late 2024, represents a fundamental architectural advance in analog and mixed-signal design. Built on 65nm BCD (bipolar, CMOS, DMOS) process technology, Treo integrates analog, digital, and power functions on a single chip with unprecedented flexibility.

Treo Platform Capabilities

Voltage Range: 1V to 90V (industry-widest)

Process Node: 65nm

Integration: Analog + Digital + Power in single die

Architecture: Modular, SoC-like with IP building blocks

Key Applications: Industrial sensors, automotive ADAS, smart power management

The platform’s modular architecture accelerates customer time-to-market while reducing development costs. October 2025’s announcement that Teledyne selected Treo for advanced infrared imaging systems validates the platform’s capabilities in demanding industrial applications.

Robust Financial Foundation

Despite revenue declines through 2025, onsemi maintained financial discipline that provides strategic flexibility.

Q3 2025 Financial Highlights

Metric

Value

Comparison

Revenue

$1,550.9M

Beat analyst estimates by 2.2%

Non-GAAP Gross Margin

38.0%

Stable despite volume decline

Non-GAAP Operating Margin

19.2%

Industry-leading profitability

Free Cash Flow

$372.4M

24% of revenue

Cash & Investments

$2.87B

Strong liquidity position

The company’s November 2025 authorization of a $6 billion share repurchase program, doubling the previous $3 billion authorization, signals management confidence in the business trajectory.

Through 2025, onsemi allocated approximately 100% of free cash flow to share buybacks, reflecting a disciplined capital allocation approach while major capacity investments ramp.

Weaknesses: Challenges Requiring Strategic Attention

Automotive Revenue Concentration and Cyclical Exposure

Automotive end-markets generated 58% of onsemi’s revenue in Q3 2025, creating significant concentration risk as the automotive industry navigates a complex transition period.

Automotive Segment Performance

Quarter

Automotive Revenue

Sequential Change

Year-over-Year Change

Q1 2025

$556.7M

-26%

-31%

Q2 2025

$555.9M

Flat

-27%

Q3 2025

$583.3M

+5%

-11%

Q4 2025 (midpoint guidance)

~$585M

+0.3%

-14%

While sequential stabilization emerged through 2025, the year-over-year comparisons reveal the depth of the automotive semiconductor correction. Traditional internal combustion engine vehicle production remained weak, while electric vehicle adoption growth slowed from the torrid 2021-2023 pace.

Geographic concentration compounds this exposure. China represented approximately 30% of total revenue in 2025, with automotive being the dominant end-market.

Revenue in China declined 7% sequentially in Q3 2025 due to macroeconomic softness and strategic shifts by Chinese automakers managing inventory levels.

Industrial Segment Underperformance

The Industrial Solutions Group (ISG), onsemi’s smallest segment at 15% of revenue, posted the weakest performance in 2025.

ISG Q3 2025: $230.0M revenue (-18% YoY, +7% sequential)

Full-Year 2025 Estimate: ~$870M (-22% YoY)

This weakness reflects broad-based industrial inventory corrections and cautious capital spending across factory automation, industrial power, and white goods markets. While AI data center growth provided a bright spot within ISG, traditional industrial applications remained challenged.

The industrial segment’s struggles matter beyond its current revenue contribution. Industrial applications historically provided stable, counter-cyclical revenue during automotive downturns.

The simultaneous weakness across both automotive and industrial end-markets in 2025 exposed onsemi to a broader cyclical downturn than its portfolio diversification might suggest.

Margin Pressure from Underutilization

onsemi’s Q3 2025 non-GAAP gross margin of 38.0% remained healthy by industry standards but reflected ongoing pressure from factory underutilization.

Margin Evolution

Period

Non-GAAP Gross Margin

Key Factors

Q3 2024

45.5%

Peak utilization, strong pricing

Q1 2025

40.0%

Utilization decline begins

Q2 2025

37.6%

Inventory corrections accelerate

Q3 2025

38.0%

Stabilization with volume recovery

The company reduced manufacturing utilization through 2025 to avoid inventory build-up during the demand slowdown. While prudent from a balance sheet perspective, lower factory loading carries substantial margin impact given semiconductor manufacturing’s high fixed costs.

Management’s Q4 2025 guidance of 37.0% to 39.0% non-GAAP gross margin suggests continued utilization challenges into early 2026. Return to the company’s stated long-term 40%+ target requires meaningful demand recovery and volume growth.

Restructuring Costs and Asset Impairments

The company’s reported GAAP results for 2025 reveal substantial one-time charges that, while non-recurring, indicate strategic repositioning challenges.

2025 Restructuring Activity (Nine Months)

Total Restructuring Charges: $608.1M

Asset Impairments: $487.9M (primarily Q1 2025)

Non-Cash Inventory Charges: $281.5M

These charges primarily related to the exit from the Japan-based Mountain Top fab and optimization of the manufacturing footprint. While these moves position the company for improved long-term profitability, they represent significant value destruction from previous investment decisions.

Opportunities: Growth Vectors for 2026 and Beyond

Electric Vehicle Acceleration in China and Globally

Despite 2025’s slowdown, the structural shift toward vehicle electrification remains intact and accelerating. onsemi’s design win pipeline positions it to capture this growth.

EV Market Projections

Region

2024 EV Sales

2025E EV Sales

2026E EV Sales

onsemi Content per Vehicle

China

~9.5M units

~12M units

~15M units

$150-300 (SiC-equipped)

Europe

~3.2M units

~3.8M units

~5M units

$200-400 (higher SiC attach)

North America

~1.5M units

~1.8M units

~2.4M units

$250-450 (premium segment)

At the 2025 Shanghai Auto Show, onsemi revealed its products would feature in 50% of new EV models (including PHEVs) displayed. These design wins typically convert to revenue 12-18 months post-announcement, setting up a strong 2026-2027 ramp.

The China market presents particularly compelling near-term opportunity. After doubling China SiC revenue in Q2 2025, onsemi’s partnerships with leading Chinese OEMs position it to ride the next wave of EV volume growth. Chinese manufacturers are increasingly adopting 800V architectures for fast-charging capability, playing directly to onsemi’s EliteSiC strengths.

AI Infrastructure Build-Out

The AI data center opportunity extends far beyond onsemi’s current $250 million annual run rate. Multiple growth vectors exist within this expanding market.

AI Power Infrastructure Segments

Rack-Level Power Delivery (800V architectures)

- Estimated market: $2-3B by 2027

- onsemi position: Strategic partnership with NVIDIA

- Content opportunity: $500-1,500 per rack

Server Power Supplies (80 Plus Titanium efficiency)

- Estimated market: $5-7B by 2027

- onsemi position: Full SiC and GaN portfolio

- Content opportunity: $100-300 per server

GPU Power Delivery (Vcore acquisition)

- Estimated market: $3-5B by 2027

- onsemi position: Recent Vcore technology addition

- Content opportunity: $50-150 per GPU

The December 2025 partnership with GlobalFoundries to develop 650V gallium nitride (GaN) power devices specifically targets AI data center, automotive, and aerospace applications. GaN offers higher switching frequencies than silicon carbide, enabling smaller, lighter power conversion systems ideal for dense AI infrastructure.

Image source: investor.onsemi.com

Industrial Automation and Physical AI

The convergence of artificial intelligence with industrial robotics, autonomous mobile robots (AMRs), and smart manufacturing systems creates a multi-billion-dollar sensing and power opportunity.

Industrial Automation Technology Requirements

Application

Key Technologies

onsemi Solutions

Market Size 2027E

Collaborative Robots

Vision sensors, ToF depth sensing

Hyperlux ID sensor family

$4-6B

AMRs & AGVs

LiDAR, imaging arrays, motor control

Image sensors, power drivers

$3-5B

Machine Vision

High-speed imaging, AI processing

Treo-based image processors

$5-7B

Predictive Maintenance

Industrial IoT sensors, edge AI

Low-power sensor fusion SoCs

$2-4B

The March 2025 introduction of the Hyperlux ID family, the industry’s first real-time indirect time-of-flight (iToF) sensor, addresses a critical need in industrial robotics for accurate depth perception. These sensors enable robots to operate safely alongside humans, a key requirement for collaborative automation.

onsemi holds over 40% market share in automotive image sensors. Translating this imaging expertise to industrial applications through platforms like Treo represents a significant cross-selling opportunity as smart factories proliferate.

Geographic Manufacturing Expansion and Incentives

Government initiatives to reshore semiconductor manufacturing create funding opportunities for capacity expansion.

Regional Incentive Programs

Region

Program

Available Funding

onsemi Relevance

United States

CHIPS Act

$39B (manufacturing), $11B (R&D)

Potential grants for SiC expansion

European Union

European Chips Act

€43B total support

€450M secured for Czech facility

South Korea

K-Semiconductor Strategy

₩1T+ in tax benefits

Existing Bucheon facility benefits

While onsemi has not yet announced specific CHIPS Act funding awards, the company’s domestic manufacturing presence in New Hampshire and New York positions it as a logical recipient. The Department of Commerce prioritization of strategic materials including silicon carbide aligns with onsemi’s core competencies.

The secured €450 million EU support for the Czech facility demonstrates onsemi’s ability to navigate government programs successfully. This funding reduces the effective capital intensity of the $2 billion investment while securing long-term European market access.

Threats: External Risks to Monitor

Silicon Carbide Oversupply Risk

The SiC power semiconductor market faces a growing mismatch between supply capacity and near-term demand as multiple competitors expand aggressively.

SiC Capacity Additions (2024-2026)

STMicroelectronics: Catania expansion (40% capacity increase)

Infineon Technologies: Kulim facility (significant capacity add)

Wolfspeed: Mohawk Valley fab (13x capacity increase)

Rohm Semiconductor: Expansion in Japan

Chinese Competitors: 15+ new entrants ramping capacity

Industry analysis project SiC wafer market growth slowing to 20% in 2025, down from 40%+ growth in 2022-2023. This deceleration occurs as new capacity comes online, potentially creating oversupply conditions in 2026-2027 if EV demand recovery disappoints.

Chinese competition presents particular concern. Domestic Chinese SiC manufacturers benefit from government support and lower cost structures. While currently focused on the Chinese market, these players could pressure global pricing as they mature technologically.

onsemi’s doubled China SiC revenue in 2025 came partly from market share gains, but sustainable competitiveness requires continuous technology leadership.

SiC Market Competitive Dynamics

Competitor

Estimated 2025 Market Share

Key Strengths

Pricing Strategy

STMicroelectronics

35-40%

Automotive relationships, scale

Volume-based discounting

onsemi

15-20%

Vertical integration, EliteSiC technology

Premium for performance

Infineon

15-20%

Broad portfolio, module expertise

Bundling across products

Wolfspeed

10-15%

Material quality, long track record

Premium positioning

Chinese suppliers

10-15%

Local market access, cost advantage

Aggressive pricing

Intensifying Competition from Integrated Device Manufacturers

Major automotive OEMs and technology companies are pursuing vertical integration strategies that could disintermediate semiconductor suppliers.

Vertical Integration Moves

Tesla: In-house power electronics design, rumored SiC development

BYD: Acquired semiconductor design capabilities

Xiaomi: Developing custom automotive silicon

Apple: Expanding silicon design beyond mobile to automotive

While these initiatives primarily target digital silicon initially, the trend toward OEM-designed power semiconductors could pressure onsemi’s automotive design win pipeline. The company’s response involves deepening technical partnerships and offering system-level solutions that pure-play IDMs struggle to replicate.

The data center market shows similar dynamics. Hyperscalers, including Amazon (Annapurna Labs), Google (Tensor), and Microsoft (custom AI silicon) design increasing amounts of custom silicon.

While this creates opportunity for differentiated analog and power solutions, it also risks commoditization of standard power delivery components.

www.deepresearchglobal.com/p/amazon-swot-analysis

www.deepresearchglobal.com/p/alphabet-swot-analysis

Microsoft SWOT Analysis (2025)

www.deepresearchglobal.com/p/microsoft-swot-analysis

Macroeconomic and Geopolitical Headwinds

The semiconductor industry operates at the intersection of multiple geopolitical fault lines that create business uncertainty.

Geopolitical Risk Factors

Risk

Impact on onsemi

Mitigation Strategies

US-China Technology Restrictions

Export controls limiting China sales (~30% of revenue)

Diversify customer base; compliant products

Taiwan Semiconductor Risk

Supply chain disruption (packaging operations)

Dual-source critical capabilities

European Energy Costs

Manufacturing cost pressure (Czech facility)

Energy-efficient process technology

Currency Fluctuations

Translation impacts on global revenues

Natural hedges; selective hedging programs

The Biden administration’s export control expansions on advanced semiconductors to China continue evolving. While power semiconductors currently face fewer restrictions than leading-edge logic chips, future controls could limit onsemi’s access to China’s massive automotive market.

Broader macroeconomic conditions add uncertainty. The semiconductor industry projects 11-12% revenue growth in 2025, but this outlook assumes stable interest rates and avoiding recession. Economic weakness in Europe or China could defer automotive electrification investments, delaying onsemi’s recovery trajectory.

Talent Acquisition and Retention Challenges

The semiconductor industry faces a critical talent shortage that intensifies as capacity expands.

Industry Talent Gap Projections

Estimated U.S. Semiconductor Jobs by 2030: 1.4M

Current Workforce: ~345K

Required New Hires: ~1M

Engineering Graduates (relevant fields) per year: ~67K

Projected Annual Deficit: ~60K workers

onsemi’s geographic manufacturing strategy spanning Arizona, New Hampshire, New York, South Korea, and the Czech Republic creates competition for scarce engineering and technical talent. The Czech facility expansion particularly faces challenges given Central Europe’s limited semiconductor workforce.

The company’s R&D spending of $450 million annually (approximately 10% of revenue) positions it as an attractive employer, but competition from both traditional semiconductor companies and technology giants bidding for the same talent pool remains fierce.

Strategic Imperatives for 2026

Execution of Manufacturing Ramps

The Czech Republic SiC facility represents onsemi’s largest growth investment. Successful execution requires navigating construction, equipment installation, process qualification, and customer certification. Delays could allow competitors to capture market share during the expected 2026-2027 EV demand recovery.

The company projects the Czech facility will reach meaningful production by late 2026, with full ramp extending into 2028. This timeline creates a narrow window to capture European automaker design wins before alternative suppliers lock in positions.

AI Infrastructure Portfolio Integration

The Vcore acquisition closed in October 2025, creating integration challenges and opportunities. Successfully combining Vcore’s voltage regulation expertise with onsemi’s existing power portfolio could establish unmatched “grid-to-core” capability, but execution risks include technology integration, customer qualification, and sales force coordination.

The NVIDIA 800V partnership provides validation and a reference design for the broader market. Converting this collaboration into production revenues across multiple hyperscaler and enterprise data center customers represents a 2026 priority.

Margin Recovery Path

Returning gross margins to 40%+ requires a combination of volume recovery, favorable product mix, and operational efficiency gains. Management’s guidance suggests Q4 2025 will see continued pressure before improvement begins.

Margin Recovery Levers

Initiative

Potential Margin Impact

Timeline

Automotive volume recovery

+150-200 bps

H2 2026

AI data center mix improvement

+100-150 bps

Throughout 2026

Manufacturing footprint optimization

+50-100 bps

2026-2027

Treo platform ramp (higher-margin products)

+50-100 bps

2026-2027

SiC vertical integration benefits

+100-150 bps

2027+

Achieving the upper end of these ranges would return onsemi to industry-leading profitability, but requires successful execution across multiple dimensions simultaneously.

Capital Allocation Balance

The $6 billion share repurchase authorization signals confidence but creates tension with growth investment needs. onsemi must balance:

Returning capital to shareholders through buybacks

Funding multi-billion-dollar manufacturing expansions

Maintaining strategic acquisition flexibility

Preserving investment-grade balance sheet strength

The company’s strong free cash flow generation ($933 million through nine months of 2025) provides flexibility, but sustained capital intensity through the Czech ramp will test this balance. Management has indicated prioritizing strategic investments while opportunistically repurchasing shares, suggesting a dynamic capital allocation approach.

My Final Thoughts

onsemi stands at an inflection point where multi-year investments in silicon carbide and strategic positioning in AI infrastructure position it for significant growth, but near-term execution challenges and competitive threats create meaningful risk.

The company’s vertically integrated SiC strategy represents a genuine competitive advantage.

Few competitors can match this level of supply chain control, particularly for the automotive market, where long-term supply assurance matters as much as technology performance. The Czech facility investment, backed by substantial European government support, reinforces this advantage for a critical geographic market.

AI data center revenue growth from negligible to $250 million annually in less than two years demonstrates both opportunity scale and onsemi’s ability to pivot quickly. The NVIDIA partnership and Vcore acquisition position the company to capture meaningful share of the multi-billion-dollar AI power infrastructure build-out through 2027.

However, investors should recognize several considerations.

The automotive concentration creates continued cyclical exposure until industrial and data center end-markets scale to meaningful diversification. The 2026-2027 timeframe will test whether EV adoption resumes strong growth or continues the 2025 deceleration pattern.

Silicon carbide market dynamics bear watching closely. Oversupply conditions in 2026 could pressure pricing and margins across the industry. onsemi’s technology leadership and vertical integration provide some insulation, but not immunity. The company’s ability to maintain premium pricing through superior performance will determine whether margins expand or contract as volumes recover.

From a portfolio perspective, onsemi represents a levered bet on three technology trends: vehicle electrification, AI infrastructure expansion, and industrial automation. These secular growth drivers remain intact despite near-term cyclical noise. The company’s financial strength and strategic positioning provide resources to navigate the transition period.

The $6 billion buyback authorization at current valuation levels suggests management views the stock as undervalued relative to long-term earnings power. This capital allocation decision merits attention, as management teams often possess superior insight into business trajectory versus outside analysts.

Investors evaluating onsemi for 2026 should focus on three key metrics:

Automotive revenue stabilization signaling demand recovery

AI data center revenue progression toward $500 million annually, and

Gross margin trajectory back toward 40%.

These indicators will validate or challenge the company’s strategic positioning ahead of major new capacity coming online in 2027.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with financial advisors before making investment decisions.