Wolfspeed - SWOT Analysis Report (2026)

Wolfspeed SWOT analysis 2026: Fresh from bankruptcy, can this SiC leader overcome Chinese rivals and capacity challenges? Critical insights for investors.

Wolfspeed $WOLF ( ▲ 4.88% ) emerges from one of the semiconductor industry’s most dramatic restructurings just as the silicon carbide revolution reaches a critical inflection point.

The Durham, North Carolina-based pioneer filed for Chapter 11 bankruptcy protection on June 30, 2025, and emerged 91 days later on September 29, 2025, having eliminated $4.6 billion in debt.

For investors analyzing the company’s prospects, the question isn’t whether silicon carbide technology will transform power electronics.

The question is whether Wolfspeed can capitalize on its technological leadership while navigating intense competition from Chinese rivals, operational challenges at its new manufacturing facilities, and uncertainty surrounding government funding that underpins its expansion plans.

Table of Contents

Understanding Wolfspeed’s Business Model

Core Operations and Technology Leadership

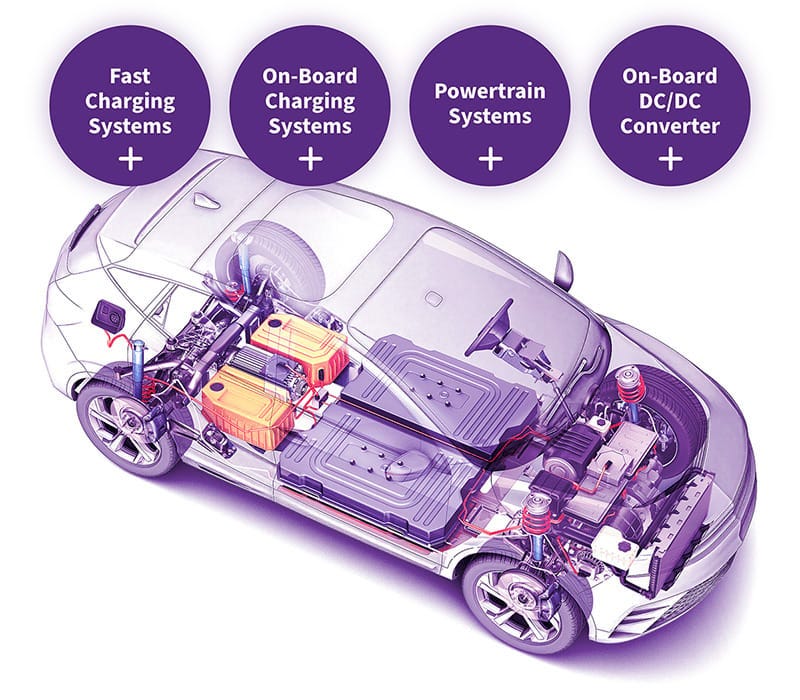

Wolfspeed operates as the sole vertically integrated manufacturer of 200mm silicon carbide substrates and devices in the world. This distinction matters profoundly. The company controls its entire supply chain, from growing silicon carbide crystals to fabricating finished power devices.

This vertical integration provides both cost advantages and quality control that competitors struggle to replicate.

The company’s technology addresses a fundamental limitation of traditional silicon semiconductors. Silicon carbide devices can handle higher voltages, operate at higher temperatures, and switch faster than conventional silicon.

These properties translate directly into more efficient power conversion systems across multiple applications.

Business Segment

Primary Products

Key Applications

Materials

150mm and 200mm SiC wafers (bare and epitaxial)

Substrate supply to device manufacturers

Power Devices

SiC MOSFETs, diodes, power modules

EV traction inverters, onboard chargers, industrial motor drives

Renewable Energy

Power conversion solutions

Solar inverters, energy storage systems, wind power

Silicon carbide offers up to 4% higher power efficiency compared to traditional silicon in various power applications.

For electric vehicles, this translates to extended driving range, faster charging times, and reduced battery costs. For industrial applications, it means smaller, lighter power systems that generate less heat.

Manufacturing Infrastructure and Capacity

Wolfspeed operates multiple manufacturing facilities with distinct roles. The company’s Mohawk Valley Fab in Marcy, New York, represents the world’s first and largest fully automated 200mm silicon carbide device fabrication facility. This $1 billion facility opened in April 2022 and currently operates at approximately 20-25% utilization.

The John Palmour Manufacturing Center for Silicon Carbide in Siler City, North Carolina, remains under construction. This $5 billion materials facility will produce 200mm silicon carbide wafers when it becomes operational. The facility represents the largest single manufacturing investment in North Carolina’s history.

In Durham, North Carolina, Wolfspeed maintains its headquarters and legacy manufacturing operations. The company recently announced plans to consolidate device production at the Mohawk Valley facility, closing its older Durham device manufacturing line to improve operational efficiency.

The transition to 200mm wafer technology represents a critical strategic move. Larger wafers allow more devices per wafer, reducing per-unit manufacturing costs. Wolfspeed commercially launched its 200mm silicon carbide materials portfolio in September 2025, marking a significant technological milestone.

Financial Performance and Restructuring Outcomes

The bankruptcy restructuring fundamentally transformed Wolfspeed’s balance sheet. The company reduced its debt by approximately 70%, from $6.7 billion to roughly $2 billion. Annual cash interest costs decreased by about 60%, improving the company’s ability to fund operations during this critical ramp-up phase.

Financial Snapshot: Fiscal Q1 2026 (ended September 28, 2025)

Revenue: $196.8 million

Gross Margin: (39%)

Operating Expenses: $171.1 million

Capital Expenditures: Reduced to $150-200M annually (from previous $1B+ run rate)

Liquidity: Approximately $1.5 billion (including $698.6M CHIPS Act tax refund)

Revenue declined 6.14% year-over-year in fiscal 2025, falling from $807.2 million to $757.6 million. The first quarter of fiscal 2026 showed a modest 1.08% revenue increase compared to the prior quarter, but the company continues operating with negative gross margins due to significant underutilization of its new manufacturing capacity.

The company faces substantial doubt about its ability to continue as a going concern, according to management’s own assessment. This designation reflects the operational and financial headwinds that persist despite the successful restructuring.

Strengths: Technological Leadership and Strategic Positioning

Unmatched Vertical Integration

Wolfspeed’s position as the only vertically integrated 200mm silicon carbide manufacturer creates significant competitive advantages. The company controls material quality from crystal growth through device fabrication, allowing for optimization across the entire value chain. Competitors must either rely on external substrate suppliers or invest billions to replicate this integration.

This vertical structure also provides flexibility in capacity allocation. During periods of strong device demand, Wolfspeed can prioritize internal consumption. When external substrate demand strengthens, the company can increase material sales. This optionality provides strategic advantages that horizontally integrated competitors cannot match.

Blue-Chip Customer Portfolio

Wolfspeed has secured design wins and supply agreements with major automotive OEMs that validate its technology leadership. In December 2025, the company announced it powers Toyota’s electric vehicle platforms with its silicon carbide components. This relationship represents a significant strategic achievement, as Toyota remains among the world’s largest automotive manufacturers.

The company’s customer base extends beyond Toyota. Wolfspeed maintains strategic partnerships with several industry leaders:

Customer/Partner

Agreement Type

Strategic Significance

General Motors

10-year strategic supply agreement (Oct 2021)

Direct OEM relationship for EV programs; $2B estimated value

Jaguar Land Rover

Strategic partnership (Oct 2022)

SiC semiconductor supply for next-generation EVs

Renesas Electronics

10-year wafer supply agreement (Jul 2023)

150mm scaling to 200mm; major Japanese semiconductor company

BorgWarner

$500M investment with capacity corridor

Tier 1 automotive supplier relationship

ZF Friedrichshafen

Strategic partnership

Major automotive systems supplier

These relationships provide both revenue visibility and market validation. Major OEMs conduct exhaustive qualification processes before selecting power semiconductor suppliers. Once qualified, switching costs create substantial barriers to competitive displacement.

Tesla’s early adoption of silicon carbide chips in its powertrains demonstrated the technology’s advantages and helped establish the market. While Wolfspeed doesn’t publicly disclose Tesla as a customer, the broader industry adoption that Tesla catalyzed benefits all silicon carbide suppliers.

www.deepresearchglobal.com/p/tesla-swot-analysis

Advanced Manufacturing Technology

The Mohawk Valley Fab represents a technological leap in semiconductor manufacturing automation. The facility operates as a fully automated 200mm silicon carbide fabrication line, incorporating advanced process control systems and Industry 4.0 manufacturing principles.

This automation provides several competitive advantages. Labor costs per wafer decrease significantly compared to manual operations. Process consistency improves, leading to higher yields and better device performance. The facility can scale production efficiently as demand increases without proportional increases in operating costs.

Wolfspeed’s fourth-generation silicon carbide MOSFET technology delivers meaningful performance improvements. The company’s Gen 4 devices offer lower on-resistance, improved switching characteristics, and enhanced reliability compared to previous generations. These technical advantages translate directly into customer value through more efficient, more reliable power systems.

Government Support and Strategic Funding

Wolfspeed secured $750 million in proposed funding from the U.S. CHIPS and Science Act in October 2024. This federal support aims to bolster domestic semiconductor manufacturing capacity and reduce dependence on foreign suppliers. The funding supports both the New York fab expansion and the North Carolina materials facility.

Beyond direct grants, Wolfspeed has received $698.6 million in cash tax refunds under the CHIPS Act’s advanced manufacturing investment tax credit. These funds arrived in late 2025, significantly improving the company’s liquidity position at a critical time. The company expects to receive more than $600 million in additional cash tax refunds during fiscal year 2026.

An investment group led by Apollo Global Management committed an additional $750 million in private funding alongside the government support. This combination of public and private capital provides the financial resources necessary to complete Wolfspeed’s ambitious capacity expansion.

The strategic nature of silicon carbide technology for national security and economic competitiveness provides some protection against funding cuts. The Department of Defense relies on wide-bandgap semiconductors for military applications, and the automotive industry’s transition to electric vehicles depends on access to these materials.

Market Position in Silicon Carbide Substrates

Despite intensifying competition, Wolfspeed maintained a 34% market share in the global silicon carbide substrate market in 2024, according to TrendForce. This leadership position provides both pricing power and market influence.

The company’s decades of experience growing silicon carbide crystals create knowledge advantages that competitors struggle to replicate. Crystal growth requires specialized expertise in materials science, thermal management, and process control. Defect density in silicon carbide wafers remains a critical challenge, and Wolfspeed’s long development history provides advantages in this area.

Weaknesses: Operational Challenges and Financial Pressure

Severe Capacity Underutilization

Wolfspeed’s most significant operational challenge stems from dramatic underutilization of its expensive new manufacturing capacity. The Mohawk Valley Fab operates at approximately 20-25% utilization, well below the 70-80% levels typically required for profitability in semiconductor manufacturing.

This underutilization creates a vicious cycle. The company incurs substantial fixed costs for facility depreciation, maintenance, utilities, and base staffing regardless of production volume. These costs flow through to negative gross margins, consuming cash that the company needs to fund operations and complete its expansion projects.

Capacity Utilization Impact on Financial Performance

Fixed Facility Costs: ~$200M+ annually (depreciation, maintenance, base operations)

Current Utilization: 20-25%

Revenue Generation: Insufficient to cover allocated fixed costs

Result: (39%) gross margin in Q1 FY2026

Path to Profitability Requires: 60-70%+ utilization for positive gross margins

The timing mismatch between capacity investment and demand realization creates profound financial stress. Wolfspeed invested billions building state-of-the-art facilities based on demand projections that assumed faster electric vehicle adoption. When EV market growth slowed in 2024-2025, demand materialized more gradually than anticipated, leaving the company with expensive idle capacity.

Persistent Revenue Decline

Wolfspeed has experienced declining revenue for consecutive quarters, reflecting both market challenges and operational constraints. Fiscal year 2025 revenue fell 6.14% to $757.6 million from $807.2 million in fiscal 2024. This downward trajectory continued into fiscal 2026, with management projecting Q2 fiscal 2026 revenue of $150-190 million.

Several factors drive this revenue decline. The company intentionally shut down older, less efficient production lines as part of its transition to 200mm technology. While strategically sound long-term, this consolidation temporarily reduced available capacity. Customer qualification timelines for new 200mm devices extended longer than anticipated, delaying revenue ramps from the Mohawk Valley facility.

The automotive market slowdown, particularly in electric vehicles, reduced order volumes from key customers. Some automotive OEMs adjusted their EV production plans downward in response to weaker consumer demand, directly impacting Wolfspeed’s device shipments.

Fiscal Period

Revenue

Year-over-Year Change

FY2024

$807.2M

(baseline)

FY2025

$757.6M

-6.14%

Q1 FY2026

$196.8M

-5.57% (TTM basis)

Q2 FY2026 (guidance)

$150-190M

Continued decline expected

Going Concern Uncertainty

Management’s substantial doubt about the company’s ability to continue as a going concern represents a significant red flag for investors. This accounting designation doesn’t mean bankruptcy is imminent, particularly given the recent restructuring, but it signals that management recognizes serious risks to the company’s viability.

Several factors contribute to this assessment. The company continues burning cash to fund operations and complete its expansion projects. While liquidity improved significantly with the CHIPS Act tax refunds, the path to self-sustaining profitability remains uncertain and dependent on factors partially outside management’s control.

The company must successfully ramp production at the Mohawk Valley facility, qualify new customers for 200mm devices, and achieve sufficient volume to cover fixed costs. If any of these critical milestones encounter significant delays, liquidity could become constrained before the company achieves profitability.

Complex Fresh-Start Accounting

Wolfspeed’s emergence from bankruptcy triggers fresh-start accounting requirements under U.S. GAAP. This accounting treatment essentially revalues all assets and liabilities at fair market value, creating a new basis for financial reporting. The company expects these adjustments to materially impact its balance sheet in Q2 fiscal 2026.

Fresh-start accounting creates several complications for investors. Historical financial metrics become difficult to compare with post-emergence results. Asset valuations may include significant write-downs, particularly for property, plant, and equipment at facilities operating well below capacity. These non-cash charges impact book value and various financial ratios that investors use for analysis.

The bankruptcy also resulted in complete cancellation of legacy common shares, with new equity issued to creditors and existing shareholders receiving only approximately 1.3 million new shares. This substantial dilution means pre-bankruptcy shareholders retained minimal ownership in the restructured company.

Limited Margin for Execution Errors

Wolfspeed operates with essentially no margin for error during this critical period. The company must execute flawlessly on multiple fronts simultaneously. Any significant setback in customer qualification, manufacturing ramp-up, or technology development could jeopardize the entire restructuring plan.

The pressure extends to external factors as well. Significant delays in CHIPS Act funding disbursement, changes in government policy, or shifts in customer demand could create liquidity pressure before the company reaches sustainable profitability. Management has limited ability to adjust course quickly given the capital-intensive nature of semiconductor manufacturing.

Opportunities: Market Growth and Strategic Expansion

Accelerating Electric Vehicle Adoption

Despite the recent slowdown, long-term electric vehicle adoption trends remain strongly positive. Multiple governments maintain aggressive electrification mandates. The European Union, California, and several other jurisdictions have established timelines for phasing out internal combustion engine vehicles. China continues pushing EV adoption through subsidies and regulatory requirements.

By 2027, over 50% of battery electric vehicles could rely on silicon carbide powertrains, compared with approximately 30% currently, according to McKinsey analysis. This penetration increase represents billions of dollars in potential revenue for silicon carbide device manufacturers.

The transition from 150mm to 200mm silicon carbide wafers will substantially reduce costs per device, making the technology accessible to a broader range of vehicle price points. Premium and luxury EVs already incorporate silicon carbide extensively. As costs decline, mainstream and economy EVs will increasingly adopt the technology, dramatically expanding the addressable market.

EV Market Opportunity Drivers

Global EV Sales Projections: 20M+ units annually by 2026

SiC Content per Vehicle: $300-500 in traction inverter and OBC

Penetration Rate: Increasing from 30% to 50%+ by 2027

Potential Annual Market Size: $3-5B for SiC devices in automotive by 2027

Wolfspeed Target Share: 15-20% market share potential

Industrial and Renewable Energy Applications

While electric vehicles capture headlines, industrial applications and renewable energy systems represent substantial growth opportunities for silicon carbide technology. Industrial motor drives, data center power supplies, and renewable energy inverters all benefit from silicon carbide’s efficiency advantages.

Solar energy systems require highly efficient inverters to convert DC power from panels to AC power for the grid. Silicon carbide devices enable smaller, more efficient inverters that reduce installation costs and improve energy harvest. As solar installations scale globally, demand for silicon carbide in renewable applications grows proportionally.

Energy storage systems represent another significant opportunity. Grid-scale and commercial battery storage requires sophisticated power conversion systems. Silicon carbide enables bidirectional inverters that efficiently charge and discharge battery systems, improving overall system economics.

Application Segment

SiC Advantages

Growth Drivers

Solar Inverters

Higher efficiency, smaller size, improved reliability

Global renewable energy mandates, cost reduction

Energy Storage

Bidirectional power flow, high efficiency

Grid modernization, renewable integration

Industrial Motor Drives

Energy efficiency, reduced cooling requirements

Factory automation, energy cost reduction

Data Center Power

High power density, improved efficiency

AI computing growth, sustainability requirements

The industrial market exhibits less volatility than automotive, providing revenue diversification. Many industrial customers prioritize total cost of ownership over initial component costs, making them receptive to premium-priced silicon carbide devices that deliver operational savings.

Capacity as a Strategic Asset

Wolfspeed’s current capacity underutilization represents a significant near-term weakness, but this same capacity becomes a powerful strategic asset when demand accelerates. The company has largely completed its major capital investments. The Mohawk Valley facility exists and operates. The Siler City materials facility nears completion.

When demand materializes, Wolfspeed can scale production rapidly without requiring years of construction and qualification. Competitors attempting to enter the market or expand capacity must invest billions and wait 2-3 years for new facilities to become operational. This time advantage could prove decisive in a rapidly growing market.

The capital-light phase that Wolfspeed now enters also improves financial dynamics. The company has reduced annual capital expenditures to approximately $150-200 million for fiscal 2026-2027, down from previous run rates exceeding $1 billion annually. This reduction allows the company to focus available capital on operations, customer qualification, and technology development rather than facility construction.

Image source: wolfspeed.com

Technology Leadership in Next-Generation Devices

Wolfspeed continues investing in advanced device architectures and manufacturing processes. The company’s Gen 4 silicon carbide MOSFET technology delivers substantial performance improvements, and the development pipeline includes further innovations.

Advanced packaging technologies represent one key opportunity. Traditional discrete devices give way to integrated power modules that combine multiple devices with sophisticated thermal management and gate drive circuitry. Wolfspeed’s power module offerings address customer demand for turnkey solutions that simplify system design and improve reliability.

The transition to 200mm wafer technology provides a platform for sustained cost reduction through improved manufacturing efficiency. As production volumes increase and learning curves advance, per-unit costs will decline, enabling Wolfspeed to either improve margins or pass savings to customers to accelerate market penetration.

Geographic Expansion and Supply Chain Resilience

Growing geopolitical tensions and supply chain concerns drive customers to prioritize geographic diversification. Wolfspeed’s concentrated U.S. manufacturing presence provides advantages as customers seek to reduce dependence on Asian suppliers. Both automotive OEMs and industrial customers increasingly value North American and European supply sources.

The company maintains operations in Europe and Asia for customer support and sales, but its manufacturing concentration in the United States differentiates it from many competitors. As governments implement domestic content requirements and customers prioritize supply chain resilience, this geographic positioning could provide competitive advantages.

Wolfspeed’s planned (though currently paused) facility in Saarland, Germany, would further enhance its geographic diversity when economic conditions improve sufficiently to proceed with the investment. European automotive customers particularly value local supply sources given the continent’s stringent environmental regulations and industrial policy priorities.

Threats: Competition, Market Dynamics, and External Risks

Intensifying Chinese Competition

Chinese silicon carbide manufacturers have emerged as formidable competitors, claiming nearly 40% of the global substrate market by 2025. TankeBlue and SICC each hold approximately 17% market share, rapidly closing the gap with Wolfspeed’s 34% share.

Chinese competitors benefit from substantial government support, lower labor costs, and aggressive pricing strategies. The Chinese government views wide-bandgap semiconductors as strategically important and provides funding, subsidies, and policy support to domestic manufacturers. This support allows Chinese companies to underprice Western competitors while investing heavily in capacity expansion.

Quality and reliability concerns have historically limited Chinese suppliers’ penetration in demanding automotive applications, but this advantage erodes as Chinese manufacturers improve their processes and gain experience.

Several Chinese silicon carbide companies now pursue automotive qualifications with global OEMs, potentially threatening Wolfspeed’s customer relationships.

Competitor

Region

Market Share (2024)

Key Strengths

Wolfspeed

United States

34%

Technology leadership, vertical integration, established customers

TankeBlue

China

17.3%

Government support, cost advantages, rapid expansion

SICC

China

17.1%

Aggressive pricing, domestic market access, scale

STMicroelectronics

Europe

~10-15% (devices)

Diversified portfolio, automotive relationships, European base

ON Semiconductor

United States

~10-15% (devices)

Broad product portfolio, established distribution

The combined Chinese market share trajectory concerns Western manufacturers. In 2021, Chinese companies controlled only 10% of the silicon carbide substrate market. By 2025, this share reached nearly 40%, demonstrating extremely rapid growth.

If this trend continues, Chinese manufacturers could dominate the substrate market within several years, potentially leveraging this position to expand into devices.

onsemi (ON Semiconductor) - SWOT Analysis Report (2026)

www.deepresearchglobal.com/p/onsemi-swot-analysis-report

Electric Vehicle Market Volatility

The recent EV market slowdown demonstrates the cyclical risk inherent in Wolfspeed’s automotive-heavy business mix. Multiple factors contribute to reduced EV adoption rates including higher interest rates, reduced government incentives in some markets, charging infrastructure constraints, and consumer concerns about vehicle range and resale values.

This slowdown materialized precisely when Wolfspeed needed strong demand to fill its new manufacturing capacity. The timing mismatch between the company’s multi-billion dollar capacity investments (made based on aggressive EV adoption projections) and actual market development creates profound financial pressure.

Automotive demand exhibits high cyclicality even without the additional uncertainty of new technology adoption. Economic downturns reduce vehicle sales across all categories. The transition to electric vehicles adds uncertainty about the pace and pattern of adoption. Some forecasts prove overly optimistic, as recent experience demonstrates.

The concentration of Wolfspeed’s revenue in automotive applications amplifies this cyclical exposure. While diversification into industrial and renewable energy applications helps, automotive relationships represent the company’s most significant revenue opportunities and customer relationships.

Established Semiconductor Competitors

Beyond Chinese startups, Wolfspeed faces competition from major established semiconductor manufacturers with far greater financial resources. STMicroelectronics, Infineon Technologies, and ON Semiconductor all pursue silicon carbide aggressively, each bringing distinct competitive advantages.

STMicroelectronics leads the silicon carbide device market with approximately 32.6% share in 2023, according to industry analysis. The European giant benefits from diversified operations, strong European automotive relationships, and substantial financial resources. STMicroelectronics can absorb losses in silicon carbide while ramping volumes, cross-subsidizing the business with profits from other product lines.

Infineon Technologies brings similar advantages with its broad product portfolio and established automotive customer base. The German company maintains relationships with virtually every major automotive OEM globally. Infineon can offer customers complete semiconductor solutions, bundling silicon carbide devices with other products to win design sockets.

ON Semiconductor acquired GT Advanced Technologies’ silicon carbide business, gaining substrate capabilities to complement its device operations. The company’s diversified business model and strong financial position allow aggressive investment in silicon carbide despite near-term profitability challenges.

These established competitors possess advantages that Wolfspeed cannot easily match. Their diversified revenue streams provide financial flexibility during market downturns. Their existing customer relationships create opportunities to introduce silicon carbide alongside other products. Their established supply chains and manufacturing footprints allow them to serve global customers effectively.

CHIPS Act Funding Uncertainty

While Wolfspeed has received significant tax refunds under the CHIPS Act, the proposed $750 million direct grant remains subject to final negotiations and disbursement. Political changes and policy shifts create uncertainty about whether these funds will ultimately materialize as anticipated.

The return of different political priorities in 2026 introduces questions about continued support for semiconductor subsidies. While strategic considerations around supply chain security and technology leadership argue for sustained commitment, budget pressures and competing priorities could affect implementation.

Even if the funding proceeds as planned, disbursement typically occurs in tranches tied to specific milestones and construction progress. Delays in meeting requirements or changes in project timelines could defer cash receipts, potentially creating liquidity pressure during a critical period.

The uncertainty around CHIPS Act funding has previously triggered volatility in Wolfspeed’s stock price. Investors closely monitor announcements about program implementation and funding disbursement. Any negative developments could significantly impact market sentiment and the company’s ability to raise additional capital if needed.

Technology and Manufacturing Execution Risks

Silicon carbide manufacturing remains technically challenging despite decades of development. Crystal defects, process variations, and yield issues can dramatically impact costs and profitability. Any significant manufacturing problems at the Mohawk Valley facility or the Siler City materials plant could disrupt production and damage customer relationships.

The transition to 200mm wafer technology, while strategically essential, introduces execution risk. Larger wafers complicate crystal growth, increasing the likelihood of defects. Device fabrication processes developed for 150mm wafers require optimization for 200mm. Customer qualifications for 200mm devices take time and resources.

Wolfspeed’s vertically integrated model amplifies manufacturing risk. Problems at the materials level cascade through to devices. The company cannot easily source alternative substrates if its internal production encounters problems. This integration creates both cost advantages and concentration risk.

Competing technologies also pose potential threats. Gallium nitride (GaN) devices offer advantages for certain applications, particularly lower voltage power conversion. While silicon carbide dominates high-voltage automotive applications, GaN could capture significant market share in other segments. Next-generation silicon technologies could also improve, potentially reducing silicon carbide’s cost-performance advantages in some applications.

Image source: wolfspeed.com

Strategic Implications for Investors

Critical Success Factors for 2026 and Beyond

Wolfspeed’s path to sustainable profitability depends on executing several critical initiatives successfully. First, the company must substantially improve capacity utilization at the Mohawk Valley facility. Reaching 60-70% utilization would transform financial performance, converting negative gross margins to positive contributions that could fund operations and generate cash flow.

Customer qualification and production ramp timelines represent the second critical factor. Major automotive design wins must translate into volume production as qualified vehicles enter production. Industrial and renewable energy customers must adopt Wolfspeed’s 200mm devices, diversifying revenue beyond automotive applications.

The company must also complete construction of the Siler City materials facility and successfully ramp internal substrate production on 200mm technology. This vertical integration provides the cost structure and supply security necessary to compete effectively with Chinese manufacturers who benefit from lower labor costs.

Key Milestones to Monitor

Q1-Q2 2026:

- Mohawk Valley capacity utilization trajectory

- Customer qualification progress for 200mm devices

- CHIPS Act funding disbursement updates

- Quarterly revenue trends and gross margin improvement

H2 2026 - 2027:

- Siler City facility completion and ramp

- Major automotive program production starts

- Industrial/renewable energy revenue diversification

- Path to positive operating cash flow

Valuation Considerations and Investment Framework

Wolfspeed presents a complex valuation challenge. Traditional metrics like price-to-earnings ratios prove meaningless given persistent losses. The company’s going concern uncertainty and recent bankruptcy further complicate analysis. Asset values remain uncertain pending fresh-start accounting implementation.

Investors must evaluate Wolfspeed based on scenario analysis rather than conventional valuation methods. In a bull case where EV adoption accelerates, silicon carbide penetration increases, and Wolfspeed successfully ramps production, the company could generate substantial value. The installed manufacturing capacity, customer relationships, and technology leadership would position it to capture significant market share in a rapidly growing industry.

The bear case involves continued automotive weakness, intensifying Chinese competition, and execution challenges that prevent the company from reaching profitable operations. In this scenario, Wolfspeed might require additional financing (likely dilutive given the capital structure), or potentially face strategic alternatives including asset sales or merger discussions with better-capitalized competitors.

The base case suggests a multi-year period of operational challenges and financial pressure before the company reaches sustained profitability. Capacity utilization will improve gradually as automotive production ramps and industrial applications expand. The company will likely consume substantial cash during this period, relying on CHIPS Act funding and careful capital management to bridge to profitability.

Investment Considerations

Positive Factors

Risk Factors

Technology

Proven SiC leadership, 200mm capabilities

Evolving competitive technologies, execution risks

Market Position

Established automotive relationships, vertical integration

Chinese competitors, established semiconductor rivals

Financials

Reduced debt post-restructuring, CHIPS Act support

Negative cash flow, going concern uncertainty

Operations

World-class facilities, automation advantages

Severe underutilization, production ramp challenges

Strategic

Long-term EV/industrial growth trends

Near-term market volatility, funding dependencies

Risk Management and Portfolio Context

Given the substantial risks and uncertainties surrounding Wolfspeed, position sizing becomes critical for investors considering exposure. The company’s binary outcome potential (eventual success generating substantial returns versus continued struggles leading to further dilution or strategic restructuring) suggests treating it as a speculative position within a diversified portfolio.

Several risk management approaches merit consideration. Investors might limit Wolfspeed to a small percentage of overall portfolio value, acknowledging the high risk-reward profile. Alternatively, pairing Wolfspeed with larger, more stable semiconductor holdings could provide sector exposure while managing company-specific risk.

Monitoring specific operational metrics rather than stock price volatility provides better insight into fundamental progress. Quarterly capacity utilization trends, customer qualification announcements, and gross margin evolution offer more meaningful signals than short-term price movements driven by market sentiment.

The government funding situation requires careful attention. Any significant developments regarding CHIPS Act implementation, funding delays, or policy changes could materially impact Wolfspeed’s liquidity and strategic options. Investors should closely follow political and regulatory developments affecting semiconductor subsidies.

My Final Thoughts

Wolfspeed stands at a defining moment in its corporate history. The company has successfully navigated bankruptcy, emerging with a cleaner balance sheet and renewed focus on operational execution. Its manufacturing assets, technology leadership, and customer relationships position it to potentially capitalize on the long-term transition to silicon carbide power electronics.

The path forward remains fraught with challenges. Severe capacity underutilization generates substantial losses that consume cash and pressure liquidity. Chinese competitors advance rapidly, claiming market share with aggressive pricing and government support. The recent automotive market slowdown demonstrates the cyclical risks inherent in the company’s business mix.

For investors, Wolfspeed represents a high-risk, high-potential-reward opportunity rather than a conservative holding.

The company’s eventual success depends on multiple factors aligning favorably, including recovering EV demand, successful production ramps, effective competition with Chinese manufacturers, and continued government support. Any significant setback could jeopardize the restructuring plan and force additional strategic actions.

The investment thesis ultimately rests on conviction about long-term silicon carbide adoption trends and confidence in Wolfspeed’s ability to execute operationally during a challenging transition period.

Those who believe silicon carbide will inevitably capture significant market share from traditional silicon, and that Wolfspeed’s vertical integration and customer relationships provide durable competitive advantages, may view current challenges as temporary obstacles on a path to eventual success.

Conversely, investors concerned about Chinese competition, execution risks, or extended automotive market weakness should approach cautiously or avoid the stock entirely. The margin for error remains minimal, and the company must deliver successful execution across multiple dimensions simultaneously to justify optimistic scenarios.

The next 12-18 months will prove critical. Capacity utilization trends, customer qualification progress, and gross margin trajectory will provide definitive evidence about whether Wolfspeed can successfully transition from restructuring mode to growth mode.

Until these operational metrics demonstrate sustained improvement, the investment remains highly speculative regardless of the technology’s long-term promise.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with financial advisors before making investment decisions.