KLA Corporation - SWOT Analysis Report (2026)

Our comprehensive SWOT analysis examines KLA Corporation, which has established itself as a key player in process control and yield management solutions.

KLA Corporation $KLAC ( ▲ 5.55% ) has established itself as an indispensable player, commanding a dominant market share in process control and yield management solutions.

As you evaluate opportunities in the semiconductor equipment sector, understanding KLA’s competitive position through a comprehensive SWOT analysis becomes critical for informed decision-making.

Table of Contents

Understanding KLA Corporation’s Business Model

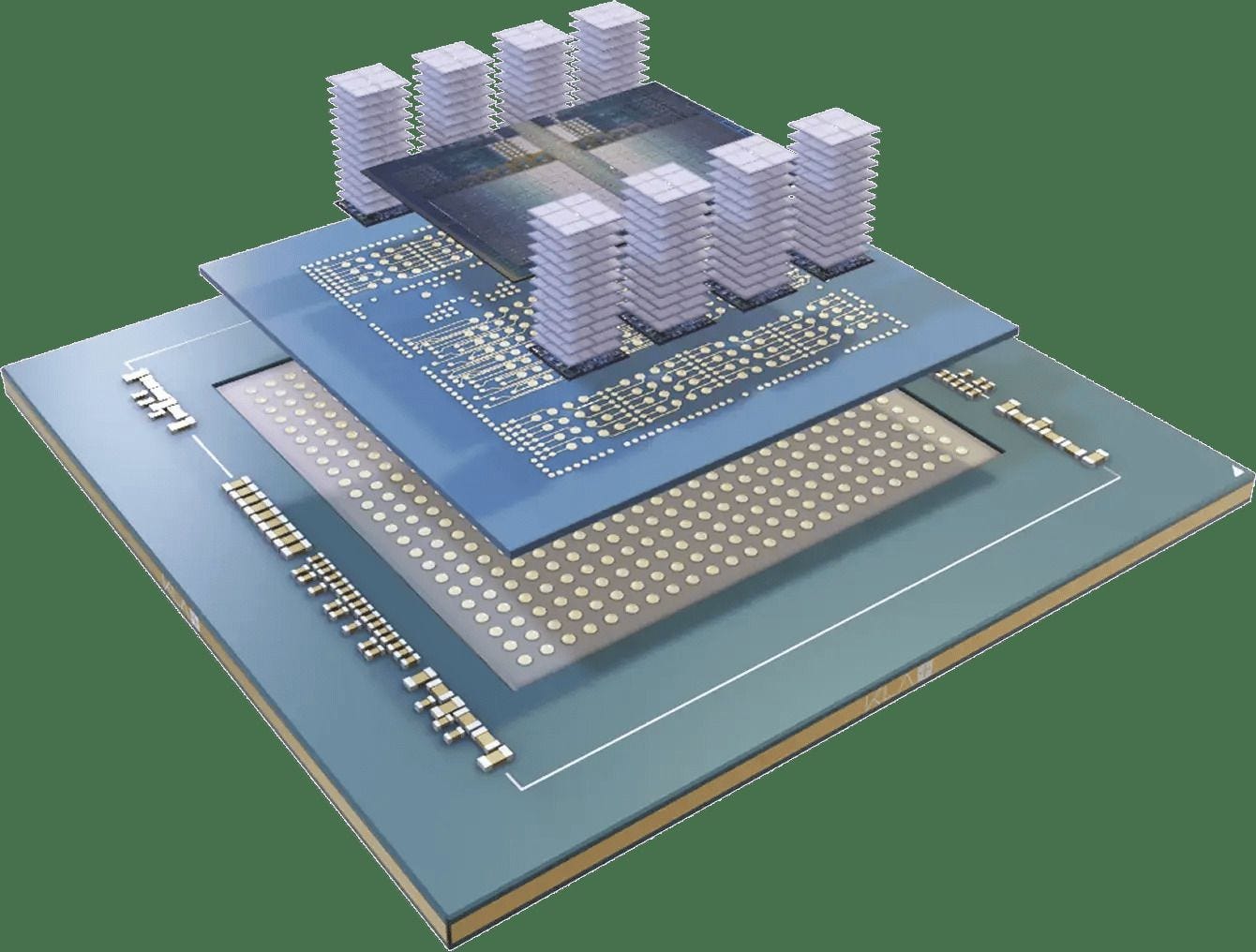

KLA Corporation develops and manufactures advanced equipment and services that enable innovation throughout the electronics industry. The company’s primary focus lies in process control solutions that help semiconductor manufacturers identify defects, measure critical dimensions, and optimize yields during chip production.

This specialization positions KLA as a crucial enabler of semiconductor manufacturing rather than a direct competitor to chip producers.

Image source: kla.com

The company reported impressive fiscal 2026 first quarter results ending September 30, 2025, with total revenues reaching $3.21 billion and GAAP diluted earnings per share of $8.47. These figures reflect double-digit year-over-year revenue and earnings growth, demonstrating KLA’s ability to capitalize on robust semiconductor industry demand.

Revenue Composition and Customer Base

KLA’s revenue structure reflects the company’s strategic positioning across multiple semiconductor market segments. According to the company’s latest financial disclosures, KLA’s semiconductor process control business divides into two primary customer categories:

CUSTOMER SEGMENT BREAKDOWN (Q1 FY2026)

========================================

Foundry/Logic Customers: 74%

Memory Customers: 26%

========================================

This distribution highlights KLA’s strong exposure to foundry and logic manufacturing, where advanced process nodes and AI chip production drive significant equipment demand. The company’s customer base includes virtually all major semiconductor manufacturers globally, creating a diversified revenue foundation.

Beyond equipment sales, KLA has built a substantial service business that provides recurring revenue streams. The company’s service revenue reached $744.7 million in Q1 FY2026, representing approximately 23% of total revenues. This service model includes maintenance contracts, spare parts, and system upgrades that generate predictable cash flows throughout economic cycles.

Strengths: Dominant Market Position and Technology Leadership

Unassailable Market Share in Process Control

KLA’s most significant strength lies in its commanding market position within the semiconductor process control segment. As of late 2025, KLA holds approximately 56% market share in process control, representing dominance that few technology companies achieve in competitive markets. This leadership extends across multiple product categories, with market share ranging from 50% to over 80% in various inspection and metrology segments.

The company’s market position creates several competitive advantages. First, KLA benefits from substantial switching costs, as semiconductor manufacturers invest heavily in qualifying and integrating process control equipment into their production lines. Second, the company’s installed base generates recurring service revenue and creates opportunities for upgrade sales. Third, KLA’s scale enables continued investment in research and development that smaller competitors struggle to match.

Technology Leadership Across Product Portfolio

KLA’s technology leadership manifests in multiple dimensions. The company maintains the industry’s most comprehensive portfolio of inspection and metrology tools, addressing virtually every process control requirement in modern semiconductor manufacturing. This breadth ensures KLA remains the single-source solution provider for many customers, strengthening customer relationships and increasing wallet share.

Recent product innovations demonstrate KLA’s technical capabilities. The company has introduced advanced e-beam inspection systems capable of detecting nanometer-scale defects critical for advanced node manufacturing. These systems employ sophisticated algorithms combining artificial intelligence and machine learning to identify patterns that human operators or traditional systems might miss.

In metrology, KLA’s overlay and critical dimension measurement tools set industry standards for accuracy and throughput. As semiconductor manufacturers transition to extreme ultraviolet lithography and gate-all-around transistor architectures, precise measurement becomes increasingly critical. KLA’s ability to deliver tools meeting these demanding specifications reinforces its technology leadership position.

Financial Performance and Operational Excellence

KLA CORPORATION FINANCIAL HIGHLIGHTS

=====================================================

Metric Q1 FY2026 Q1 FY2025

-----------------------------------------------------

Total Revenue $3.21B $2.84B

Year-over-Year Growth 13.0% --

GAAP Net Income $1.12B $946M

GAAP Diluted EPS $8.47 $7.01

Operating Cash Flow (LTM) $4.25B --

Free Cash Flow (LTM) $3.88B --

Gross Margin (Non-GAAP) 61.3% 61.7%

=====================================================

KLA’s financial performance demonstrates operational excellence across multiple dimensions. The company achieved fiscal year 2025 revenues of $12.16 billion, representing 23.89% growth from the prior year. This growth occurred against a backdrop of semiconductor industry cyclicality, highlighting KLA’s relative outperformance compared to broader wafer fabrication equipment markets.

Gross margins consistently exceed 60%, reflecting the high value-add nature of KLA’s products and limited direct competition in many process control segments. Operating margins similarly remain robust, enabling substantial free cash flow generation. In fiscal 2025, KLA generated over $4 billion in operating cash flow, providing resources for continued investment in research and development, strategic acquisitions, and shareholder returns.

The company’s return on invested capital significantly exceeds its cost of capital, creating economic value for shareholders. This financial strength provides flexibility to invest counter-cyclically during industry downturns, potentially gaining market share when competitors reduce spending.

Service Business: The Recurring Revenue Engine

KLA’s service business represents a strategic strength that differentiates the company from pure equipment vendors. Service revenue grew 15% year-over-year to $2.7 billion in fiscal 2025, demonstrating the stability and recurring nature of this model. More than 75% of service revenue comes from multi-year contracts, with renewal rates exceeding 95%.

This service model creates several advantages. First, it provides revenue stability during equipment spending downturns, partially offsetting cyclicality in systems sales. Second, maintaining close relationships with customers through service contracts creates opportunities to introduce new products and identify emerging requirements. Third, the high renewal rates demonstrate customer satisfaction and switching costs associated with KLA’s ecosystem.

The service business also exhibits attractive unit economics. Service contracts typically carry higher gross margins than equipment sales because they leverage the existing installed base without requiring full manufacturing costs. As KLA’s installed base grows, service revenue should continue expanding, providing an increasingly valuable revenue stream.

Weaknesses: Challenges in a Complex Operating Environment

Exposure to Semiconductor Industry Cyclicality

Despite its market leadership, KLA remains fundamentally exposed to the cyclical nature of semiconductor capital equipment spending. Semiconductor manufacturers adjust capital expenditures based on demand forecasts, capacity utilization, and technology transitions. During downturns, equipment orders can decline sharply, impacting KLA’s revenue and profitability.

Historical patterns demonstrate this cyclicality. Wafer fabrication equipment spending declined 6.51% in calendar 2024 before recovering in 2025. While KLA’s process control focus and service business provide some insulation, the company cannot completely escape industry cycles. Investors must account for this cyclicality when evaluating valuation multiples and long-term growth expectations.

The timing and severity of cycles have become increasingly difficult to predict. Rapid changes in end-market demand, inventory corrections, and geopolitical factors can trigger sudden spending adjustments. This unpredictability complicates planning and can lead to volatility in financial results quarter-to-quarter.

Geographic Concentration and China Exposure

KLA’s international operations expose the company to various operational risks. The company generates substantial revenue from Asia, where most semiconductor manufacturing occurs. This geographic concentration creates exposure to regional economic conditions, political stability, and regulatory changes.

China represents a particular challenge. KLA reduced its China revenue share from 41% in fiscal 2024 to approximately 30% in fiscal 2025, partially in response to U.S. export controls. While this diversification reduces concentration risk, it also eliminates a historically significant growth market. The company expects U.S. trade tensions to hurt sales by $300 million to $350 million over five quarters.

GEOGRAPHIC REVENUE EXPOSURE SHIFTS

====================================================

Region FY2024 Est. FY2025 Est.

----------------------------------------------------

China ~41% ~30%

Other Asia ~35% ~42%

Americas ~15% ~18%

Europe ~9% ~10%

====================================================

Note: Estimates based on public disclosures and analyst reports

Limited Product Diversification Outside Core Markets

While KLA dominates process control, the company has limited diversification into adjacent semiconductor equipment categories. Unlike competitors such as Applied Materials, which offers deposition, etch, and inspection tools, KLA focuses primarily on inspection and metrology. This specialization creates expertise depth but also limits addressable market expansion opportunities.

Applied Materials - SWOT Analysis Report (2026)

www.deepresearchglobal.com/p/applied-materials-swot-analysis-report

If process control equipment spending grows more slowly than other wafer fabrication equipment categories, KLA’s revenue growth could lag broader industry trends. Similarly, technology transitions that reduce process control intensity could pressure KLA’s market position, though such scenarios appear unlikely given increasing manufacturing complexity.

The company has addressed this weakness partially through its advanced packaging initiatives, expanding beyond traditional wafer-level process control. However, packaging represents a smaller market than front-end wafer processing, limiting the diversification impact.

High Customer Concentration Risk

KLA serves a concentrated customer base, with a small number of leading semiconductor manufacturers accounting for a substantial portion of revenues. The top customers likely include Taiwan Semiconductor Manufacturing Company (TSMC), Samsung, Intel, and SK Hynix. This concentration creates risk if any major customer reduces spending, encounters operational challenges, or switches to alternative solutions.

TSMC - SWOT Analysis Report (2026)

www.deepresearchglobal.com/p/tsmc-swot-analysis-report

Samsung Electronics - SWOT Analysis Report (2026)

www.deepresearchglobal.com/p/samsung-electronics-swot-analysis-report

Intel - SWOT Analysis Report (2026)

www.deepresearchglobal.com/p/intel-swot-analysis-report

SK Hynix - SWOT Analysis Report (2026)

www.deepresearchglobal.com/p/sk-hynix-swot-analysis-report

The company’s dependence on capital-intensive customers creates additional risk. Major semiconductor manufacturers face their own cyclical pressures and competitive dynamics that can affect their willingness and ability to invest in new equipment. Delays in customer roadmaps or technology transitions can create revenue volatility for KLA.

Opportunities: Secular Growth Drivers and Market Expansion

Artificial Intelligence Computing Revolution

The artificial intelligence revolution represents the most significant growth opportunity for KLA in the coming years. AI chip manufacturing requires advanced semiconductor process nodes, complex architectures, and exceptionally tight yield control. These requirements play directly to KLA’s strengths in process control and metrology.

Image source: kla.com

Graphics processing units and AI accelerators incorporate billions of transistors manufactured at leading-edge nodes below 5 nanometers. At these dimensions, even minuscule defects can cause chip failures or performance degradation. KLA’s inspection systems become increasingly critical as manufacturers push physical limits of silicon technology.

Beyond traditional logic chips, AI computing drives demand for high bandwidth memory. HBM stacks multiple DRAM dies vertically, placing them in close proximity to processors to reduce latency and increase bandwidth. This advanced packaging requires sophisticated inspection and metrology throughout the manufacturing process. KLA has positioned itself to address these requirements, with advanced packaging revenue expected to reach $925 million in fiscal 2025, up from previous targets.

The AI opportunity extends beyond near-term equipment sales. As AI infrastructure buildout continues through the remainder of the decade, KLA should benefit from sustained elevated demand. Even after the initial wave of capacity additions, ongoing equipment refreshes and technology transitions will drive continued spending.

Advanced Packaging Market Expansion

Advanced packaging represents a significant growth vector for KLA beyond traditional wafer-level process control. As semiconductor manufacturers increasingly adopt 2.5D and 3D packaging architectures, demand for packaging-specific inspection and metrology tools accelerates.

Several factors drive advanced packaging adoption. First, continued Moore’s Law scaling becomes increasingly difficult and expensive at extreme nodes. Packaging multiple chiplets together offers performance improvements and cost advantages compared to monolithic chip designs. Second, heterogeneous integration allows combining different process technologies and materials in a single package, enabling new functionality impossible with traditional approaches.

KLA has developed specialized tools addressing advanced packaging requirements, including hybrid bonding inspection, through-silicon via metrology, and die-to-wafer alignment systems. The company raised its 2025 advanced packaging revenue target to $925 million, citing strong demand from high-bandwidth memory, advanced packaging, and leading-edge logic applications.

ADVANCED PACKAGING REVENUE GROWTH TRAJECTORY

================================================

Year Revenue YoY Growth

------------------------------------------------

FY2024 $500M --

FY2025 $925M 85%

FY2026E $1,300M+ 40%+

================================================

Note: FY2026 represents analyst estimates

The advanced packaging opportunity should persist throughout the decade as adoption broadens beyond leading-edge AI chips to mainstream applications. Automotive electronics, mobile devices, and data center infrastructure will increasingly incorporate advanced packaging, expanding KLA’s addressable market.

EUV Lithography Adoption Acceleration

Extreme ultraviolet lithography represents a fundamental technology transition in semiconductor manufacturing. ASML’s EUV systems enable printing features at dimensions impossible with traditional deep ultraviolet lithography. As EUV adoption expands from leading-edge logic to memory and matures into high-volume manufacturing, process control requirements intensify.

ASML - SWOT Analysis Report (2026)

www.deepresearchglobal.com/p/asml-swot-analysis-report

EUV lithography introduces unique inspection challenges. The technology uses reflective optics rather than traditional refractive lenses, creating new potential defect modes. Photomasks for EUV require actinic inspection at EUV wavelengths, driving demand for KLA’s specialized reticle inspection tools. Wafer-level inspection must detect defects measured in single-digit nanometers to ensure EUV process yields.

KLA has invested heavily in developing EUV-specific process control solutions. These tools command premium pricing given their technical complexity and limited competition. As EUV tool installations accelerate globally, KLA should benefit from associated process control equipment orders and ongoing service revenue.

Semiconductor Market Growth and Regional Diversification

The broader semiconductor market continues expanding, driven by digitalization across industries. According to SEMI forecasts, global semiconductor equipment sales should reach $156 billion in 2027, representing sustained growth from $133 billion in 2025. This expansion provides tailwinds for equipment vendors including KLA.

Regional diversification opportunities also exist. While China faces restrictions, other regions including Southeast Asia, India, and Europe seek to build domestic semiconductor manufacturing capabilities. Government incentives and geopolitical considerations drive these initiatives, creating incremental equipment demand. KLA’s process control tools remain essential regardless of manufacturing location, positioning the company to benefit from geographic diversification.

Memory market recovery represents another opportunity. After extended weakness in DRAM and NAND flash markets, memory manufacturers have begun increasing capital expenditures. Memory production requires intensive process control given the repetitive structures and tight specifications. KLA typically captures disproportionate share in memory spending relative to other equipment categories.

Emerging Applications and Technology Platforms

Beyond traditional computing applications, semiconductors increasingly enable emerging technologies including autonomous vehicles, Internet of Things devices, and renewable energy systems. Each application creates unique semiconductor requirements and manufacturing challenges, potentially driving specialized process control needs.

Automotive semiconductors, for example, require exceptional reliability given safety-critical applications. This reliability demands rigorous defect inspection and process monitoring throughout manufacturing. KLA’s automotive-grade inspection tools address these requirements, creating incremental revenue opportunities as vehicle semiconductor content increases.

Power semiconductors represent another emerging growth area. Silicon carbide and gallium nitride devices enable more efficient power conversion in applications from electric vehicles to data centers. These wide-bandgap materials require specialized inspection and metrology approaches, creating opportunities for KLA to develop and deploy new tool categories.

Threats: Navigating Challenges in a Geopolitically Complex World

Geopolitical Tensions and Export Controls

U.S.-China technology competition represents the most significant near-term threat to KLA’s business. Export controls on advanced semiconductor equipment to China have already impacted KLA’s revenue, with management quantifying the impact at $300-350 million over five quarters. Future policy changes could further restrict technology transfers, potentially eliminating additional revenue.

The dynamic nature of export regulations creates ongoing uncertainty. Policy adjustments can occur with limited warning, making long-term planning difficult. KLA must invest resources in compliance systems and may need to develop separate product variants meeting export restrictions. These activities increase costs without generating incremental revenue.

Beyond U.S.-China relations, broader geopolitical tensions affect semiconductor supply chains. The Russia-Ukraine conflict, Middle East instability, and various regional disputes create risks to KLA’s operations, supply chains, and customer demand. While the company has successfully navigated these challenges historically, escalation scenarios could prove more disruptive.

Intensifying Competition in Process Control

While KLA maintains dominant market share, competitive threats persist and may intensify. Applied Materials, the largest semiconductor equipment vendor, continues developing process control capabilities. Applied Materials’ broad product portfolio and customer relationships create advantages in cross-selling inspection and metrology tools alongside deposition and etch systems.

Smaller specialized competitors also pose threats in specific niches. Companies including Onto Innovation, Camtek, and various Asian equipment vendors target particular process control segments with competitive pricing or specialized capabilities. While none match KLA’s comprehensive portfolio, competitors could capture share in specific applications or regions.

Technology disruption represents another competitive risk. New inspection approaches leveraging artificial intelligence, computational imaging, or alternative physical principles could potentially challenge KLA’s installed base. The company must continue investing heavily in research and development to maintain technology leadership, with no guarantees that all investments will succeed commercially.

Technology Transition Risks and Obsolescence

Semiconductor manufacturing undergoes constant evolution, with each technology generation introducing new challenges and requirements. While these transitions typically favor KLA by creating demand for more advanced process control, they also carry execution risks. If KLA fails to deliver competitive solutions for emerging technology nodes or architectures, competitors could gain share.

The transition from FinFET to gate-all-around transistor architectures represents one such inflection point. These new structures require different inspection and metrology approaches to monitor critical dimensions and detect defects. KLA has invested in developing appropriate tools, but delays or performance shortfalls could impact its competitive position.

Similarly, new materials including high-mobility semiconductors and 2D materials may require novel inspection techniques beyond KLA’s current capabilities. The company must anticipate these transitions and invest speculatively in emerging technologies, accepting that some investments may never generate meaningful returns if the industry follows different paths.

Economic Downturn and Spending Slowdown Scenarios

Macroeconomic conditions significantly influence semiconductor capital equipment spending. An economic recession could trigger inventory corrections, demand slowdown, and reduced capital expenditures by semiconductor manufacturers. Even KLA’s service business, while relatively stable, would face pressure if customers seek cost reductions.

Recent history provides cautionary examples. The COVID-19 pandemic initially disrupted equipment deliveries and installations before triggering a surge in semiconductor demand. However, the subsequent inventory correction in late 2022 and early 2023 led to reduced equipment spending. Similar patterns could recur if economic growth slows or end-market demand weakens.

Interest rate environments also affect capital equipment purchasing decisions. Higher interest rates increase the cost of financing capital expenditures, potentially causing customers to delay or reduce equipment orders. While semiconductor manufacturers generally maintain strong balance sheets, marginal projects become less attractive at higher discount rates.

Supply Chain Vulnerabilities and Component Availability

KLA’s manufacturing depends on complex global supply chains incorporating components from multiple suppliers and geographies. Supply chain disruptions can delay equipment deliveries, increase costs, and impact customer satisfaction. Recent years have demonstrated supply chain vulnerability through semiconductor shortages, logistics challenges, and geopolitical disruptions.

Component availability represents a particular concern for specialized materials and parts with limited suppliers. If key suppliers encounter operational challenges, quality issues, or capacity constraints, KLA’s production could be impacted. The company has implemented risk mitigation strategies including qualifying multiple suppliers and maintaining strategic inventory, but complete elimination of supply chain risk remains impossible.

Natural disasters, pandemics, and climate events pose additional supply chain threats. Semiconductor equipment manufacturing concentrates in specific regions, creating exposure to localized disruptions. A major earthquake in semiconductor equipment manufacturing hubs could significantly impact industry-wide equipment availability.

Strategic Positioning for Long-Term Success

Management Execution and Strategic Priorities

KLA’s management team has demonstrated consistent execution against strategic priorities. The KLA Operating Model emphasizes four key pillars: technology leadership, operational excellence, a winning culture, and a trusted partnerships with customers. This framework has guided the company through multiple industry cycles while maintaining market leadership.

Current strategic priorities focus on capitalizing on secular growth opportunities while maintaining financial discipline. Management has articulated clear targets for advanced packaging revenue expansion, service business growth, and market share gains in emerging applications. The company balances growth investments with shareholder returns through dividends and share repurchases.

Capital allocation decisions reflect financial discipline and shareholder-friendly policies. KLA generated $3.88 billion in free cash flow over the last twelve months, providing substantial resources for investment and returns. The company returned $3.09 billion to shareholders through dividends and buybacks during this period, demonstrating commitment to balanced capital deployment.

Financial Strength and Balance Sheet Flexibility

KLA maintains a solid financial position with manageable leverage and strong cash generation. The company’s debt-to-EBITDA ratio remains conservative, providing flexibility for strategic investments or opportunistic acquisitions. Fitch Ratings affirms KLA’s ratings at ‘A’ with a stable outlook, reflecting the company’s strong business position and financial management.

This financial strength enables counter-cyclical investment strategies that can strengthen competitive positioning. During industry downturns when competitors reduce spending, KLA can maintain or increase research and development investments, potentially accelerating product development cycles. Similarly, acquisition opportunities may arise during periods of market stress when valuation multiples compress.

The company’s consistent cash generation supports a progressive dividend policy. KLA has increased dividends annually, providing shareholders with growing income streams alongside capital appreciation potential. This combination appeals to income-focused investors while demonstrating management’s confidence in sustainable cash flow generation.

Investment in Research and Development

R&D INVESTMENT TRENDS

=====================================================

Period R&D Expense % of Revenue

-----------------------------------------------------

Q1 FY2026 $360.5M 11.2%

Q1 FY2025 $323.1M 11.4%

FY2025 Full $1,380M+ 11.3%

=====================================================

KLA’s substantial research and development investments underpin its technology leadership position. The company consistently invests over 11% of revenues in R&D, exceeding many semiconductor equipment peers. These investments fund development of next-generation inspection and metrology systems, advanced software and algorithms, and emerging technology platforms.

The company’s R&D strategy emphasizes close collaboration with leading semiconductor manufacturers to understand future requirements. This customer intimacy ensures KLA develops solutions addressing actual manufacturing challenges rather than pursuing speculative technologies with uncertain market demand. Early customer engagement also accelerates product development cycles and facilitates rapid market adoption.

Disclaimer: This analysis is for informational purposes only and should not be construed as investment advice. Investors should conduct their own due diligence and consult with financial advisors before making investment decisions.