Coca-Cola - Company Overview, Analysis and Outlook Report (2026)

Coca-Cola company analysis: Q3 results show 6% organic growth, 32% margins. DCF models mixed. Read the deep dive on valuation, risks & catalysts for investors.

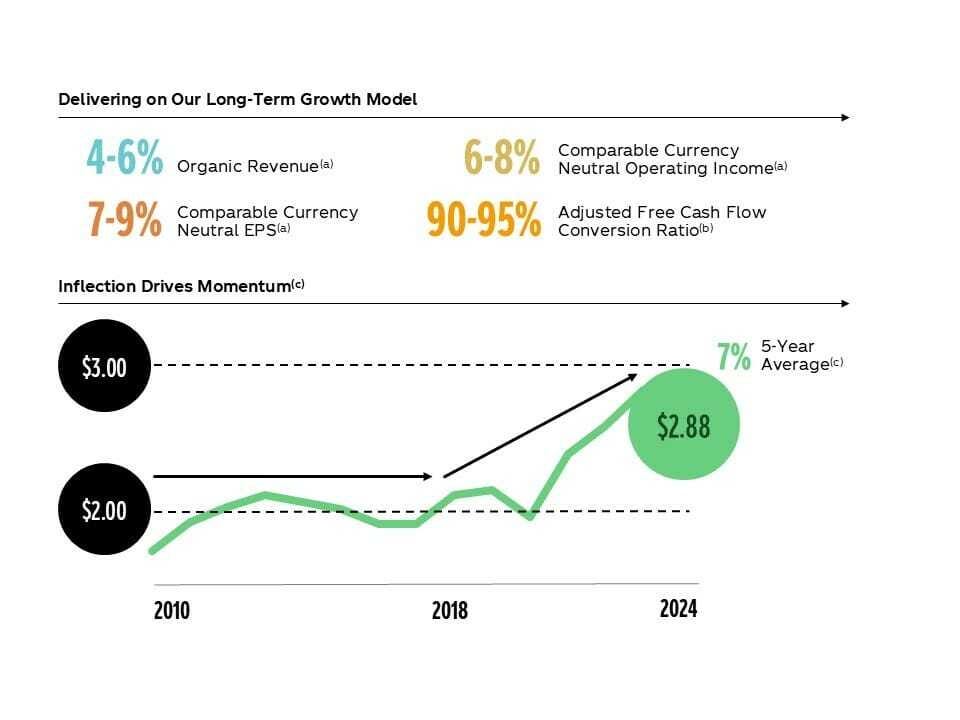

Executive TL;DR

Q3 2025 Performance: Coca-Cola $KO ( ▲ 0.11% ) delivered 6% organic revenue growth with net revenues reaching $12.5 billion, driven by 6% price/mix growth despite flat concentrate sales.

Financial Strength: Operating margin expanded to 32.0%, while comparable EPS grew 6% to $0.82, demonstrating pricing power amid challenging macro conditions.

2026 Outlook: Management projects 5-6% organic revenue growth with slight currency tailwinds, positioning the company for continued value creation.

Valuation Tension: Wall Street analysts set a consensus price target of $79.08, suggesting modest upside from current levels around $70, while DCF analyses show mixed signals.

Also Read:

Table of Contents

Image source: coca-colacompany.com

Business Overview and Key Facts

The Coca-Cola Company stands as the world’s largest nonalcoholic beverage corporation, operating in more than 200 countries. Founded in 1886, the Atlanta-based company has built an unmatched global distribution network through its franchise business model.

The company generates revenue through two primary channels. First, it sells concentrates and syrups to bottling partners worldwide. Second, it sells finished beverages directly to retailers in certain markets.

Revenue Snapshot

For the last twelve months (LTM) ending September 2025, Coca-Cola reported total revenues of $36.1 billion. This represents steady growth despite facing headwinds in several markets.

The geographic revenue breakdown demonstrates global diversification:

Geographic Segment

Q3 2025 Organic Revenue Growth

Volume Performance

Europe, Middle East & Africa

7%

+4%

Latin America

4%

Flat

North America

4%

Flat

Asia Pacific

7%

-1%

Core Product Lines

Coca-Cola operates across five major beverage categories. Sparkling soft drinks remain the cornerstone, generating the majority of revenue.

Trademark Coca-Cola grew 1% in Q3 2025. Coca-Cola Zero Sugar surged 14%, reflecting the consumer shift toward healthier options. Diet Coke/Coca-Cola Light expanded 2%, primarily driven by North American demand.

The water, sports, coffee and tea segment grew 3%. Sports drinks advanced 3%, with the dual-brand strategy of Powerade and BODYARMOR gaining traction. The company’s ready-to-drink tea portfolio maintained global category leadership.

Value-added dairy represents a growing opportunity. The fairlife portfolio continues expanding in the United States. In Mexico, Santa Clara captured the value share leadership position with 13% volume growth during Q3 2025.

Latest Strategic Developments and News

Product Innovation Pipeline

Coca-Cola has accelerated its innovation cadence. Starting January 1, 2026, the company will introduce 7.5-ounce mini cans as single-serve options in convenience stores for the first time.

The Orange Cream flavor innovation launched in early 2025. Coca-Cola Orange Cream and Coca-Cola Zero Sugar Orange Cream remain available through early 2026. This represents a deliberate strategy to refresh flavor offerings continuously.

Minute Maid Zero Sugar has expanded into select Asia Pacific markets. The brand shows strong consumer interest and solid volume performance, building on North American success.

Image source: investors.coca-colacompany.com

Bottling System Transformation

The company’s franchise model evolution continues. In October 2025, Coca-Cola HBC AG announced a definitive agreement to acquire a controlling interest in Coca-Cola Beverages Africa (CCBA).

This refranchising step consolidates operations under a proven bottler. CCHBC brings strong operational expertise in African markets. The transaction strengthens the overall system’s capability to drive growth.

In India, the company sold a 40% ownership stake in Hindustan Coca-Cola Holdings to Jubilant Bhartia Group in July 2025. This represents another milestone in optimizing the bottling network.

Functional Beverage Expansion

The company has intensified its focus on functional beverages. The fairlife portfolio continues expanding, meeting consumer demand for protein-enriched dairy products.

BODYARMOR made its European debut in Spain during 2025. The brand’s international expansion leverages insights from its U.S. success against Gatorade. The Brussels innovation team adapted formulations for European consumer preferences.

China Market Optimism

Despite broader Asia Pacific challenges, management remains optimistic about China. The company is developing granular market strategies and customer-specific execution plans.

China contributed to Q1 2025 global unit case volume growth of 2%. The system continues investing in supply chain capabilities to support long-term expansion.