SpaceX-Tesla Merger: Possibilities and Impact

Dear Readers, Welcome to Deep Research Global.

Let’s analyze the topic in detail.

The single most discussed corporate event of 2026 is no longer just the SpaceX IPO.

Investor attention has shifted to a much bigger question: whether Elon Musk intends to follow the Nasdaq debut by combining SpaceX with Tesla into one gigantic public company.

Several recent reports have confirmed that Musk has spoken with colleagues about folding the two companies into a single entity.

Prediction markets have also begun pricing in the probability, and Wall Street analysts have placed the odds anywhere between 33 percent and 90 percent depending on the timeframe.

For investors, this is no more a hypothetical scenario. SpaceX is set to start trading under ticker SPCX on the Nasdaq in mid-June 2026, and the structural conditions for a follow-on combination are already aligning.

This deep dive analysis walks through what is currently known, the financial mechanics, the operating overlap, the governance concerns, the strategic logic, the risks, and what it could mean for shareholders of both companies.

QUICK SUMMARY

- SpaceX IPO: Targeted June 12, 2026 (Ticker: SPCX)

- SpaceX target valuation: up to $1.75 trillion

- Tesla current market cap: ~$1.6 trillion (May 2026)

- Combined entity potential: ~$3.4 trillion

- Wedbush merger probability: 80-90% by early 2027

- Kalshi prediction market: 52% by May 2027

Recommended - Read Full Reports

Read All Reports

Disclaimer: This analysis is for informational & educational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with their personal financial advisors before making investment decisions. Past performance does not guarantee future results.

How the Merger Conversation Reached This Point

The current merger talk is the natural extension of a long sequence of intercompany dealings between Tesla, SpaceX, and xAI that began intensifying in 2024 and accelerated dramatically in early 2026.

In January 2026, Tesla disclosed a $2 billion investment in xAI, Musk’s artificial intelligence venture.

Within weeks, SpaceX absorbed xAI in a transaction valued at roughly $1.25 trillion, which is easily the largest U.S. corporate tie-up ever by value.

That single transaction restructured Musk’s empire into two giants:

A private SpaceX (now also home to xAI and the X social media platform), and

A public Tesla.

The combination of these two is what is now under active discussion.

TIMELINE OF MUSK ENTITY CONSOLIDATION

2016 - Tesla acquires SolarCity ($2.6B)

2022 - Musk takes Twitter private ($44B)

2025 - xAI acquires X for $33B equity ($45B incl. debt)

2026 (Jan) - Tesla invests $2B in xAI

2026 (Feb) - SpaceX merges with xAI (~$1.25T combined)

2026 (May) - SpaceX files S-1 for $1.75T IPO

2026 (Jun) - SPCX expected to begin trading

2026-2027? - Potential SpaceX–Tesla merger

Parallel entrepreneurship is a strategy Musk has already proven works. Bringing the parallel tracks under one roof appears to be the logical next chapter.

The Numbers Behind a $3.4 Trillion Combination

Both companies sit roughly in the same neighborhood, which makes a stock-for-stock combination plausible without either side having to pay a crippling premium.

Tesla closed recent sessions at a market capitalization near $1.65 trillion (as of May, 2026), and SpaceX is pricing its IPO at up to $1.75 trillion.

If SpaceX is the acquirer, the rocket and satellite group would need to issue new shares equivalent to roughly 94 percent of its post-IPO float to absorb Tesla at parity.

That assumes no takeover premium, which is rare in practice. SpaceX’s share count, based on its S-1 filing, would nearly double from roughly 4.1 billion to about 8 billion shares.

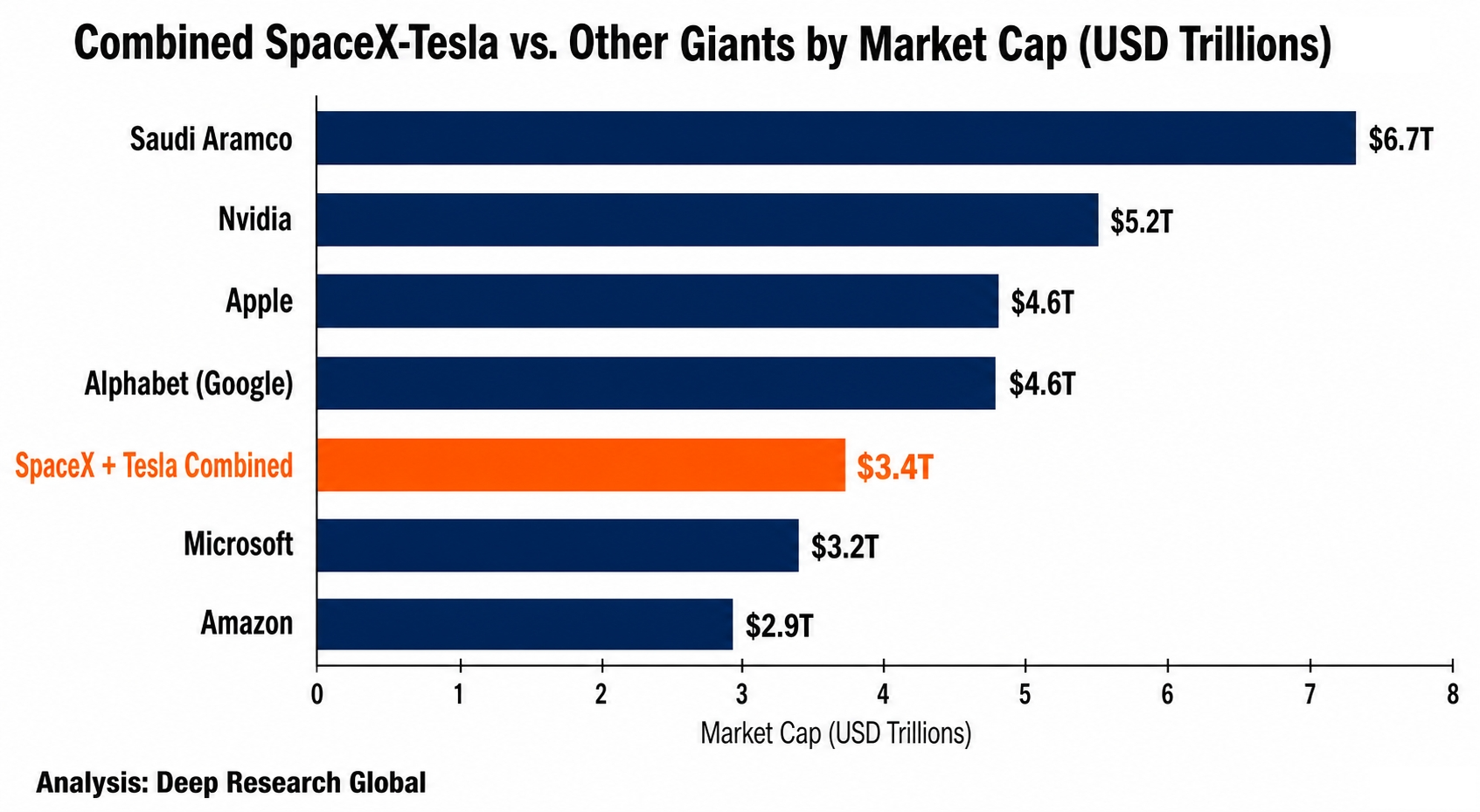

Image source: Deep Research Global analysis. Comparing the potential combined SpaceX-Tesla valuation of approximately $3.4 trillion against the world’s largest publicly traded companies, based on market cap data.

PRO-FORMA COMBINATION MATH

SpaceX (IPO target) $1.75T

Tesla (current market cap) $1.65T

-----------------------------------

Pro-forma combined entity ~$3.40T

Rank globally 5th most valuable public co.

For reference:

Saudi Aramco $6.7T

Nvidia $5.2T

Apple $4.6T

Alphabet (Google) $4.6T

Microsoft $3.2T

Amazon $2.9T

A $3.4 trillion combination would slot just behind Microsoft and Apple and just ahead of Amazon.

In sheer dollar terms it would be the largest corporate merger ever attempted, eclipsing the historical record holders by a wide margin.

The pro-forma ownership structure is what makes this deal politically dramatic.

SpaceX investors would go from owning 100 percent of an aerospace and AI conglomerate to roughly 52 percent of a combined business, with Tesla’s existing shareholders holding the remaining 48 percent.

That changes the gravitational center of the new company.

Tesla’s manufacturing assets, automotive cash flow, and consumer brand would suddenly back the same equity as Falcon 9 reusability, Starship, Starlink, xAI compute, and the X social network.

The Financial Reality Underneath the Story

However, the headline valuation hides a more uncomfortable truth.

The merged company would, based on the most recent disclosed figures, be unprofitable on a consolidated GAAP basis.

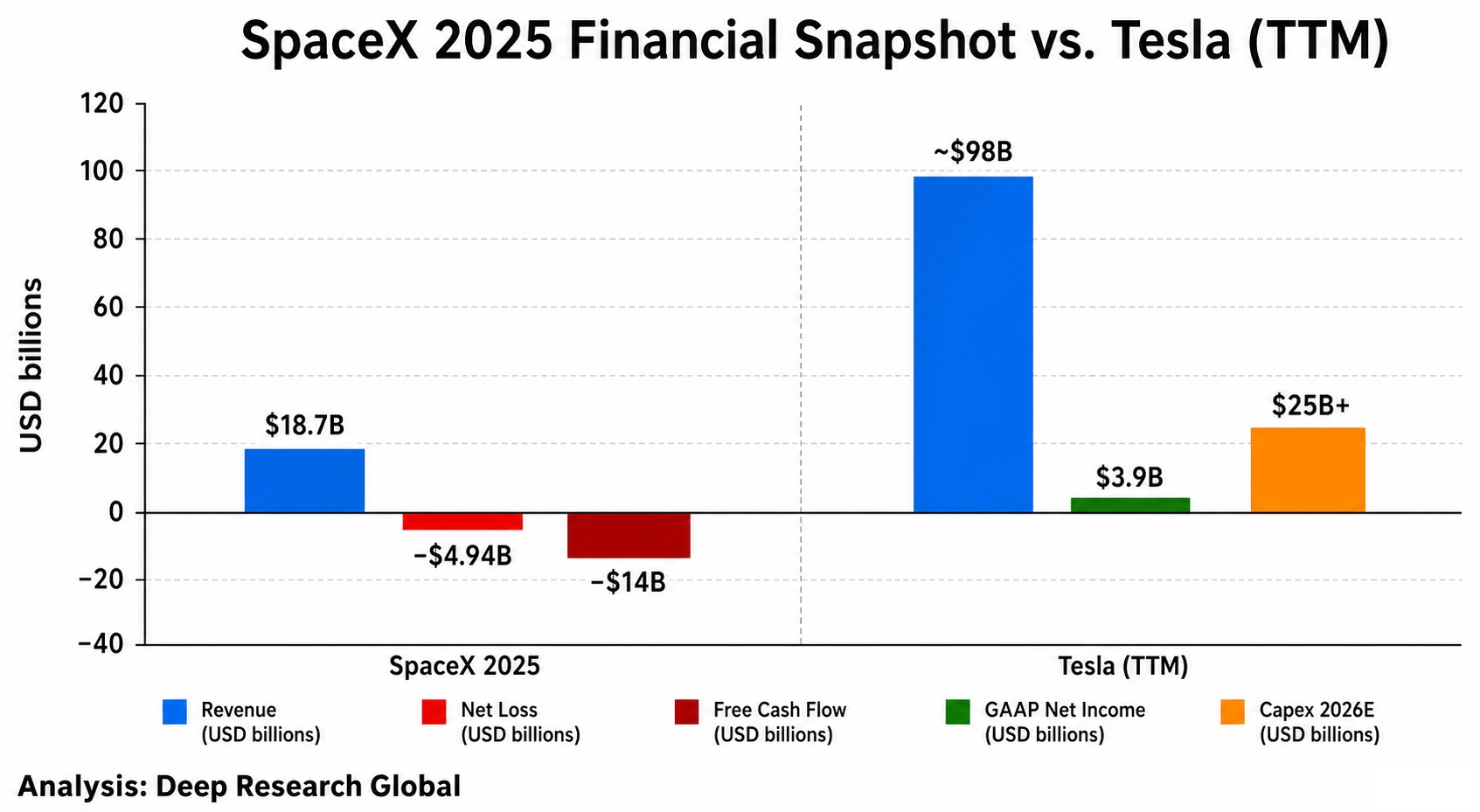

In its IPO filing, SpaceX disclosed $18.7 billion in 2025 revenue alongside a net loss of $4.94 billion. The company also reported a free cash flow deficit of $14 billion, driven primarily by AI infrastructure capex.

Tesla, for its part, posted roughly $3.9 billion in GAAP net income in the trailing four quarters. That’s down sharply from $15 billion in 2023 and $7.0 billion in 2024. About $1.6 billion of the figure came from regulatory credit sales, a stream Musk himself has said will fade.

Image source: Deep Research Global analysis. Comparing SpaceX 2025 financial data from its S-1 filing with Tesla’s most recent trailing twelve-month performance and 2026 guidance.

2025 / TTM FINANCIAL SNAPSHOT

SpaceX

Revenue: $18.67B

Net loss: -$4.94B

Starlink revenue: $11.4B (63% EBITDA margin)

FCF deficit: -$14B (AI capex driven)

Govt. share: ~20% of 2025 revenue

Tesla (trailing 12 months)

Revenue: ~$98B

GAAP net income: $3.9B (boosted by ~$1.6B reg credits)

Core earnings: ~$2.3B

2026 capex guide: $25B+

On a pro-forma combined basis, the merged group would currently print roughly negative $1 billion in GAAP earnings. That’s before adding the dilution effect of the SpaceX share issuance to consummate the deal.

Cash flow tells the same story.

SpaceX has openly acknowledged in its S-1 that it intends to spend on AI data center buildout “far in excess” of operating cash for an extended period. Tesla’s own capex burn is set to triple in 2026, reaching above $25 billion for the year, far above operating cash from its core businesses.

Stacked together, the two would need to absorb tens of billions in capital each year before the AI and robotics theses translate into earnings.

The Operating Overlap That Already Exists

For all the questions about whether a merger should happen, the operational reality is that Tesla and SpaceX already function as cousins, sharing personnel, board members, supply chains, and capital.

Elon Musk sits on both boards. So does venture capitalist Ira Ehrenpreis.

Musk’s brother Kimbal sits on Tesla’s board and previously sat on SpaceX’s. SpaceX directors Antonio Gracias and Steve Jurvetson have prior Tesla board service.

The two also share key technical leadership.

Charles Kuehmann, formerly of Apple, is vice president of materials engineering for both Tesla and SpaceX simultaneously.

Commercial transactions between the two companies are also substantial.

The SpaceX prospectus disclosed that it purchased $697 million worth of Tesla Megapack battery storage systems in 2024 and 2025 to power xAI’s Colossus data center campus near Memphis, Tennessee.

In 2025 SpaceX also spent $131 million on Tesla Cybertrucks for internal use. Earlier years featured Tesla buying solar equipment, leasing SpaceX private jets, and leaning on the rocket maker to develop a stainless alloy used in the Cybertruck.

Suppliers already treat the various Musk entities like a single customer in some cases.

In 2024 Nvidia agreed to divert a $500 million GPU order from Tesla to xAI at Musk’s request, an episode that underscored the porous corporate boundaries.

In March 2026, Tesla, SpaceX, and xAI jointly announced Terafab, a chip fabrication partnership intended to produce custom silicon for AI and robotics.

This collaboration is one of several signals fueling expectations that a formal corporate combination is on the horizon.

PUBLICLY DISCLOSED INTERCOMPANY ACTIVITY

- Tesla Megapacks sold to SpaceX: $697M (2024-2025)

- Cybertrucks bought by SpaceX: $131M (2025)

- Tesla investment in xAI: $2B (Jan 2026)

- Nvidia GPU order redirected

from Tesla to xAI at Musk request: $500M (2024)

- Shared engineering: Kuehmann (VP Materials, both)

- Overlapping directors: Musk, Ehrenpreis, etc.The Strategic Case for Combining

Supporters of the merger argue that the two companies are converging on the same underlying problem: building, deploying, and monetizing AI infrastructure at planetary scale.

Treating them as one balance sheet is, in this view, an efficiency upgrade rather than a financial maneuver.

For instance, Tesla has to run powerful AI systems inside a moving vehicle subject to tight constraints on power, cooling, latency, reliability, and cost.

SpaceX, meanwhile, has to think about compute in orbit, where radiation, thermal cycling, launch mass, power generation, and heat rejection become existential design constraints.

The two problems require deeply related engineering solutions.

The data backs up the convergence story too.

SpaceX disclosed in its filing that more than three-quarters of its $10.1 billion in quarterly capital expenditures were tied to AI infrastructure rather than rockets.

Tesla, on the parallel track, has guided that its own AI spending will more than triple in 2026 to fund Optimus humanoid robots, autonomous-driving compute, and the Dojo training cluster.

The merged entity would, in theory, be able to centralize chip procurement, data center construction, and AI talent recruiting under one capital allocator.

STRATEGIC SYNERGIES MOST FREQUENTLY CITED

1. Unified AI capex allocation across robotics, autonomy,

space compute, and large language model training.

2. Shared GPU and custom silicon sourcing (Terafab).

3. Common autonomy stack between Tesla FSD,

Optimus, and SpaceX flight systems.

4. Vertical energy stack: Tesla Megapacks powering

xAI Colossus and future orbital compute.

5. Brand and capital markets leverage (one big ticker).

6. Talent mobility across companies without I-9 friction.

Long-time Musk allies also argue that consolidation simplifies the CEO’s split focus.

Andrew Rocco of Zacks told Reuters that a single entity would align Musk’s attention and let him deploy resources more decisively rather than juggle corporate firewalls between entities he already controls.

Wedbush analyst Dan Ives, who puts the merger odds at 80 to 90 percent (in early 2027), has argued that the autonomous robotics business alone could add $1 to $2 trillion to a combined entity’s market capitalization, assuming Tesla can scale Optimus and full self-driving in line with stated targets.

The Self-Dealing Concern and Governance Mechanics

The merger conversation however, cannot be separated from governance questions about how the deal would actually get done.

This is the single most discussed risk among institutional investors, and it has already attracted litigation.

Musk holds roughly 20 percent of Tesla’s equity, while controlling 85.1 percent of SpaceX’s voting power through a super-voting share class disclosed in the S-1.

That asymmetry is at the heart of the self-dealing concern.

VOTING POWER ASYMMETRY (KEY GOVERNANCE FACT)

Tesla: Musk owns ~20% of equity (one share = one vote)

SpaceX: Musk controls ~85.1% of voting power via super-voting share class

SpaceX self-describes as a "controlled company" in S-1, which exempts it from certain Nasdaq corporate governance protections for public shareholders.

When a CEO sits on both sides of a negotiation, with disproportionate control on one side, terms are not negotiated at arm’s length. That’s the central concern.

Critics including several Tesla institutional holders have framed the proposed deal as the fourth time Musk has orchestrated a billion-dollar transaction between entities he controls.

The earlier three: the SolarCity acquisition in 2016, the xAI-X transaction in 2025, and the SpaceX-xAI combination in 2026.

The 2016 SolarCity deal was ultimately ruled fair by a Delaware court, but other Tesla directors agreed to a $60 million settlement without admitting fault. The Tesla board’s $2 billion xAI investment is the subject of an active shareholder lawsuit alleging breach of fiduciary duty.

Legal experts have argued that a SpaceX-Tesla merger would likely not raise antitrust issues, since the two compete in different markets, but it would almost certainly trigger contentious shareholder votes and potential Delaware litigation.

The questions are predictable:

Which company is the parent,

What is the exchange ratio,

Who decides the price, and

Whether minority shareholders are protected.

For Tesla, an additional procedural safeguard usually applies.

Special committees of independent directors typically negotiate related-party transactions, and Delaware case law gives stronger protection when a majority of disinterested shareholders also approve.

LIKELY GOVERNANCE STEPS IN A TESLA–SPACEX MERGER

1. Tesla forms special committee of independent directors.

2. Committee retains its own banker and counsel.

3. Fairness opinion delivered to each board.

4. SpaceX board approves (low friction; Musk 85% voting).

5. Tesla board approves on committee recommendation.

6. Majority-of-the-minority vote at Tesla.

7. SEC review, antitrust filings, foreign approvals.

8. Closing typically 6-12 months later.

Whether the Tesla independent committee acts robustly will be the single most-watched governance question of the next twelve months.

Past Musk-related transactions have not always produced the cleanest committee processes, which is precisely what motivates the skepticism in some institutional circles.

Tesla’s Position Heading Into a Potential Deal

To understand why a merger might be attractive to Tesla shareholders right now, look at the recent operating trajectory. The picture is not as strong as Tesla’s market value implies.

Tesla’s GAAP net income has fallen materially from a 2023 peak of $15 billion to roughly $3.9 billion on a trailing-twelve-month basis.

Strip out regulatory credit sales and Bitcoin gains, and core earnings approach roughly $2.3 billion.

At the same time, Tesla is preparing for a capital expenditure surge.

Management’s own guidance is that capex will roughly triple in 2026 versus 2025, exceeding $25 billion for the year. The bulk of that increase is tied to Optimus production tooling, expanded data center footprint, and the Terafab silicon project.

The Tesla shareholder vote in November 2025 also approved a pay package for Musk that could reach $1 trillion in stock if all twelve operational and market-cap milestones are met.

The final tranche is unlocked when Tesla reaches an $8.5 trillion market capitalization.

TESLA OPERATING TRAJECTORY (2023 -> TTM 2026)

Year GAAP Net Income

2023 $15.0B

2024 $7.0B

TTM Q1'26 $3.9B (incl. ~$1.6B reg credits)

Core TTM ~$2.3B

CAPEX OUTLOOK

2024 actual ~$11B

2025 actual ~$10B

2026 guidance $25B+

A combination with SpaceX would, in effect, hand Tesla shareholders a slice of Starlink (the most profitable Musk-owned business), Falcon launch cash flow, and a significant stake in the AI compute and model layer through xAI.

It would also dilute exposure to the EV demand cycle that has pressured Tesla’s stock.

Skeptics counter that Tesla shareholders would also be importing $14 billion of SpaceX free cash flow deficit, the operational risk of Starship development, the political risk of Mars-scale promises, and the integration overhang of xAI’s well-publicized rebuild.

For Tesla pure-play investors, the deal is therefore not unambiguously good or bad.

It depends almost entirely on whether the new growth engines deliver, and that depends on execution that has historically slipped past Musk’s stated timelines.

SpaceX’s Side of the Equation

From the SpaceX vantage point, a merger with Tesla looks different.

The rocket and satellite group is being asked to issue paper equivalent to roughly its entire IPO float to take on a slower-growth, lower-margin business.

That said, SpaceX still has strong reasons to want Tesla.

The cash flows from the auto business, even if shrinking, are real and recurring. They could partially fund the AI buildout that the S-1 itself acknowledges will outpace operating cash for years.

SPACEX REVENUE COMPOSITION 2025

Starlink subscription/equipment: $11.4B (61%)

Government contracts: ~$3.7B (20%)

Commercial launch: ~$2.5B

xAI and other: ~$1.1B

Total: $18.67B

Net loss: -$4.94B

Starlink EBITDA margin: ~63%

Starlink remains the engine.

The service crossed 10.3 million paid subscribers globally in the first quarter of 2026, double the 5 million reported a year earlier. Revenue of $11.4 billion in 2025 carried a roughly 63 percent EBITDA margin.

Government contracts contributed approximately one-fifth of total SpaceX revenue in 2025, including national security launches, Starshield, and NASA’s Artemis lunar lander work. The customer concentration in U.S. government accounts is itself a risk factor disclosed in the prospectus.

The cash drain comes from xAI and from the satellite manufacturing buildout.

SpaceX is constructing additional data center capacity to host xAI’s Grok models, much of which is supplied by Tesla Megapacks.

Closing the loop by acquiring Tesla would internalize that supply chain.

Importantly, SpaceX’s compensation framework for Musk has two milestones attached: a $7.5 trillion market capitalization target and at least one million inhabitants on Mars.

Combining with Tesla would put the company materially closer to the first milestone immediately upon close.

Tesla Optimus, xAI, and the AI Story That Holds It Together

The entire merger thesis rests on one belief: that AI, robotics, and autonomy will transform both companies into something significantly more valuable than the sum of their current parts. Without that belief, the math collapses into something resembling a 1990s conglomerate.

Tesla’s primary AI bet is Optimus, the humanoid robot.

Musk has confirmed during the Q1 2026 earnings call that production will begin at Fremont in late July, with the Optimus V3 reveal pushed to later in the year.

The xAI side brings the foundation model itself.

Grok is deployed inside the X platform, sold via API, and trained on a large compute cluster known as Colossus near Memphis, Tennessee. The cluster’s GPU footprint expanded dramatically through 2025.

SpaceX’s contribution is the most exotic.

The company is exploring compute in orbit, the idea that future Starlink-class satellites could host AI inference workloads using direct solar power and radiate heat into space, partially bypassing terrestrial grid bottlenecks.

COMBINED AI STACK (POST-MERGER, HYPOTHETICAL)

Layer Owner Asset

Custom silicon Terafab Tesla+SpaceX+xAI JV

Data center power Tesla Megapack storage

Training compute xAI Colossus, Memphis

Inference compute SpaceX Future orbital tier

Foundation model xAI Grok family

Autonomy stack Tesla FSD v13+

Robotics platform Tesla Optimus V3

Satellite uplink SpaceX Starlink

Distribution xAI X social platform

The bull case is that no other company on Earth has access to every layer of this stack inside one corporate structure.

The bear case is that being vertically integrated across nine layers does not by itself produce profits, and that the total addressable market of $26.5 trillion claimed by SpaceX in its S-1 will attract the same fierce competition from Alphabet, Microsoft, Amazon, and Nvidia.

For investors evaluating the merger, the realistic test is whether the AI integration would actually be faster and cheaper inside a single corporate parent than under the current arrangement of arms-length agreements like Terafab.

The answer is not obvious.

Impact on Tesla Shareholders

Tesla shareholders face the most consequential decision in the company’s history, assuming a deal is formally proposed. They would be voting to fold the company they own into a structure where Elon Musk controls roughly 85 percent of the votes.

Bullish scenarios point to several upsides.

The combined entity gives Tesla shareholders meaningful exposure to Starlink, which is currently SpaceX’s sole profitable major business with attractive subscriber economics.

TESLA SHAREHOLDER POTENTIAL UPSIDES

- Exposure to Starlink (63% EBITDA margins)

- Exposure to xAI / Grok foundation model

- Shared AI capex (lower marginal cost to Tesla)

- Reduced executive split focus

- Reflexive valuation boost from Musk "consolidation premium"

TESLA SHAREHOLDER POTENTIAL DOWNSIDES

- Loss of Tesla-only pure-play exposure

- Heavy dilution from SpaceX paper at $1.75T price

- Reduced voting influence (super-voting shares)

- Importing $14B FCF deficit from SpaceX

- Heightened related-party litigation risk

- Slower governance reform (controlled-company exemptions)

Bearish scenarios focus on price.

If SpaceX uses its IPO-inflated paper to acquire Tesla without a meaningful premium, Tesla shareholders effectively swap an arguably stretched valuation for a more stretched one.

Critics argue the deal would transfer Tesla’s overvaluation burden onto SpaceX rather than resolve it.

The dilution mathematics are unforgiving too.

To consummate the merger at parity, SpaceX would issue paper equivalent to 94 percent of its current share count. That immediately pushes any combined-entity earnings per share even lower than the depressing pro-forma figures already imply.

There is also the practical question of what happens to TSLA as a stock.

If Tesla is absorbed into SpaceX, the ticker disappears in its current form, replaced by a position in SPCX. Index funds tracking the S&P 500 would face significant rebalancing.

The point is that Tesla shareholders need to evaluate whether the swap delivers more long-term value than holding the standalone company, considering both the upside synergies and the very real concentration of governance power.

Impact on Prospective SPCX Investors

Investors thinking about buying SPCX at the IPO are also affected. The valuation they pay assumes one of several scenarios, and the merger discussion changes the probability weighting.

If SPCX prices at $1.75 trillion in mid-June and a Tesla deal follows within 12 to 18 months, new SPCX holders would experience material dilution.

They would own a smaller percentage of a larger but slower-growing business.

SPCX IPO RISK FACTORS DIRECTLY RELEVANT TO A MERGER

- "Controlled company" status (Musk ~85% voting)

- Significant related-party transactions disclosed

- Stated AI capex above operating cash for "extended period"

- Customer concentration in U.S. government contracts

- xAI loss profile materially impacting consolidated P&L

- Tesla intercompany activity grew >5x in 2024-2025

On the other hand, the same combination could meaningfully reduce SpaceX’s risk profile.

Tesla brings nearly $100 billion in annual revenue, a global manufacturing footprint, and a brand with consumer recognition that no satellite or rocket company has ever achieved.

Investors who think Tesla’s robotics and autonomy bets will eventually pay off may see the merger as a discounted way to gain that exposure inside the same equity they already plan to own.

The decision turns on a single judgment: whether Musk’s track record of operating execution is best valued as one diversified asset, or as several specialized assets with appropriate discounts and premia.

Regulatory, Legal, and Macro Considerations

A combination of this size and structure attracts more than ordinary regulatory attention, even if antitrust is unlikely to be a primary obstacle.

Antitrust scrutiny would focus on whether the merged firm gives either side leverage that previously didn’t exist. Since Tesla and SpaceX serve mostly non-overlapping customers, vertical concerns are more likely than horizontal ones.

REGULATORY AND LEGAL CHECKPOINTS

1. SEC review of proxy and registration statements

2. Hart-Scott-Rodino antitrust filing (DOJ/FTC)

3. CFIUS review (national security; SpaceX has DOD contracts)

4. EU and UK merger control (Starlink, Tesla operations)

5. Delaware Chancery Court (related-party suit risk)

6. NHTSA, FAA, FCC sector regulators

POTENTIAL LITIGATION CATALYSTS

- Existing xAI lawsuit (Tesla shareholders)

- Likely new appraisal-rights actions

- Class actions if Tesla minority shareholders dissent

- Foreign shareholder claims (Norway sovereign fund, others)

CFIUS review could be substantial.

SpaceX is a critical national security contractor for the Pentagon, NRO, and Space Force. Any change in beneficial ownership tied to foreign-source SpaceX capital, which is heavily anonymized post-IPO, would receive scrutiny.

Delaware Chancery is the more probable battleground.

The court is already familiar with Musk-related party transactions following the SolarCity ruling and the multi-year Tesla pay package litigation that ended in shareholder re-approval in November 2025.

Tesla’s reincorporation to Texas, completed in 2024, shifts some governance disputes to that jurisdiction. Texas courts have less developed corporate case law on conflicted controller transactions, which is itself a variable in how shareholder challenges might play out.

International regulatory approval is another wild card.

European authorities have been more aggressive than U.S. regulators on tech consolidation, and Starlink’s growing footprint in the EU could attract additional review.

What to Watch Next as an Investor

For investors trying to follow the story, several specific events between June 2026 and mid-2027 will provide signal.

KEY UPCOMING SIGNALS

- Jun 12, 2026 Possible SpaceX (SPCX) Nasdaq debut

- Jul-Aug 2026 Optimus production start at Fremont

- Q3 2026 SpaceX first earnings as public co.

- Late 2026 Optimus V3 reveal (per Musk)

- 2026 year-end Possible Tesla–SpaceX deal announcement

- Q1 2027 Likely formal merger proxy (if announced)

- Mid-2027 Targeted close (if announced 2026 year-end)

Watch for a Tesla 8-K disclosing the formation of a special committee. That’s the earliest concrete signal that the board is contemplating a formal proposal.

Watch the SpaceX SPCX share price relative to its IPO benchmark. If SPCX trades materially above the IPO price, the implied exchange ratio becomes more dilutive for SpaceX original holders, which strengthens any pushback inside SpaceX.

Watch Tesla insider stock sales and the timing of Musk’s tranches under the trillion-dollar pay package. The package vests on market-cap milestones, which the merger may accelerate.

Watch litigation too. The pending Tesla shareholder suit over the xAI investment is a leading indicator of how aggressive minority Tesla holders will be in opposing or seeking modifications to any merger.

Also, watch government contract disclosures from SpaceX. National security customers may quietly object to a structure that places critical launch and satellite capacity inside a publicly traded conglomerate with material consumer-product exposure.

The Bigger Picture: One Empire, Many Risks

The proposed SpaceX-Tesla merger, if it happens, would represent the culmination of nearly two decades of Musk corporate strategy.

It would also concentrate an unprecedented amount of operational, financial, and political risk inside one ticker.

The bull case is that the combined company becomes the dominant builder and operator of physical AI: cars, robots, satellites, energy storage, foundation models, social distribution, and orbital launch all inside one capital structure.

The bear case is that the combined company is a debt-and-dilution machine whose valuation already depends on stories about Mars, robotaxis, and orbital data centers that have repeatedly slipped past their stated timelines.

BOTTOM LINE FOR INVESTORS

- Probability range (analyst & market): 33-90% over 12-18 months

- Combined valuation if signed at parity: ~$3.4 trillion

- Combined GAAP earnings (TTM pro-forma): roughly -$1B

- Combined free cash flow gap (TTM): tens of billions

- Governance risk: very high (controlled-company status)

- Litigation risk: very high (related-party transaction)

- Execution upside if AI capex monetizes: very high

What seems clear from the public record is that neither Musk nor his closest allies have ruled the deal out, and several have actively promoted the logic of it. The disclosures in the SpaceX S-1 are themselves consistent with preparing the ground for further consolidation.

What is equally clear is that the deal, if it happens, will be the largest test of related-party transaction governance in American corporate history. The result will shape how controlled-company structures, dual-class shares, and CEO compensation reform are litigated for the next decade.

For investors, the most useful posture is informed neutrality. Owning the right number of shares of either company, with full awareness of the dilution and governance mechanics, is more durable than betting on a specific outcome.

The next 12 to 18 months will likely answer the question one way or the other. Either Tesla and SpaceX combine in the largest merger ever attempted, or Musk leaves them parallel and the speculation finally subsides.

Either outcome will move trillions of dollars in market value.

That alone is reason enough for investors in both companies, and prospective SPCX buyers, to track the disclosures carefully.